Original source: Ouke Cloud Chain Research Institute

Original author: Hedy Bi

Digitalization is blurring the boundaries of traditional industries. This is a true financial revolution.

McKinsey described this digital wave in its 2017 Competing in a Borderless World report. As global acceptance of virtual assets grows, the potential behind them has sparked discussions among regulators. When tokens are regarded as financial instruments, security tokens become the focus of regulatory agencies in various countries, including the Hong Kong Securities and Futures Commission (SFC).

Since the beginning of this year, Ouke Cloud Chain Research Institute has participated in the Hong Kong government’s proposals for virtual asset platforms and continued to conduct in-depth exchanges with all walks of life in Hong Kong. Looking back at the Policy Declaration on the Development of Virtual Assets in Hong Kong issued by Hong Kong on October 31, it reiterated the potential and prospects of tokenization. In addition, just last month, Huang Lexin, head of the financial technology department of Hong Kong SFC, said that security tokens and Real World Assets (RWA) will no longer be included in the “complex” product definition, mentioning that there may be a new version of Security Token Offering (STO) regulations.

The issuance and trading of financial assets are usually subject to strict supervision, among which securities are the most representative. Security tokens are similar to traditional securities, so exploring the regulation of security tokens is one of the types of tokens that regulators can most easily expand their regulatory scope.

Hong Kong supervision is on the road to success

The author believes that SFC has a run-up attitude towards security tokens. The specific points are as follows:

1. 1+ License No. 7

Hong Kong regulators have different requirements for licenses depending on whether the trading services provided are security tokens or not, as well as the nature of the institution itself. Specifically, virtual asset trading platforms that provide or actively promote security token trading services in Hong Kong need to obtain Type 1 regulated business (securities trading) and Type 7 regulated business (providing automated trading services) issued by the Hong Kong Securities Regulatory Commission. )license. Platforms that offer non-security tokens also need to obtain a VASP license.

Any person or institution that promotes and distributes security tokens (whether in Hong Kong or to Hong Kong investors) is subject to Type 1 regulations under the Securities and Futures Ordinance unless an applicable exemption is obtained. be licensed or registered to regulate activities (securities trading).

2. Remove the 12-month post-issuance track record requirement

Security tokens no longer require a 12-month post-issuance track record. However, licensed platform operators need to comply with the general token inclusion criteria under the Guidelines for Virtual Asset Trading Platforms and the securities token distribution guidelines to be issued by the China Securities Regulatory Commission in due course.

3. Reasonable Due Diligence

Platform operators are required to conduct reasonable due diligence on security tokens proposed to be traded on the platform, and are ultimately responsible for this. At the same time, platform operators also need to ensure that internal monitoring measures, systems, technologies, etc. can support any specific risks.

Transactions are put on the chain, and compliance is also put on the chain.

When financial institutions face the issuance and trading of such high-speed and all-weather financial instruments, in addition to obtaining licenses as the first step in the industry, relevant parties such as platform operators, dealers and brokers should carry out self-internal monitoring and risk management measures , and focus on anti-money laundering and counter-terrorist financing (AMLCFT).

According to public information statistics, the total amount of anti-money laundering (AML) fines last year was nearly 5 billion US dollars. Most penalties are related to authentication and"know your customer"(KYC) solutions are poorly implemented or internal policies and risk management systems are inadequate. And in December last year, the Legislative Council passed the Anti-Money Laundering and Terrorist Financing (Amendment) Bill 2022 to complete the regulatory framework, and only then did Hong Kong make great strides into Web3.

Source:Sumsub

When the transaction is on the chain, AML compliance also needs to be on the chain. According to the internationally recognized recommendations of the Financial Action Task Force (FATF), the three aspects of customer identification and risk assessment, continuous monitoring and reporting, and control measures that AML CFT focus on also need to be adjusted accordingly.

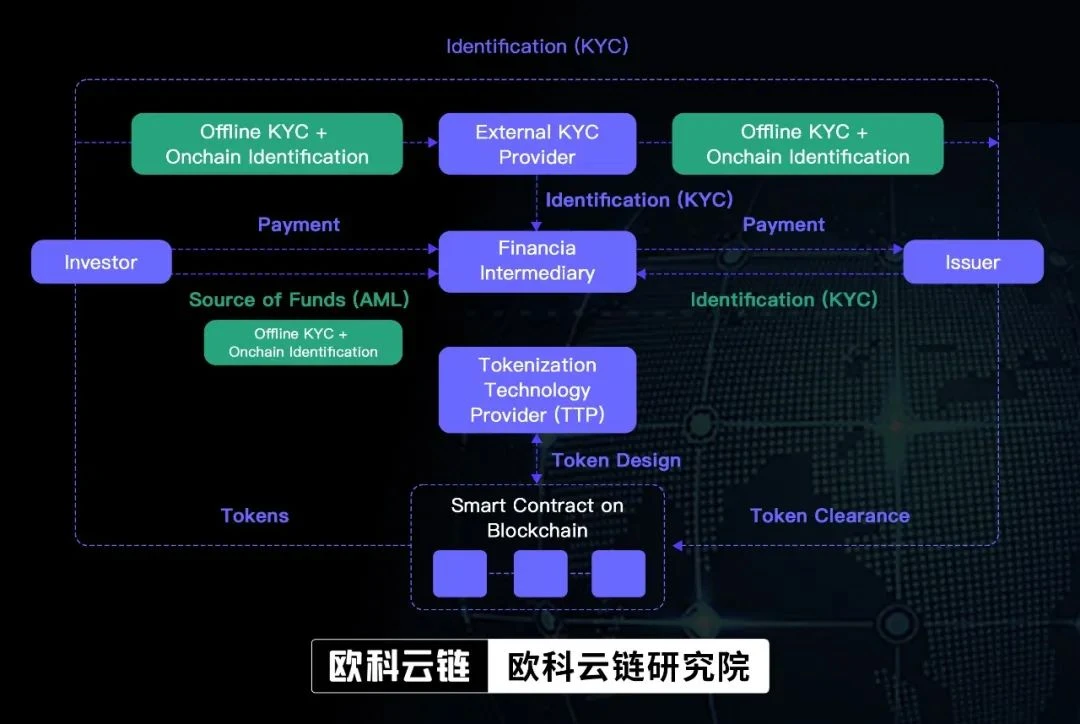

Taking security tokens as an example, during the issuance stage, virtual asset trading platforms, dealers, brokers, etc. require transaction parties to provide KYC, which belongs to off-chain information collection for customer identification. This step is a routine measure in traditional financial compliance. When an investor provides an account address (wallet) on the chain and trades with his assets on the chain, KYC should also continue to be identified on the chain, as shown in the figure below See that comprehensive identification of customer identities occurs throughout the entire process.

Source: ResearchGate

When security tokens can circulate freely without relying on intermediaries, KYA (Know Your Address, Note 1) and KYT (Know Your Transaction, Note 2) on the chain become particularly important .

This is different from traditional securities, which are based on a centralized structure, and the compliance of inter-institutional transactions is ensured by KYC at all levels of institutions. The most effective way for financial institutions is to use on-chain compliance tools such as OKLink, Chainalysis, Elliptic and other chain compliance tools to track customers virtual asset movements on the chain, so as to conduct whole-process supervision and full-chain tracking, aiming to prevent account ( On-chain address) money laundering that is out of touch with real identity.

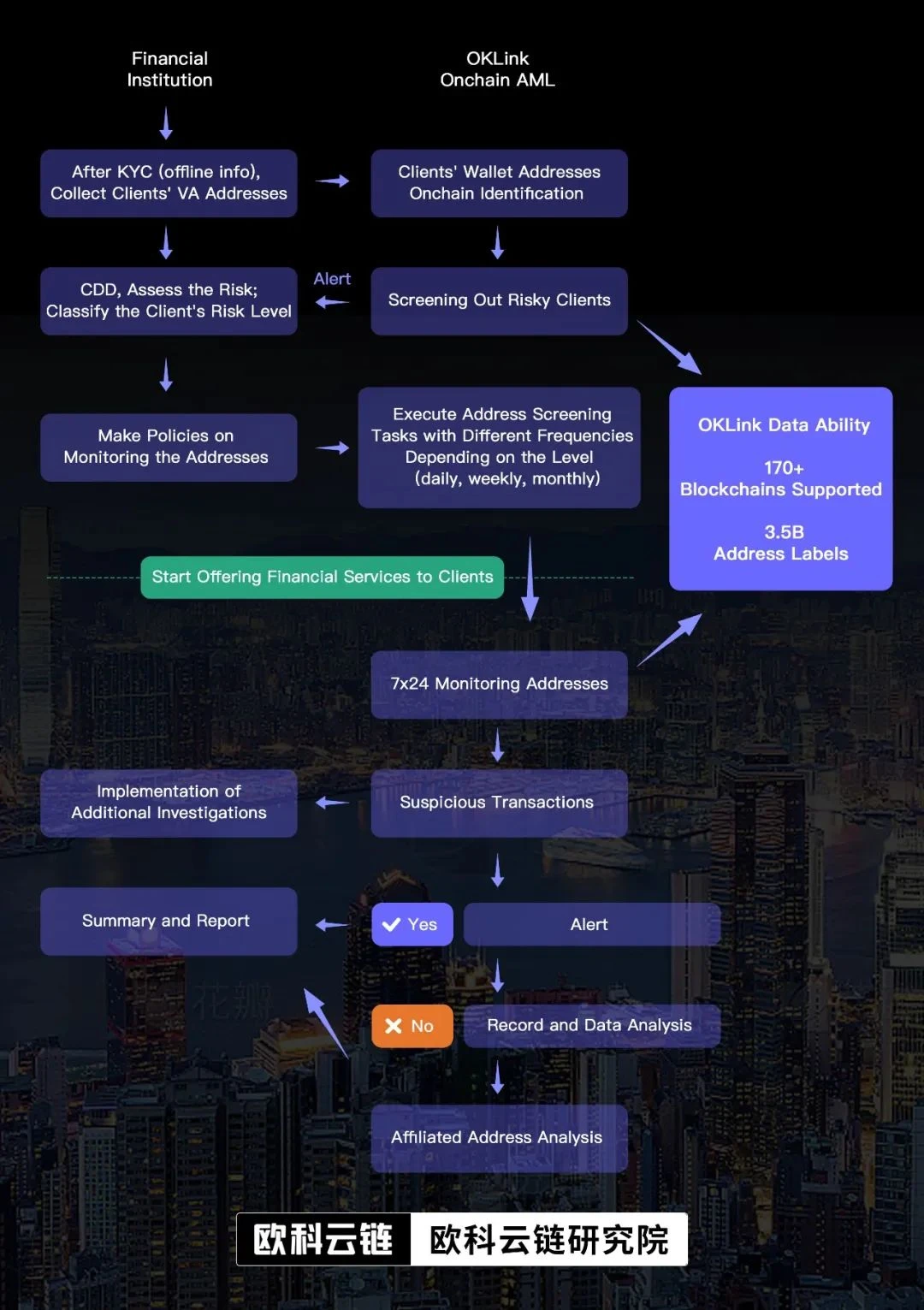

The following figure takes OKLinks Onchain AML as an example to illustrate how financial institutions use on-chain compliance tools to manage risks throughout the life cycle, so as to achieve mutual cooperation between the chain and the off-chain:

Financial institutions like Barclays Bank of the United Kingdom have tried to use on-chain compliant financial tools to identify risks and prevent risks brought about by AML CFT as early as 2015. Not only that, financial institutions including financial technology companies such as banks and payments have invested in on-chain compliance tools. According to public information statistics, the largest round of investment has reached 60 million US dollars, while on-chain compliance tools The valuation of leading companies on the track is also as high as nearly 10 billion US dollars.

We have been cultivating in the field of on-chain data for many years, and the ultimate goal is to become an on-chain navigator in this intricate new digital world. With the continuous acceptance of virtual assets by the global and Hong Kong governments, OKLinks launch of Onchain AML will provide financial Institutions and participants provide reliable compliance guidance. Nick Xiao, Product Director of OKLink, said.

Security tokens, a new representation of ownership

At the end of the day, security tokens represent ownership, such as equity, real estate, etc. The biggest difference between them and securities is that each asset is built on the blockchain in the form of tokens (according to the latest IMF article, tokens are units formulated by entries in digital ledgers using encryption technology) of. Similar to the securities market, the issuance and trading of security tokens need to comply with financial regulatory regulations and norms.

As a new representative of ownership, security tokens also mean that Web3 is using the digital form of its tokens to break the boundaries of the securities industry. Through global accessibility, high liquidity, high security and transparency, and automation and intelligence, etc., Continuously broaden the boundaries of the traditional securities industry. Liang Hanjing, director of finance, finance and financial technology of the Hong Kong Investment Promotion Agency, said in June this year that from the Hong Kong government level, asset tokenization (including security tokens) is regarded as a multi-trillion-level business opportunity.

Combining traditional financial tools with blockchain technology is an eternal topic in the global financial industry. At the same time, this has put forward new requirements for the technical regulatory capabilities of regulatory agencies, but this does not affect the introduction of global regulation of securitization tokens and its positioning. In addition to Hong Kong SFC, Okey Cloud Research Institute has sorted out the regulatory status of securities tokenization in major countries around the world, as shown in the table below.

The original nature of business will not change in the future. When the transaction is on the chain, this trillion-level business opportunity will be opened. Only after the compliance is ensured and it is included in the operation of the chain, is this the time when the mainstream truly recognizes a new technology.

About Okey Cloud Chain Research Institute: Okey Cloud Chain Research Institute is a strategic research institution under Okey Cloud Chain Group, with the mission of helping global business, public and social sectors to better understand the evolution of financial technology and blockchain economy , output in-depth analysis and professional content, covering topics such as technology application and innovation, technology and social evolution, and financial technology challenges, and is committed to promoting the application and sustainable development of cutting-edge technologies such as blockchain technology.