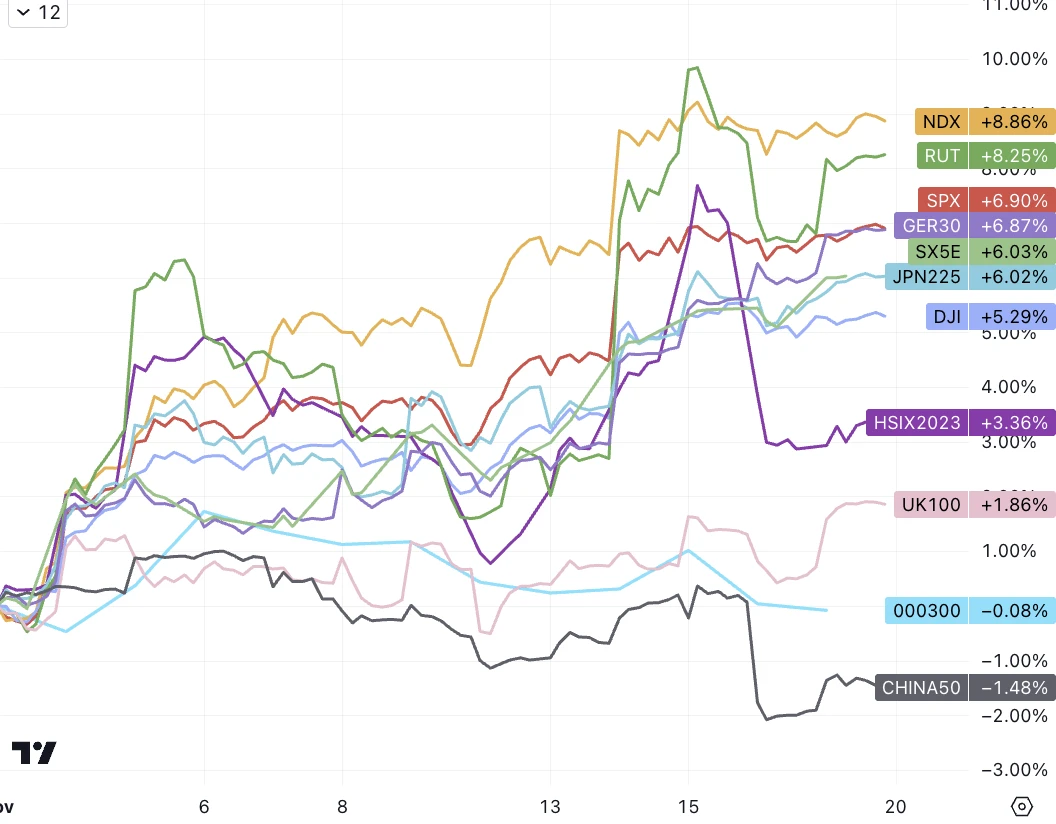

U.S. stock indexes have risen for three weeks in a row, basically recovering from their losses over the past three months. The recent market reaction is reminiscent of the market reaction after inflation cooled down for the first time this summer. The main line of this round is that the market rebounded because it confirmed that the Federal Reserve has ended this round of interest rate hikes. The supporting evidence is that the Federal Reserve hinted that it will reduce the scope of interest rate hikes and that it dropped more than expected. Inflation and employment data. Shifts in policy expectations and actual market interest rates are positive for stocks, bonds, non-U.S. currencies, including cryptocurrencies. U.S. President Joe Biden is expected to sign a temporary spending bill on Friday, officially averting a U.S. government shutdown this weekend, and the market reacted calmly to this.

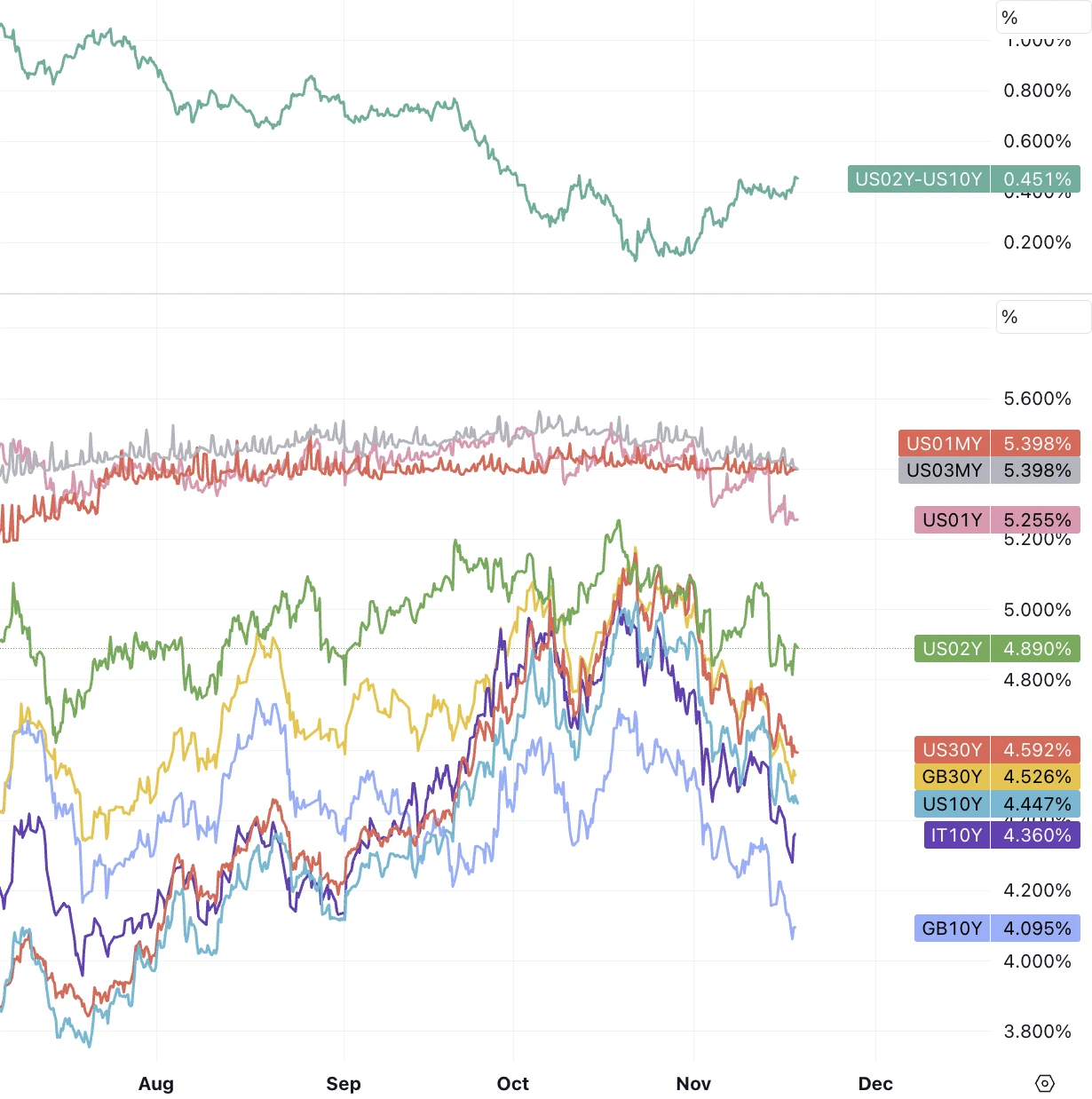

The 10-year U.S. bond briefly fell below 4.38% last Friday, and the 2-year U.S. bond fell below 4.80%, setting intraday lows in two months. The UK 10 Yr fell back to its May low.

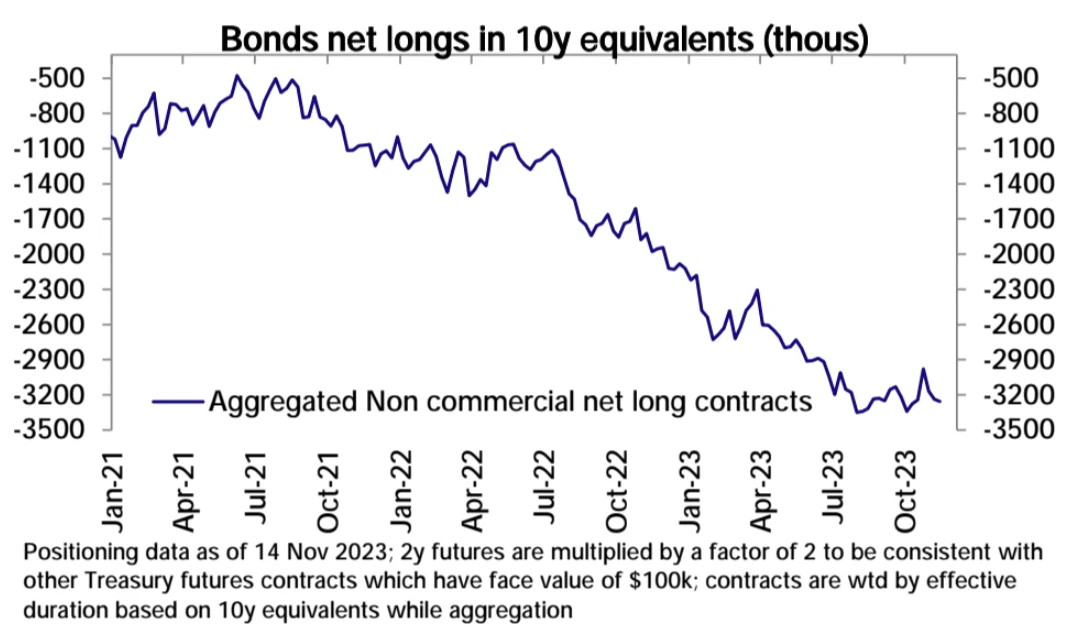

In the short term, the markets expected trading on the timing and magnitude of interest rate cuts will most likely continue, but the swing should not be too large. The timing is expected to fluctuate within 5 to 7 months (May is now expected), and the magnitude is expected to be between 75 and 150 bp (now expected to be 100, about 70 a month ago, which is already an exaggeration, the Fed itself expected only 20), only under a relatively pessimistic economic background, the first interest rate cut is possible earlier than in May, and the magnitude It is possible to exceed 100 bp. Therefore, the pricing of the short-term interest rate market has basically been completed. It is still difficult to say about the long-term. There are no less problems such as supply, deficit and political chaos, and there will only be more. It can also be seen from the futures data that the short-selling power has hardly weakened and has increased in the past two weeks.

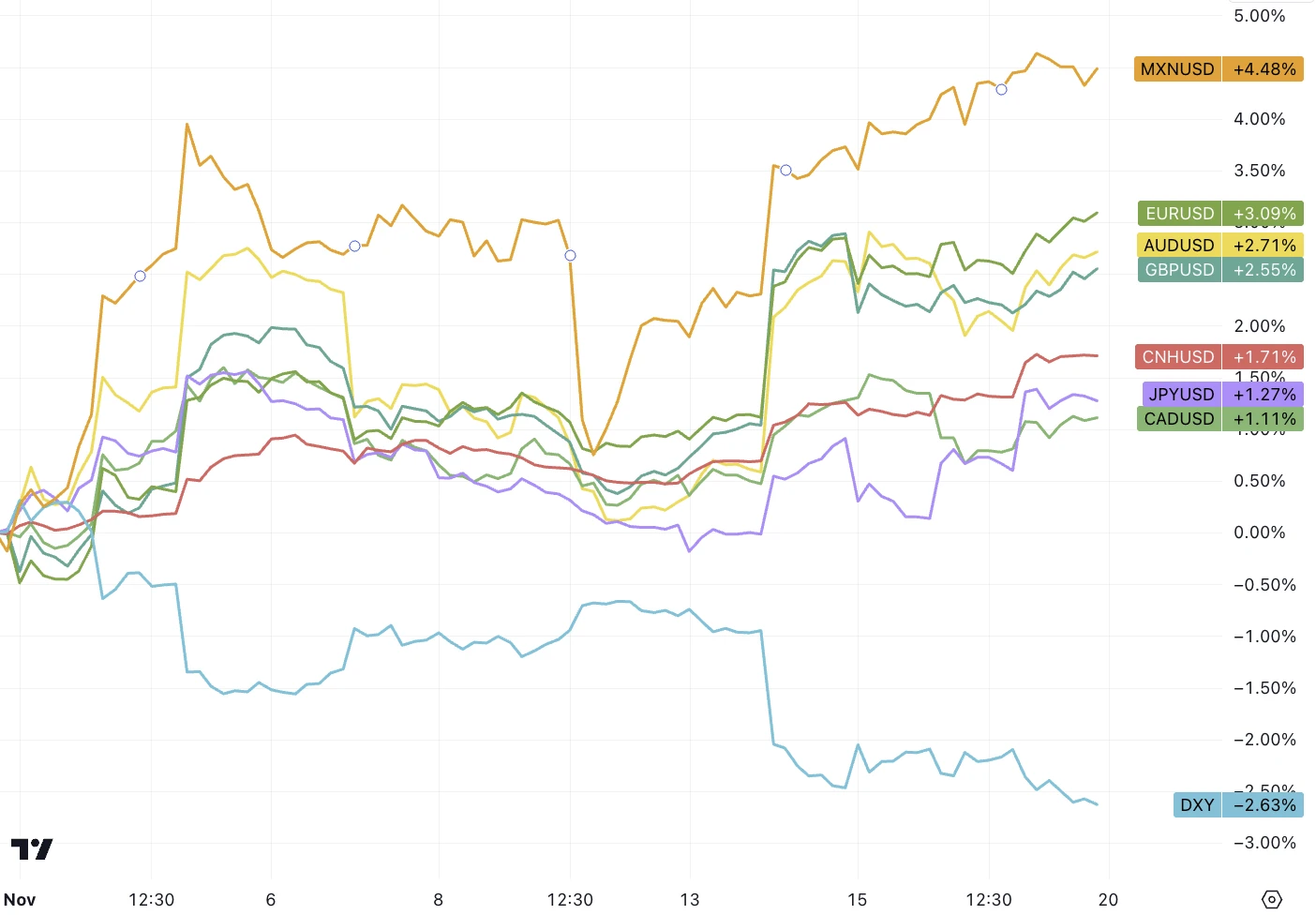

The U.S. dollar has weakened recently as expectations for interest rate hikes have cooled, with the U.S. dollar index recording its largest weekly decline in four months. Non-US currencies, including the RMB, experienced rapid appreciation last week, with CNH rapidly moving from 7.30 to 7.25. Seasonal factors also support the tendency of the RMB to strengthen in the last two months of the year, which is related to the foreign exchange settlement (selling foreign currency and buying RMB) habits of many companies. Fundamentally speaking, the relative return prospects of U.S. dollar competitors are also poor, so the attractiveness of the U.S. dollar is unlikely to be significantly eroded at this stage.

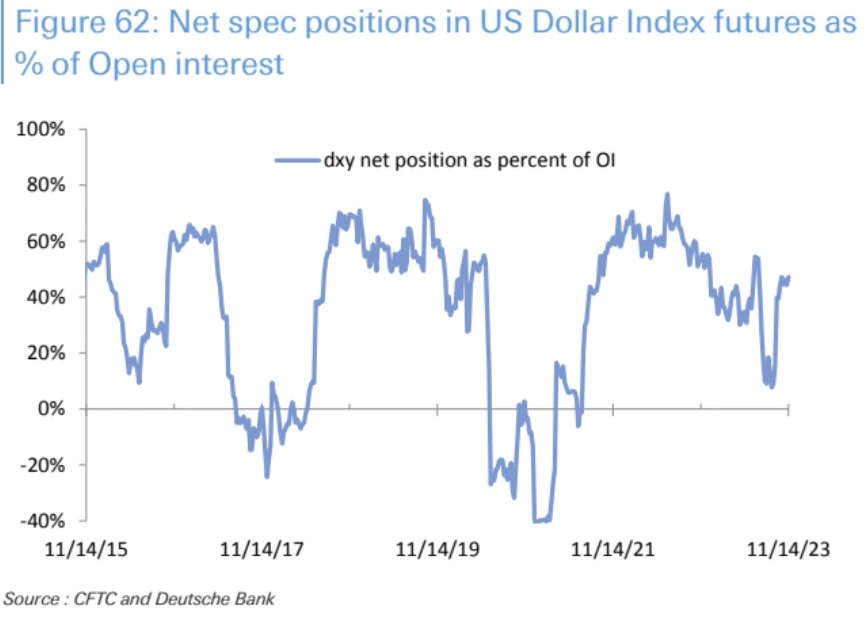

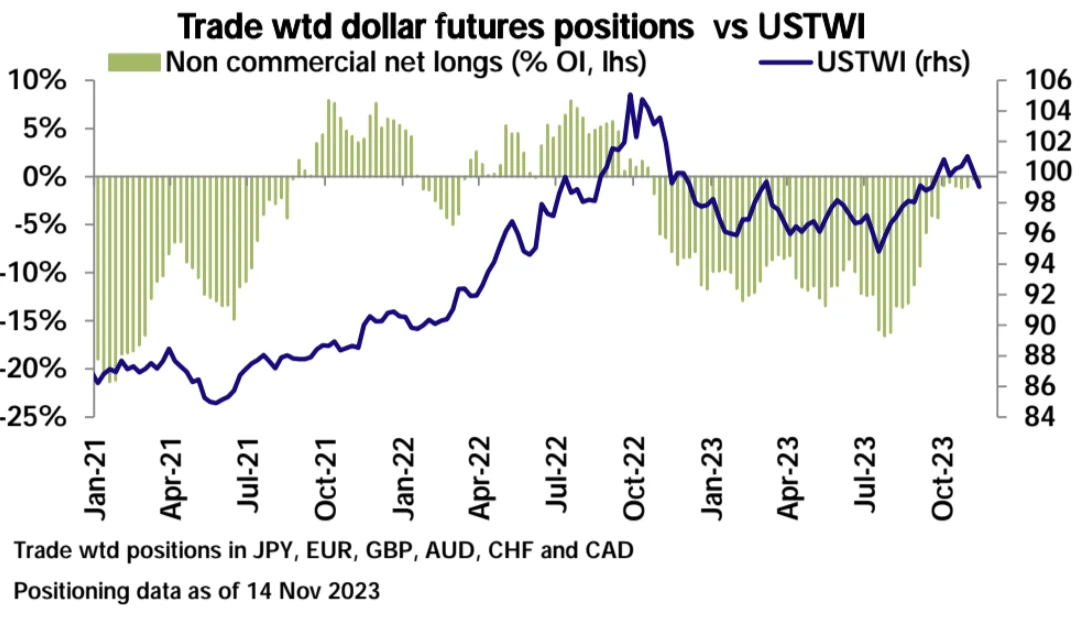

In terms of positions, the relative level of net long positions in the U.S. dollar index is not low, and there may be motivation to close positions.

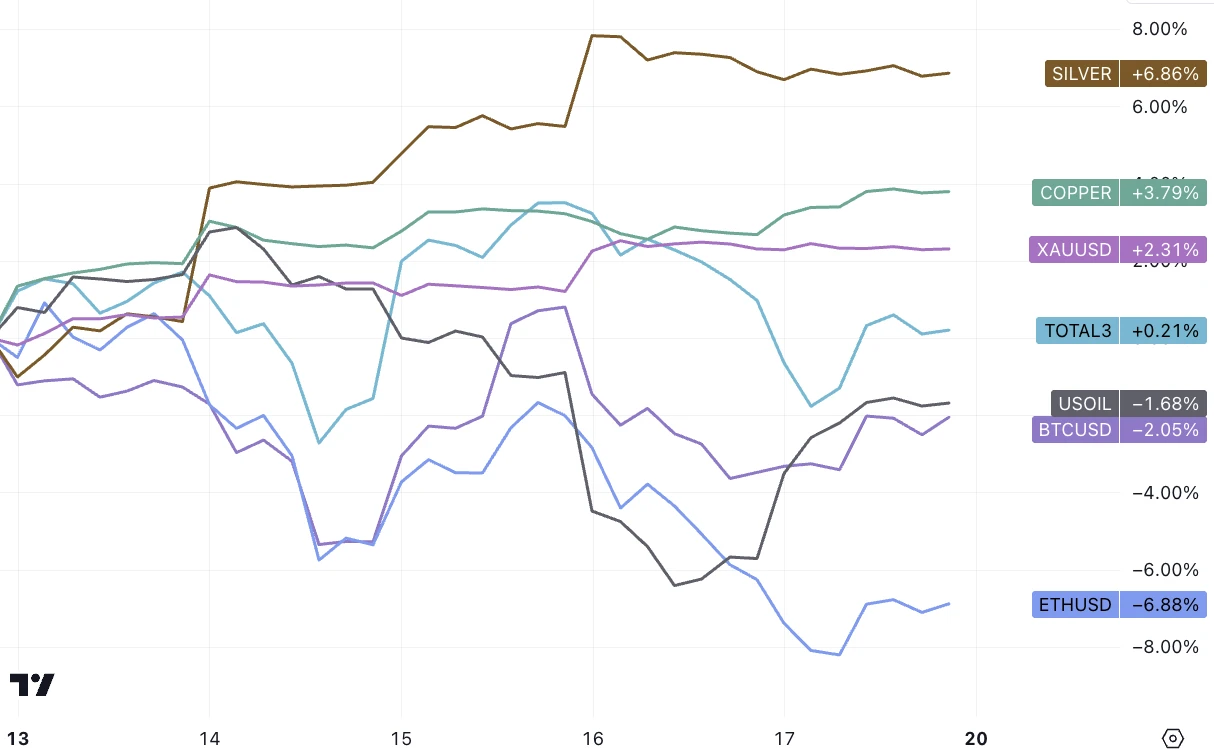

Benefiting from the weakening of the U.S. dollar and interest rates, gold and silver have soared. As expected, the SEC continues to postpone the spot ETF decision. Cryptocurrencies have experienced shock corrections, and Alt has performed relatively strongly:

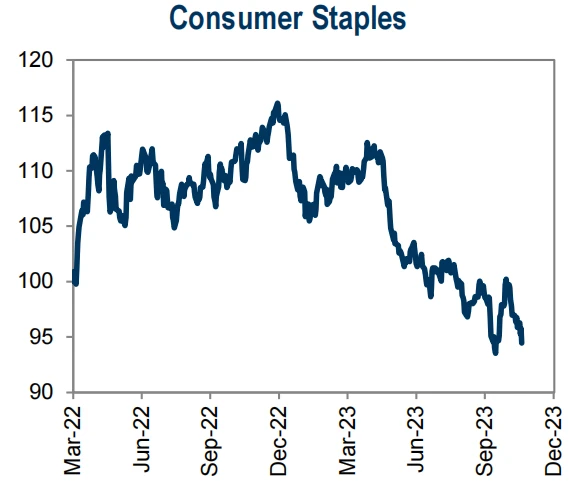

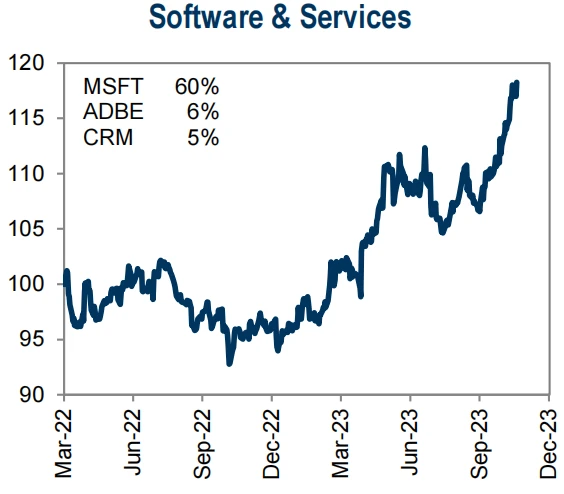

The pressure to liquidate short positions on U.S. stocks continues to be released, and the performance of technology stocks is divided. Non-profit technology stocks have surged, while giant technology stocks have been relatively dull. Regional banks and stocks with the largest short positions also saw larger gains, while consumer staples suffered sharp selloffs.

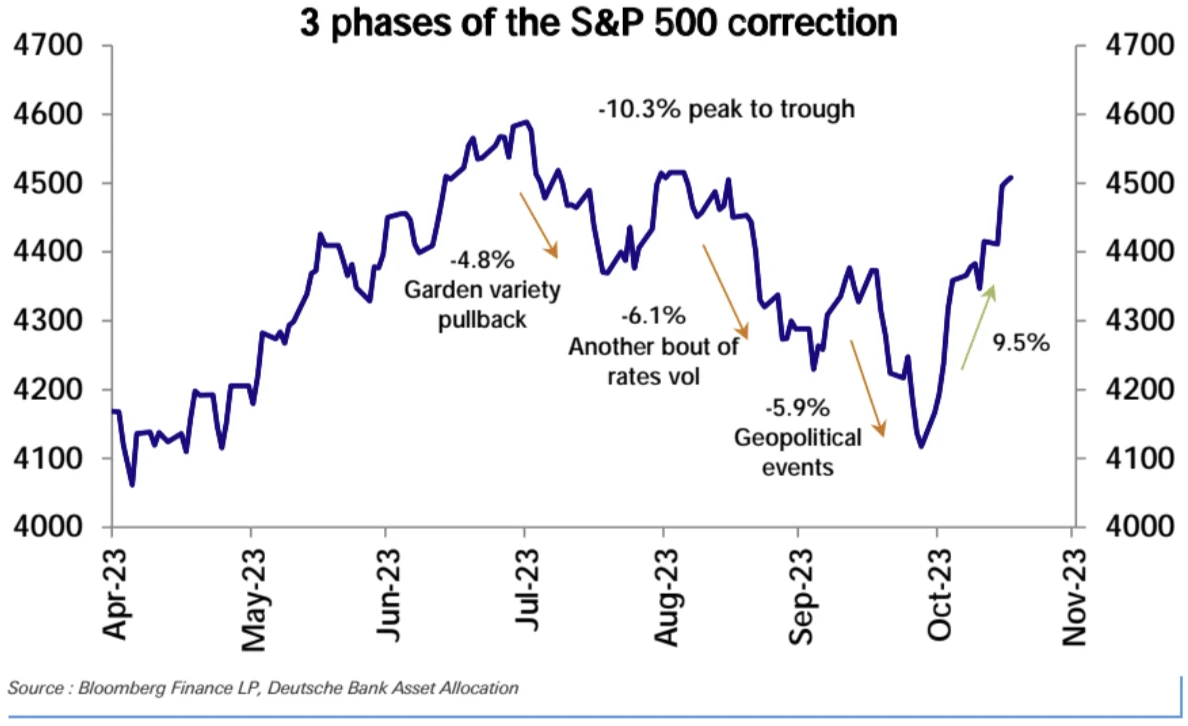

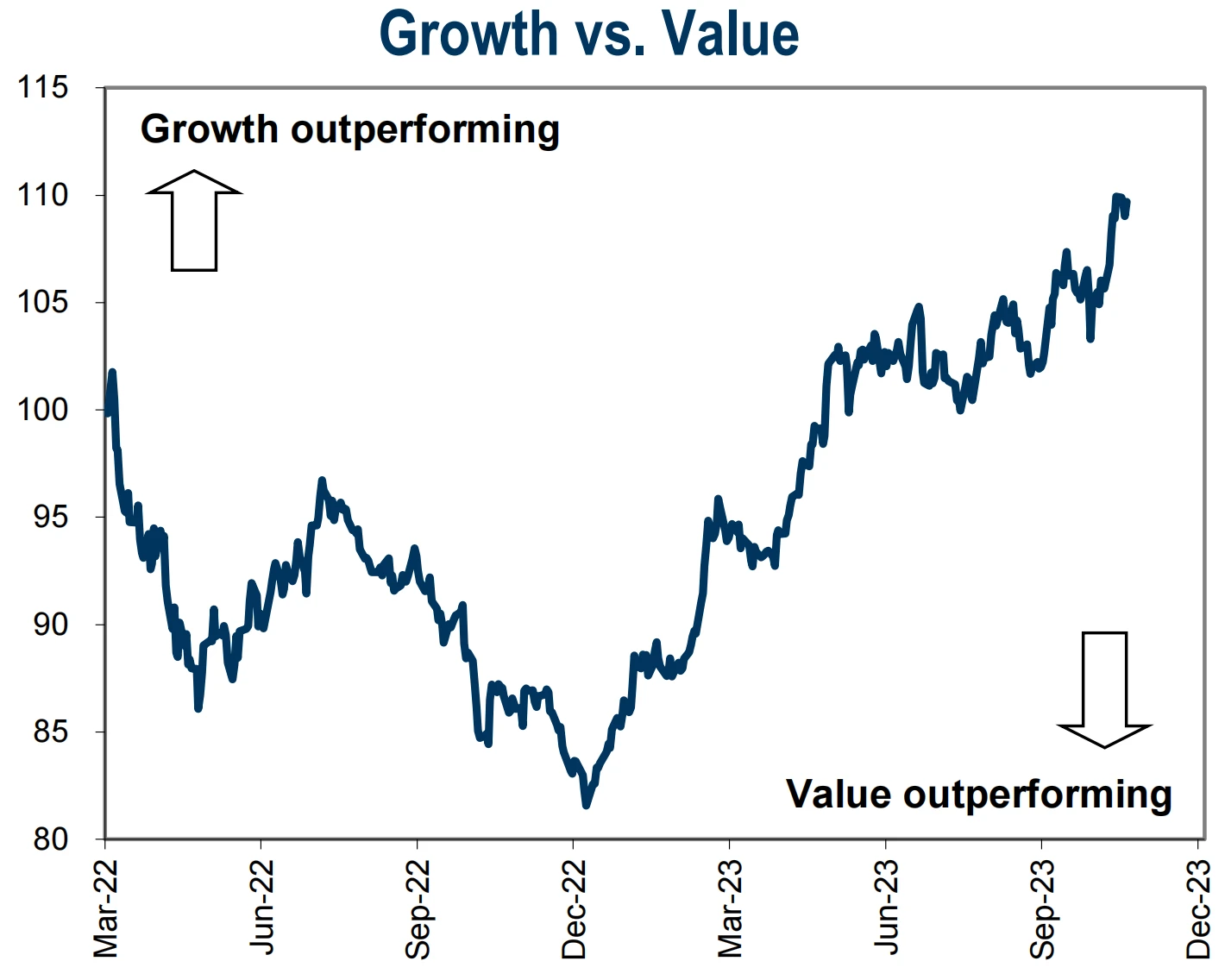

Key characteristics of stocks that outperformed last week were those that benefited from lower interest rates, lower oil prices, and previously weaker stocks, suggesting that the rebound was largely a reversal of recent shocks. There were three clear phases or drivers of the 10% correction from August to October: the normal correction in August, the impact of interest rate fluctuations in September, the geopolitical crisis in October, and now the stock market rebound unleashing the impact of interest rate fluctuations and geopolitical shocks , but from the perspective of stock performance, it has not yet reflected the expectations of upward cyclical growth.

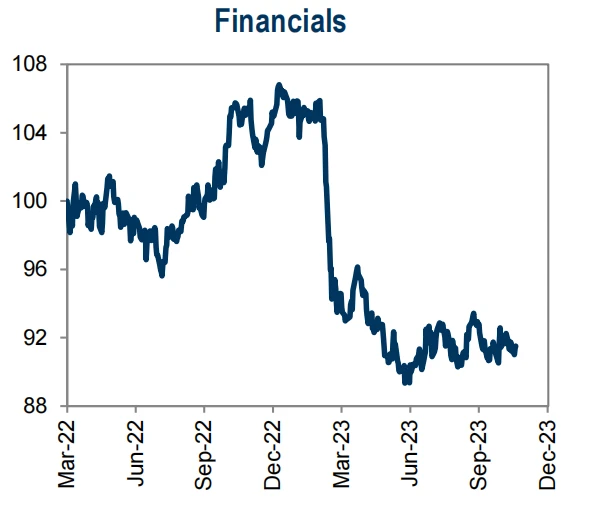

Now we cannot simply classify stocks into growth or value to judge whether the market is pricing future growth, because we can see obvious internal differentiation. For example, consumer cycle stocks and financial stocks, shipping stocks are still pricing typical recessions, while various technology stocks are still pricing in typical recessions. And energy stocks are priced at very little or essentially nothing:

OpenAI board fires CEO Sam Altman

There are two contradictions between the two. One is the controversy between security and commercialization: Since the establishment of OpenAI, there has been controversy about the security and commercialization of AI technology (Altman and Greg Brockman, the other co-founder who resigned this time) belong to the radical faction, while the board members who fired Altman, led by OpenAI chief scientist Ilya Sutskever, belong to the conservative faction). The controversies led to Elon Musk cutting ties with OpenAI in 2018 and a group of employees leaving to found rival Anthropic in 2020.

The second is Altman’s entrepreneurial ambitions: Altman once tried to raise billions of dollars from Middle Eastern sovereign wealth funds to create an AI chip startup to compete with Nvidia, an act that exacerbated conflicts with the board of directors.

This caused Microsofts midday decline to quickly expand to more than 2%, and finally closed down nearly 1.7%, but it had hit record highs in the past few days; if OpenAI becomes controlled by conservatives who resist commercialization, it will undoubtedly be negative for Microsoft. Microsoft CEO Nadella is angry about this dismissal. After all, without Sam, Microsofts control over OpenAI will be further weakened. It is strange that it has not received a board seat after investing 10 billion US dollars, and Microsoft has been anxious to make OpenAIs Commercialization of results. At present, it seems that Ilya Sutskever is very bad at external communication. There was no extra explanation after the incident. It will be difficult to win the support of public opinion if this continues. It is not impossible for the current board members to resign under pressure from all parties.

In addition, Alphabet, Googles parent company, which postponed the release of its self-proclaimed humanitys most powerful model to the first quarter of next year, closed down nearly 1.2%, falling to its highest level since October 24th, which was refreshed in three days (however, the internal strife in OpenAI should be a serious problem for Google AI) Good thing).

In addition, WorldCoin, the cryptocurrency created by Sam, fell, Bittensor (TAO), the AI concept leader on the cryptocurrency track, rose by 25%, and Render (RNDR) rose by 8%. (Do you think you have a chance?)

BX will have achieved certain results but does not include economic aspects.

President Xi came to San Francisco last week with the dual mission of stabilizing Sino-US relations and restoring investor confidence in the Chinese economy. Expectations for the summit itself were not high, but the results lived up to them. Biden described the meeting as real progress, with agreements reportedly reached on military exchanges, fentanyl and AI.

President Xi, who has always been aloof in the eyes of the Western world, showed a softer and more graceful side in San Francisco. After reminiscing with Biden about his first visit to the United States 38 years ago, he publicly accepted an NBA team jersey from the governor of California and said he would send giant pandas to American zoos.

The title of the report given by Wallstreet Journal is Xi fails to reassure U.S. business leaders about Chinas business environment: Foreign capital is fleeing China. During his first visit to the United States in six years, Chinese leader Xi Jinping did not spend much thought on winning back U.S. companies. and Investors believes that President Xi did not mention any possible future measures on trade and investment with the United States, and believes that this speech is relatively general talk. However, some commentators believe that the tendency of this speech is very friendly, even if his speech is just Generalities. “He could have given a more radical and nationalistic speech in defense of China.

In fact, President Xi did say that China would create a “world-class business environment” and improve mechanisms to protect the rights of international investors. We will also take more heart-warming measures, such as improving entry and residence policies for foreigners, he said, adding that access to financial, medical and electronic payment services will become smoother. All this is to make it easier for foreign companies to invest and operate in China. But the problem is that access itself has been relaxed. Not counting the news, foreign investors are currently more concerned about protecting legitimate rights and interests and fair competition, so This is the basis for the view of those who believe that the most important things should be avoided.

Chinese stock market pricing for BX

Global stocks continued to rise last week, but Chinas CSI 300 index had its worst week in about a month. Foreign investors sold a net 5 billion yuan of Chinese stocks, exacerbating the markets decline, with A-shares facing an unprecedented three consecutive years of losses.

Of course its not entirely BXs fault here, with the real estate sector remaining at the heart of Chinas markets deep-seated downturn and becoming a source of concern again last week. Data on Thursday showed new home prices fell the most in eight years in October and the second-hand market posted its biggest fall in nine years.

Global fight against inflation reaches turning point

The latest data last week showed that the UKs consumer price growth fell to 4.6% (expected 4.8%). The euro zones final adjusted CPI growth rate in October slowed sharply to 2.9% year-on-year from 4.3% in September. The announced US CPI of 3.2% has strengthened expectations that central banks may take off the brakes and instead cut interest rates next year. Market mainstream expectations are that the Bank of England will start cutting interest rates in May next year, followed by the Federal Reserve and the European Central Bank in June.

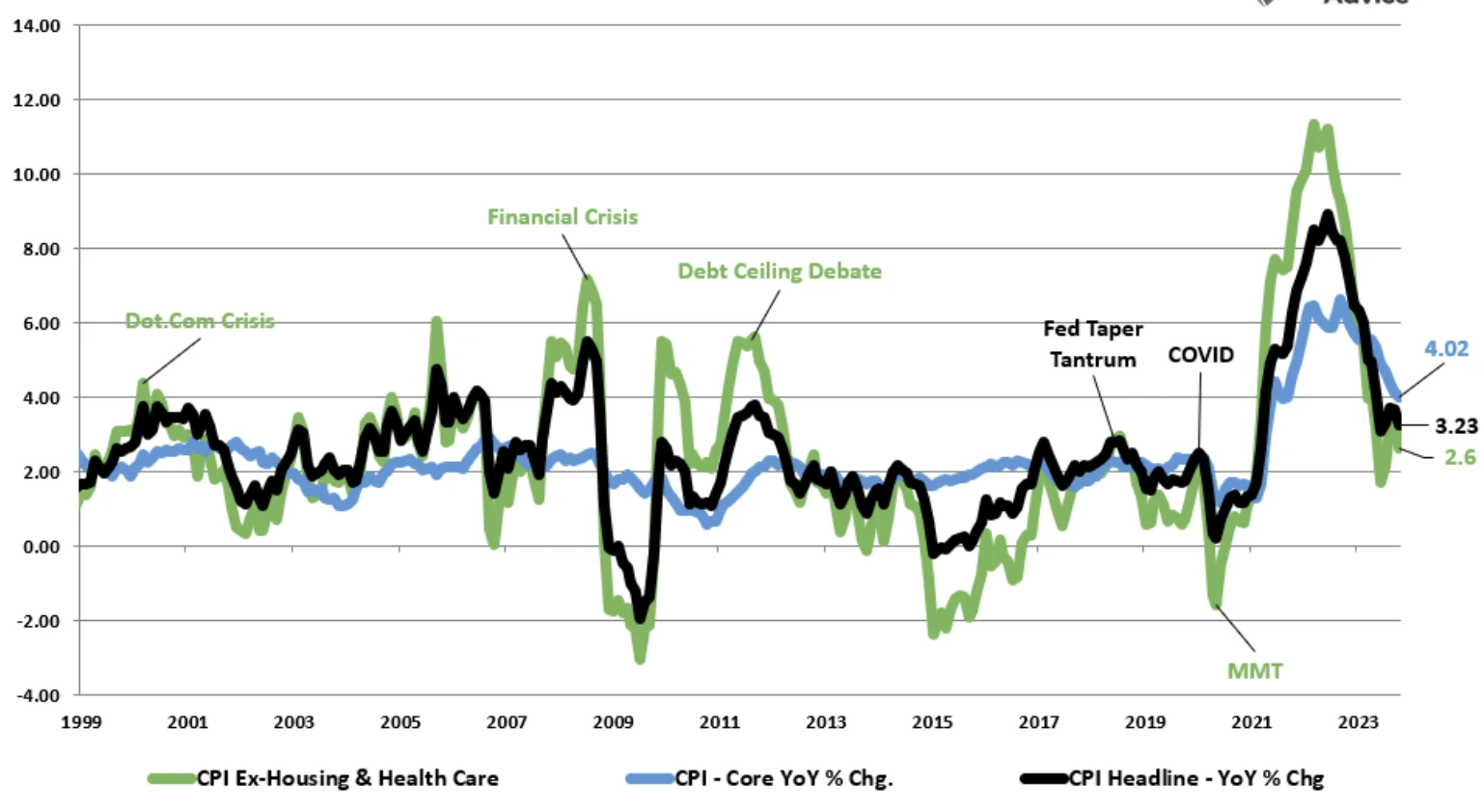

For most people, housing and medical expenses are fixed through contracts over a period of time. Taking the United States as an example, after excluding these two items, the monthly inflation rate faced by households has dropped to 2.6%:

Walmart worries about looming deflation

At the investor conference, Walmarts CFO used the word deflation to describe the current U.S. price situation, noting that we may be about to experience a period of deflation for several months. The price of general goods has been falling, and in the past few weeks or several The monthly decline is steeper than the previous trend...We may see deflation or price declines in dry goods and consumer goods in the coming weeks and months. No one knows the price of everyday items better than the management of major supermarkets. fluctuation. When they use the word deflation, it means that at least some part of the market is currently experiencing a decline in the price index. The CFO also said they saw some worrying signs in the last two weeks of October, with both sales and volumes showing weaker momentum in late October than the rest of the third quarter.

Wal-Mart, McDonalds, etc. are typical consumer stocks, and they are in the field of consumer goods. In the high inflation environment in the past two years, consumer companies can use the rise in raw material prices and supply chain interruptions to significantly raise prices and successfully pass on the costs. To consumers, so despite rising costs, most industries have actually increased their profit margins, especially large monopoly companies with advantages that have the initiative to increase prices.

The U.S. PPI released last week cooled more than expected to 1.3% year-on-year, falling 0.5% month-on-month, the largest monthly decline in three and a half years since April 2020.

Buffetts Berkshire Hathaway liquidated consumer stocks including General Motors, Johnson Johnson, Procter Gamble and Mondelez International in the third quarter. The consumer stocks sector currently accounts for only 12%, which is not in line with his self-professed investment philosophy: I like companies with stable operations and brand value, so they can escape the impact of economic fluctuations.

If deflation is not necessarily good for the stock market

If the Fed starts to cut interest rates from the current high interest rate level because of the rapid decline in prices -

Impact on the US dollar (highly likely to be negative):

Cutting interest rates means monetary policy becomes more accommodative, which tends to reduce foreign investors demand for U.S. dollar assets and therefore may cause the U.S. dollar to depreciate. Unless a major crisis occurs, which may trigger safe-haven demand, this will also be temporarily positive for the US dollar.

Impact on U.S. Treasuries (generally positive):

A rate cut will almost certainly lead to a fall in Treasury yields, which will increase the market price of Treasury bonds. As a result, U.S. Treasuries, including most high-grade fixed-income products, tend to perform well during periods of interest rate cuts.

Impact on the stock market (uncertain):

The stock markets reaction depends on the reasons and context for the rate cut. If the interest rate cut is to deal with the risk of an economic slowdown or recession, it may not directly benefit the stock market initially, because the market may be more concerned about the deterioration of economic fundamentals. Over the longer term, however, rate cuts typically lower companies borrowing costs and spur economic growth, which could ultimately support stock market gains.

Impact on commodities (uncertain):

The reaction in commodity markets was equally mixed. On the one hand, a weaker dollar could increase the price of U.S. dollar-denominated commodities. On the other hand, if the rate cut is due to concerns about an economic slowdown, it could mean less demand for goods, putting pressure on commodity prices.

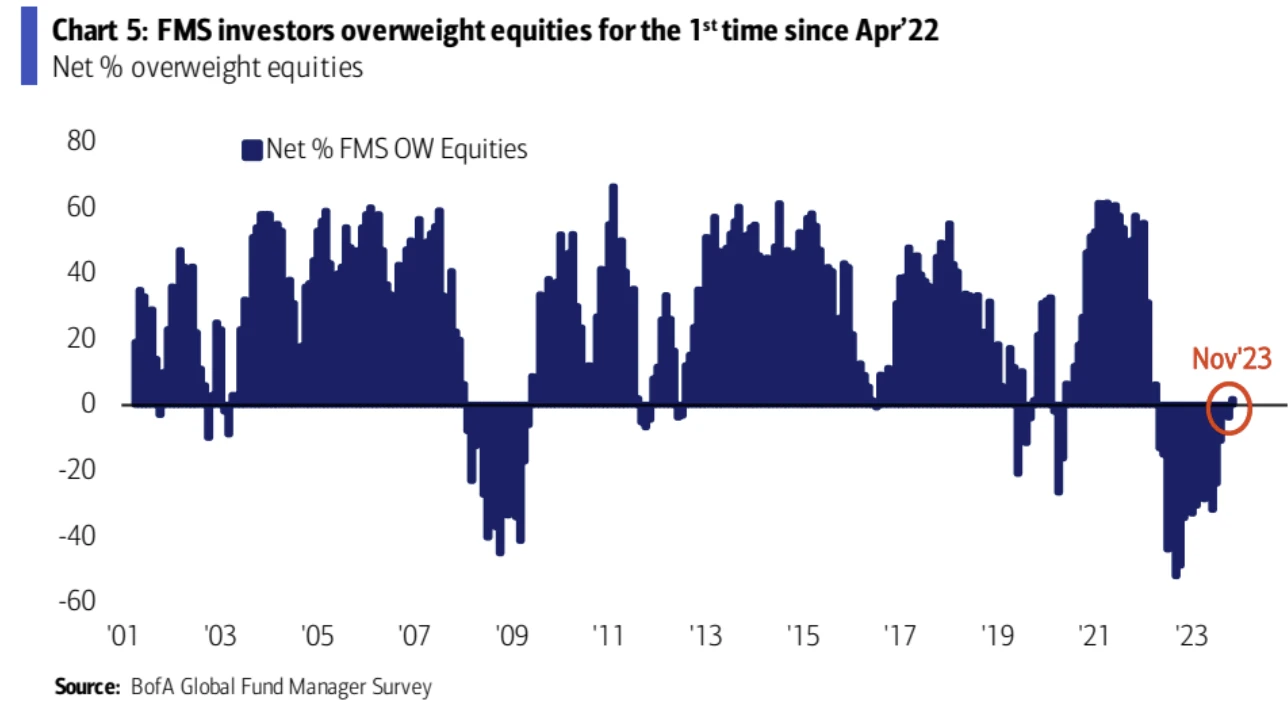

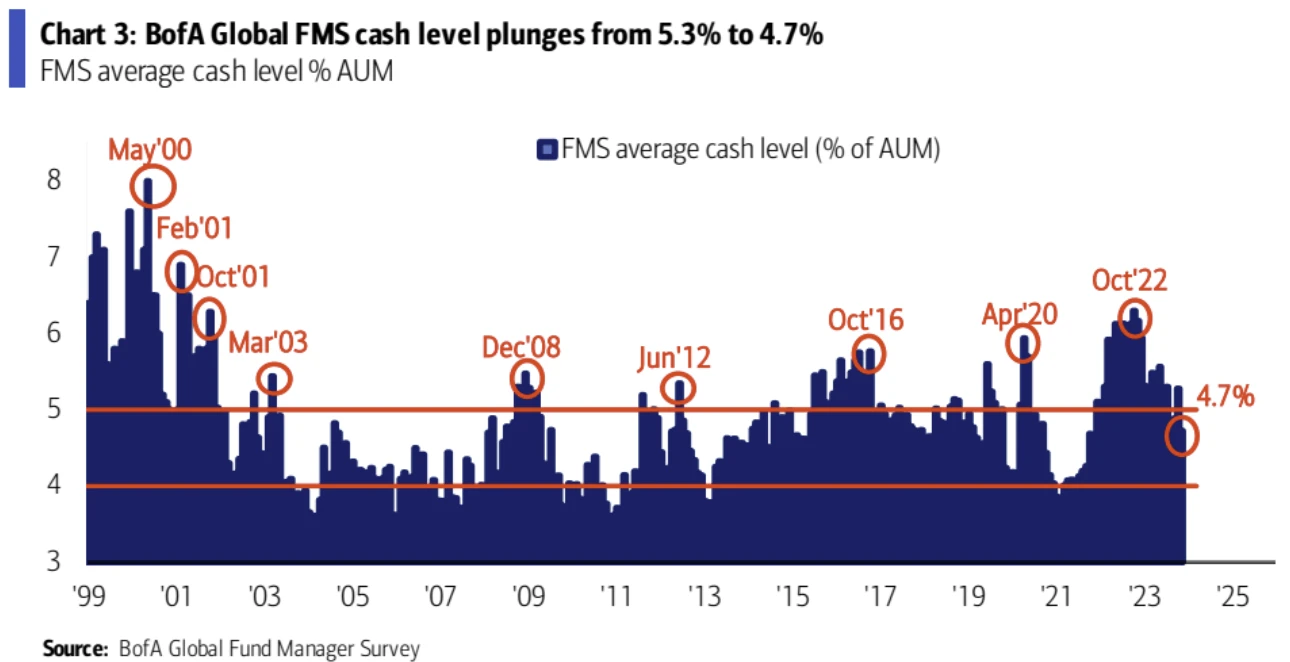

Bank of America Fund Manager Survey (FMS)

Investors reduced their cash holdings and increased their bond allocations, becoming overweighted in stocks for the first time since April 2022:

Cash levels fell to 4.7% from 5.3%, the lowest level since November 2021 and the largest drop since January this year. Cash levels of 4.7% are still slightly above the long-term average and considered neutral. A cash balance below 5% also equates to a buy signal disappearing here at Boa. If cash balances continue to fall below 4%, the FMS cash rules will issue a sell signal, reflecting investors further accumulation of risky assets and overly optimistic economic prospects:

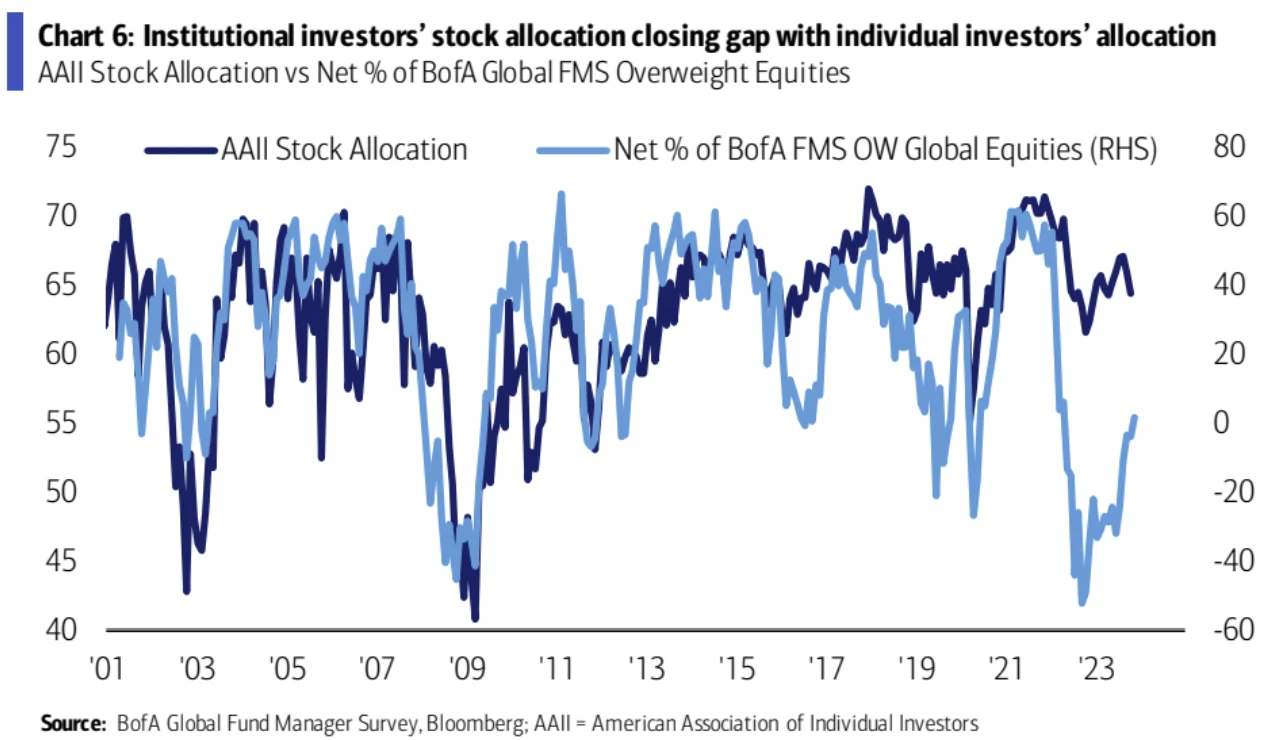

Individual investors are currently significantly more bullish on stocks than institutional investors. But the gap between the two has narrowed this year, and institutional investors pessimism about the stock has improved. AAII data shows that individual investors are currently 64% long in stocks, while the FMS survey shows that institutional investors are currently net 2% long in stocks:

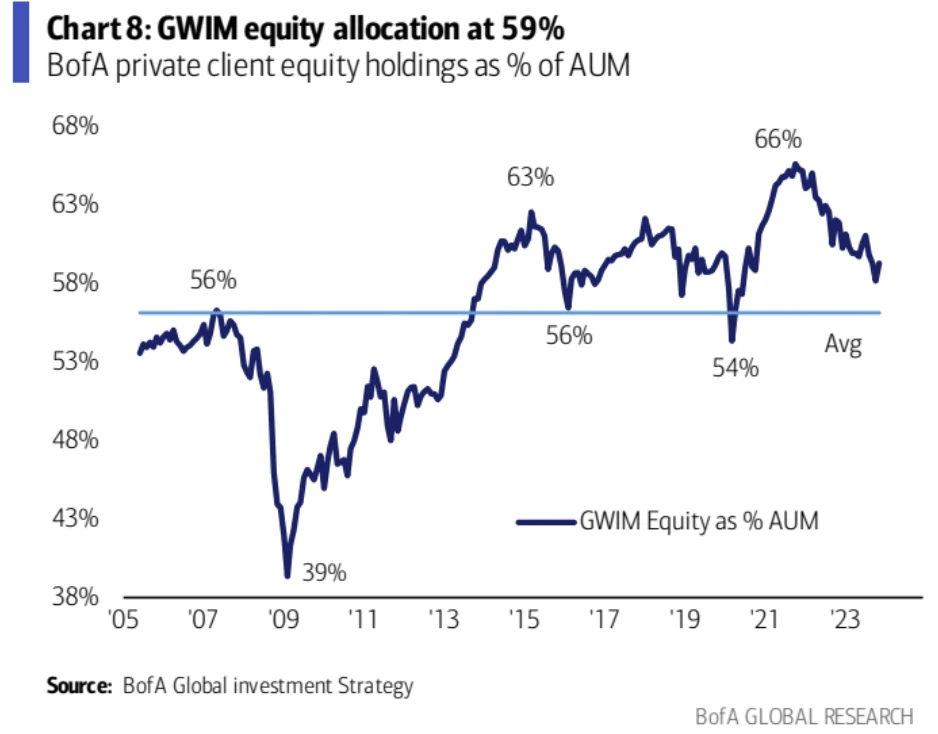

Supplementing a Bank of America Private Bank client survey, stock holdings currently account for 59% of AUM. Although it is higher than the average of 56% from 2005 to the present, there has been no period below this level in the past ten years except for the new crown epidemic:

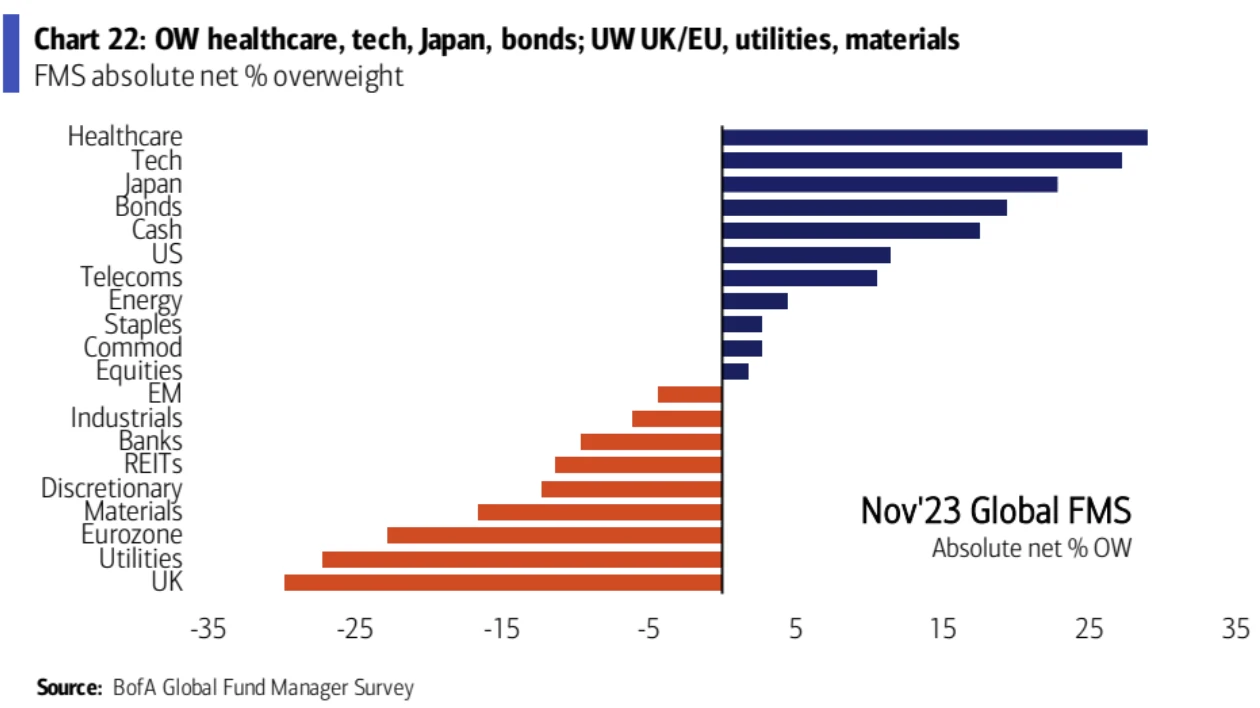

Investors are overweight technology stocks and pharmaceutical stocks and underweight European stocks and utility stocks.

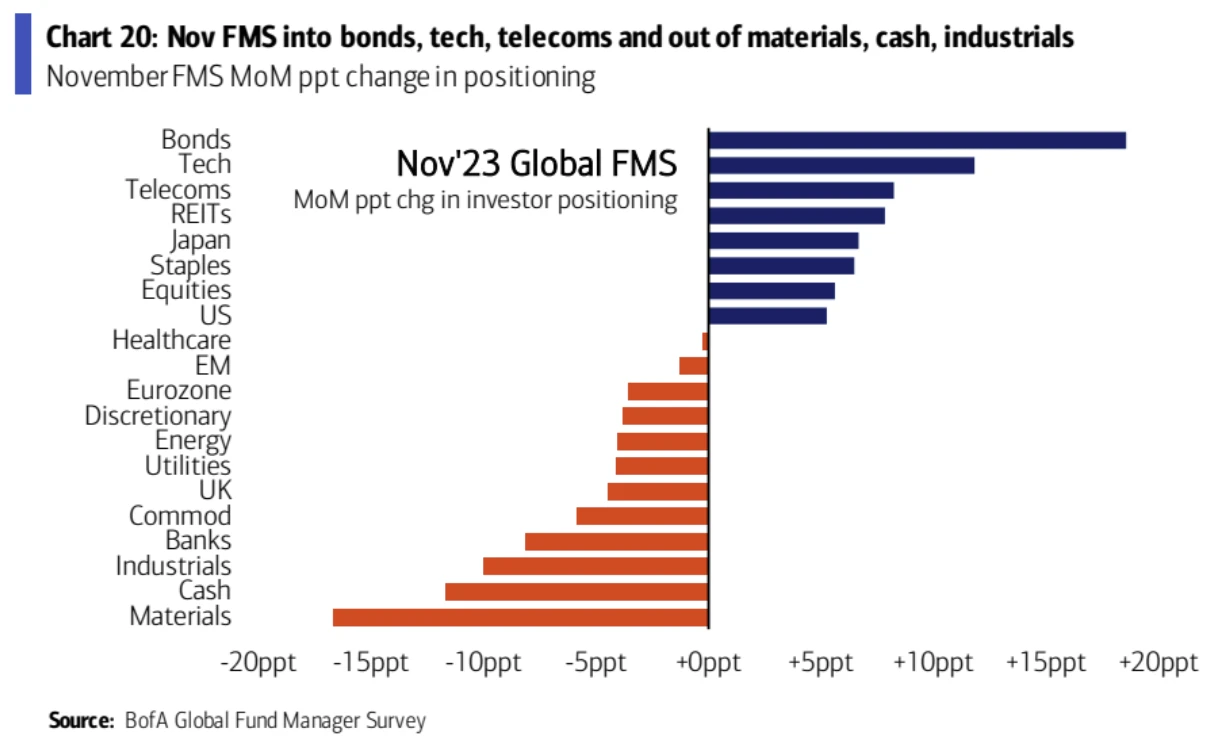

The biggest change in positions this month is the increase in holdings of bonds, technology, and telecommunications, while sticking to raw materials, cash, and industrial stocks:

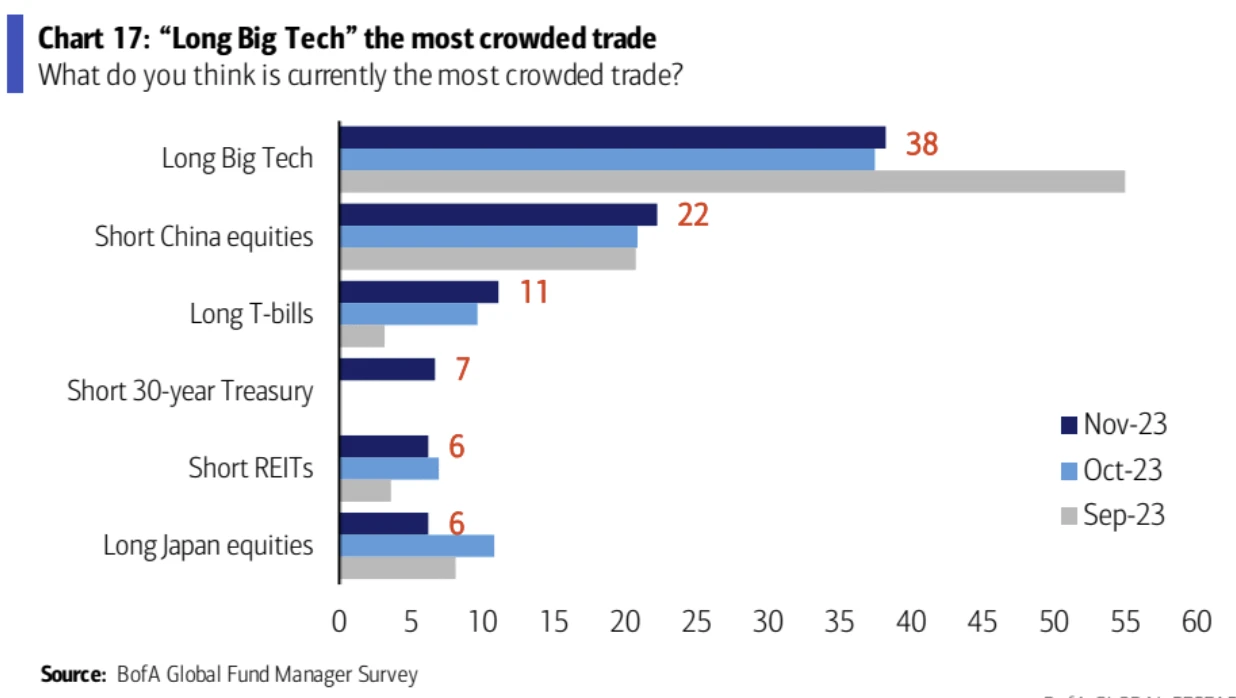

The most crowded trading positions are long cap tech stocks, short China stocks and long short-term Treasury bonds

Positions and Fund Flow

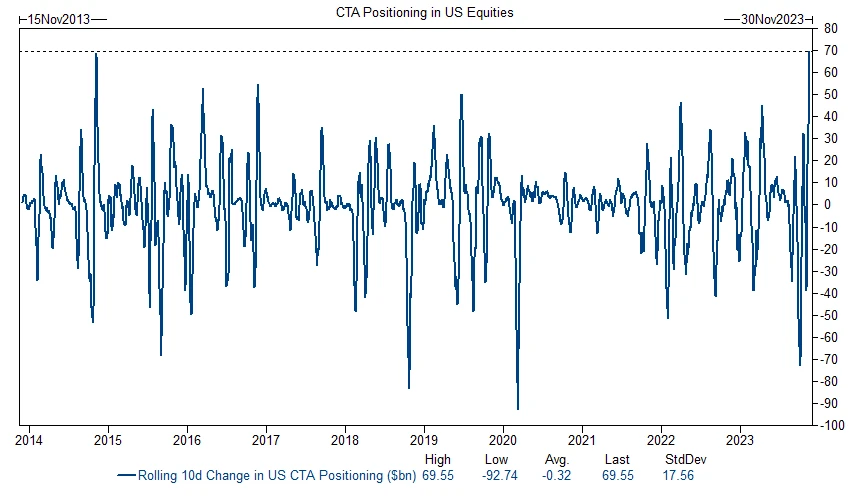

According to Goldman Sachs, In the past 10 days, CTAs have purchased nearly $70 billion in U.S. stocks... This is the largest 10-day purchase on our record.

Goldman Sachs estimates that about $140 billion in global short positions have been unwound since the beginning of the month. If nothing else, expect buying to continue for at least 1 week. There is greater need to close positions in some markets, such as small stocks that still require more buying and closing.

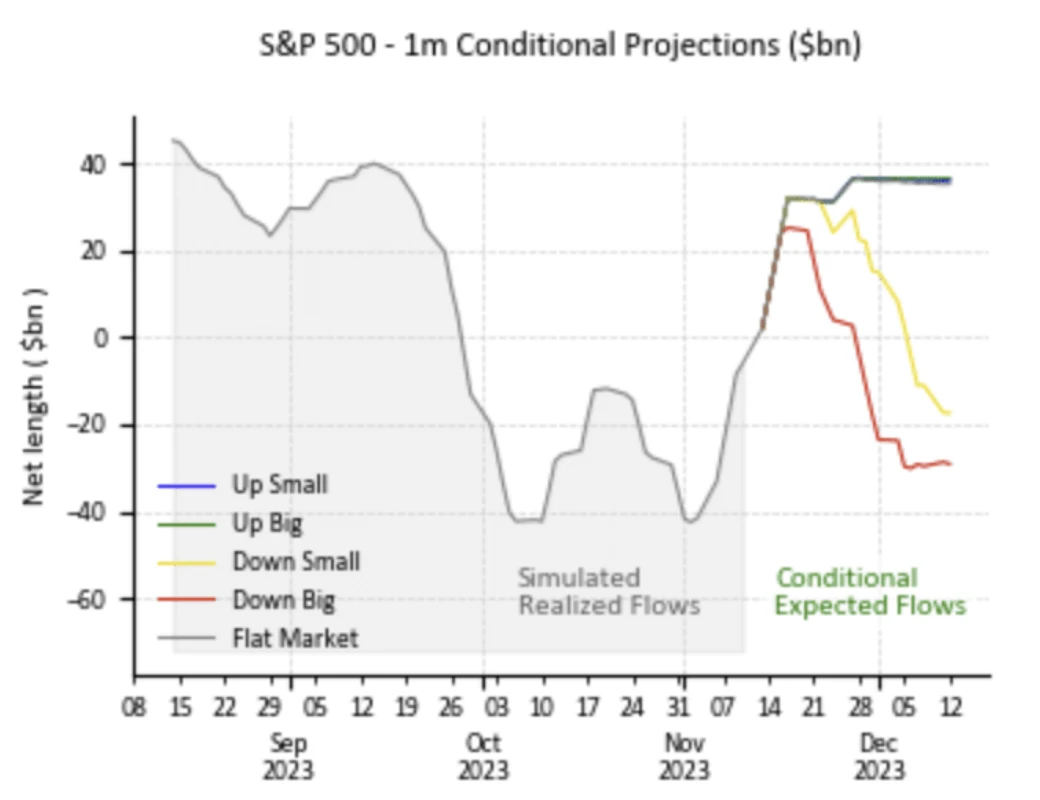

Of course, the price is that after this large-scale buying frenzy, CTAs position is now more balanced, and the momentum for subsequent replenishment may be limited:

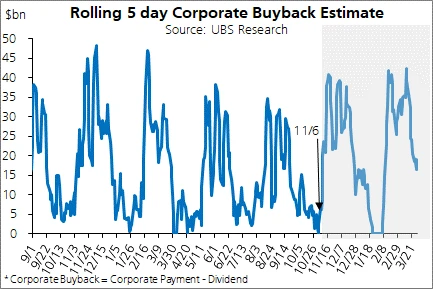

However, we are currently in the midst of a period of intensive stock repurchases, expected to last until mid-December, which will result in very strong supplementary buying, with repurchases expected to reach $40 billion last week:

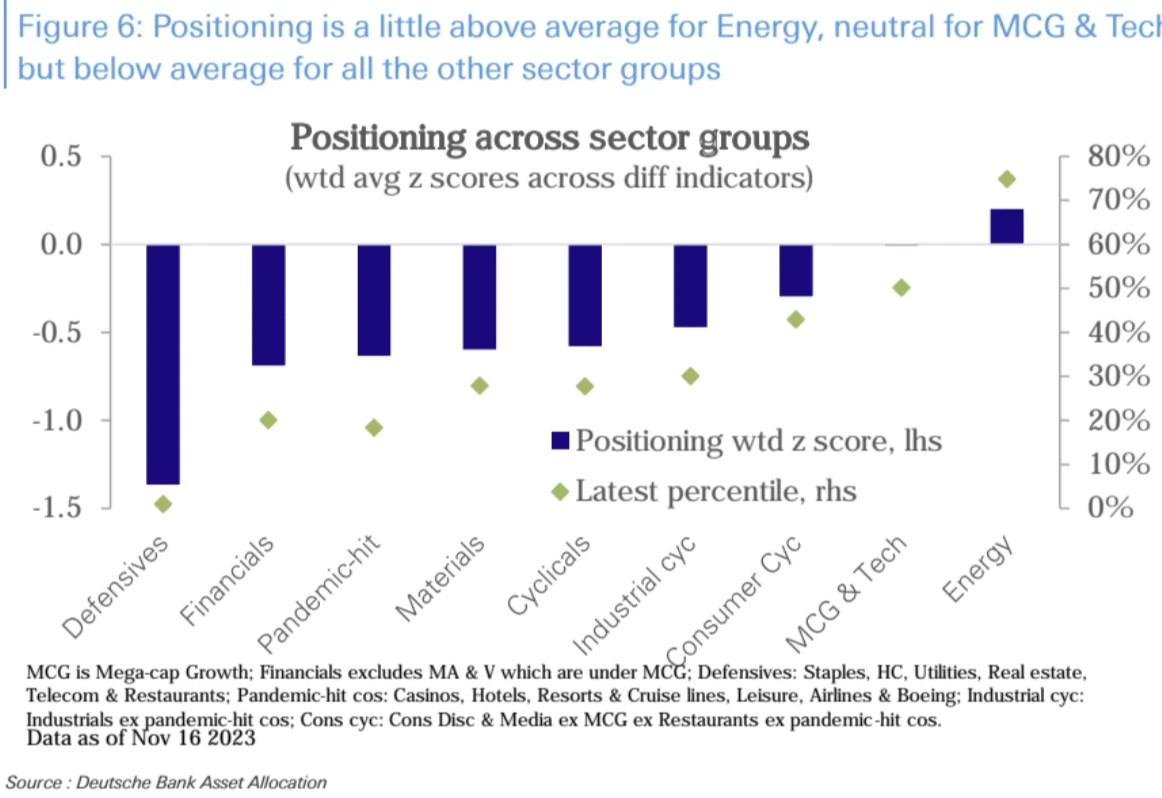

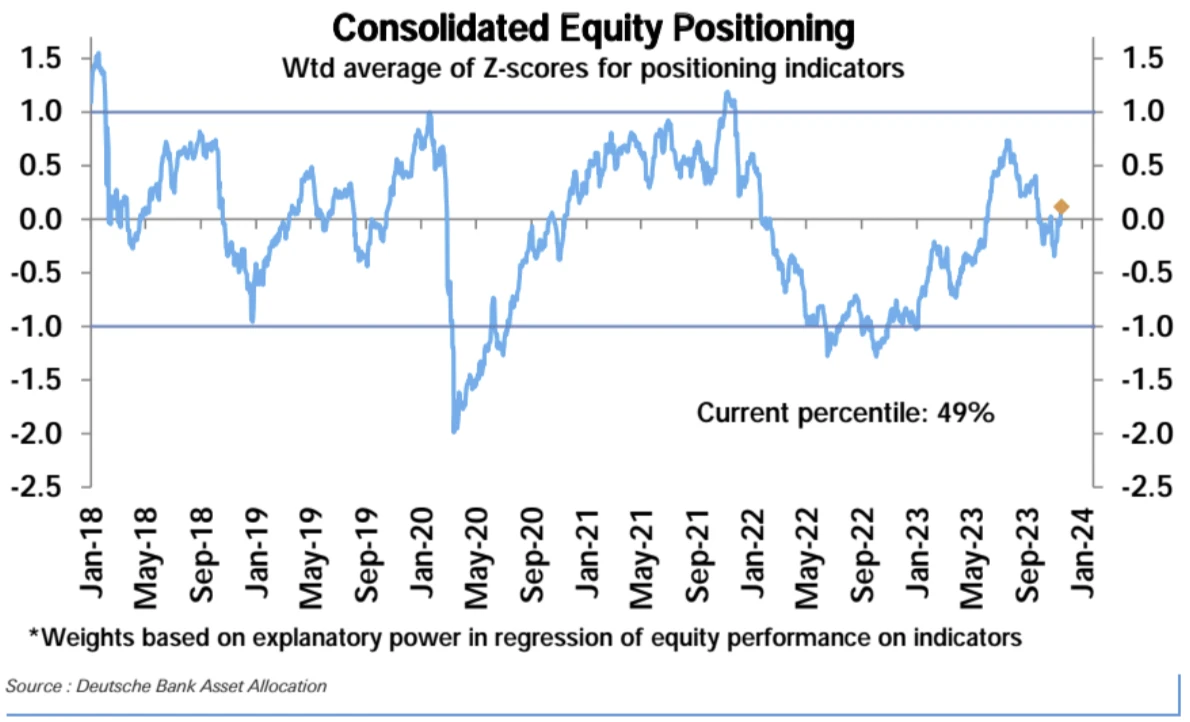

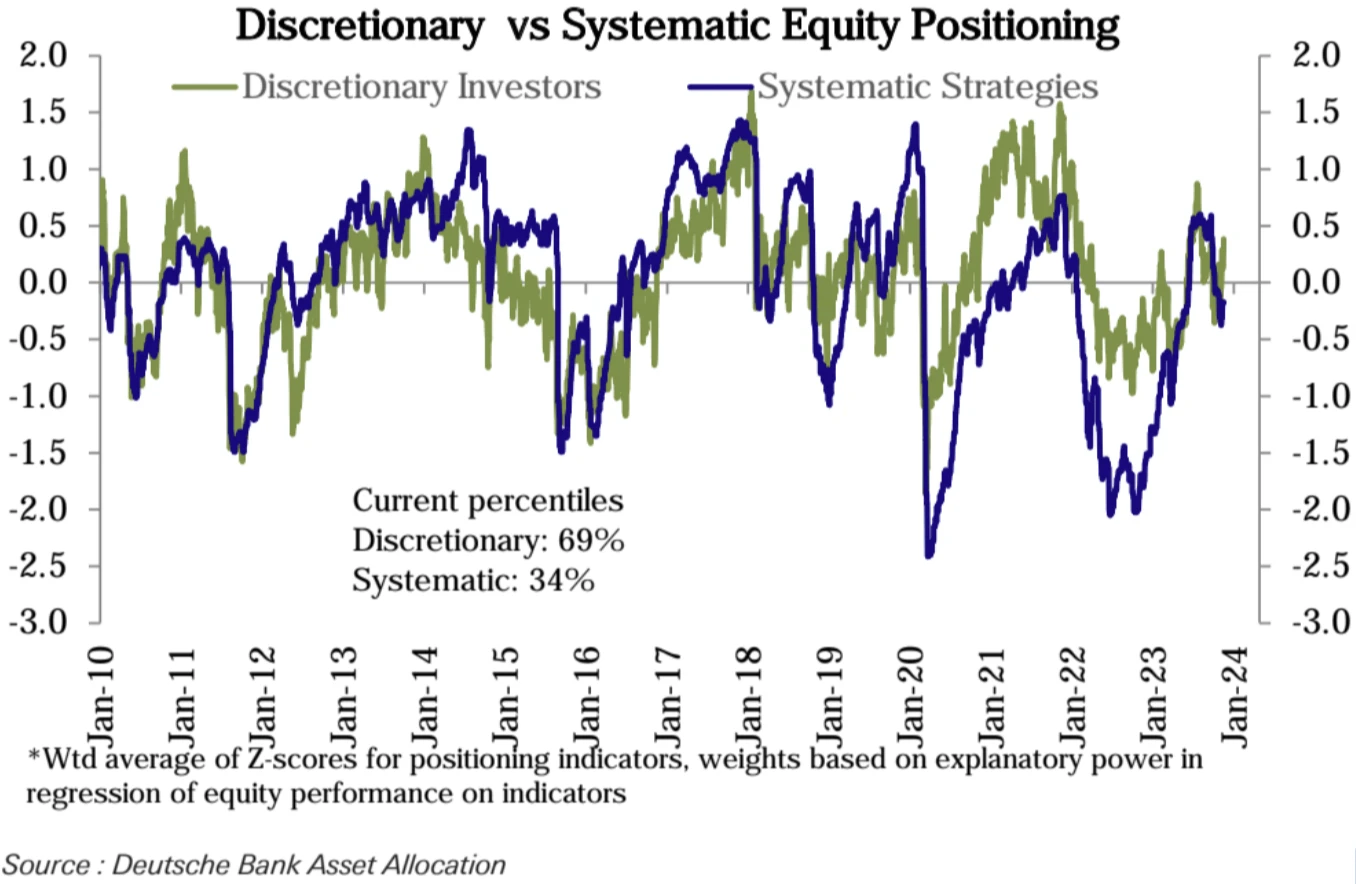

According to statistics from Deutsche Bank, the overall position of U.S. stocks has risen sharply since the end of October, but its level is still at the 49th percentile. The position of the independent strategy has rebounded significantly to be slightly overweight (69th percentile), while the position of the systematic strategy has rebounded significantly to slightly overweight (69th percentile), while the position of the systematic strategy has rebounded sharply. The position was revised up slightly to remain underweight (34th percentile).

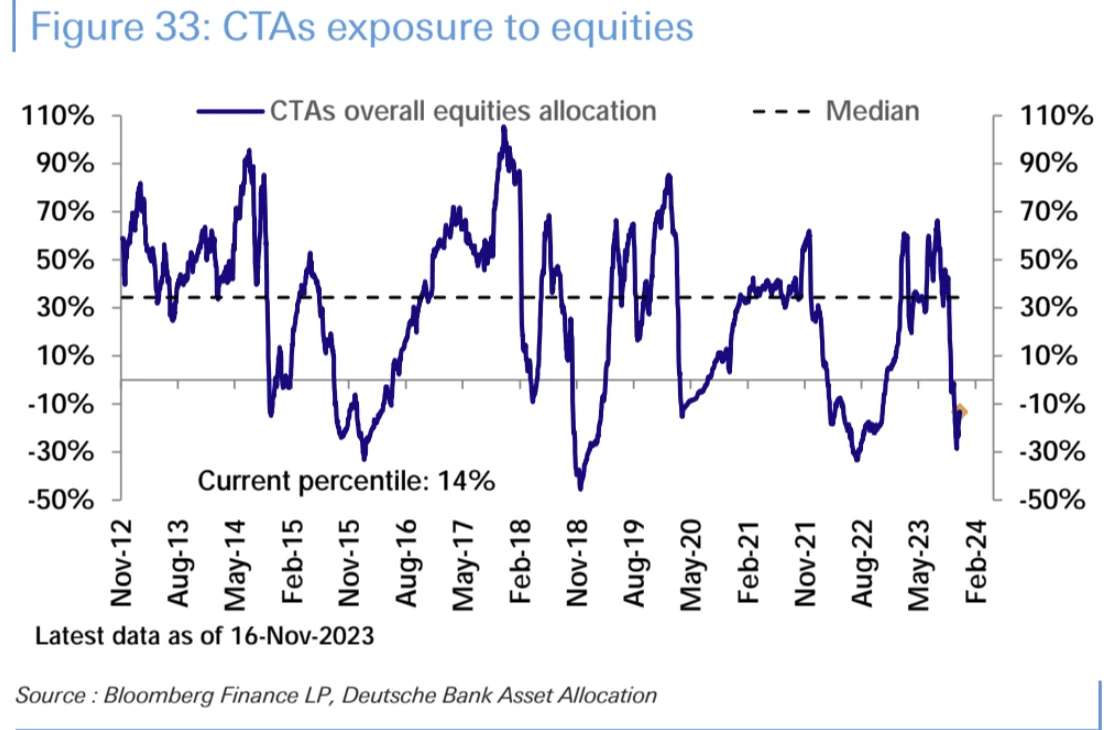

CTA capital positions have rebounded to a certain extent:

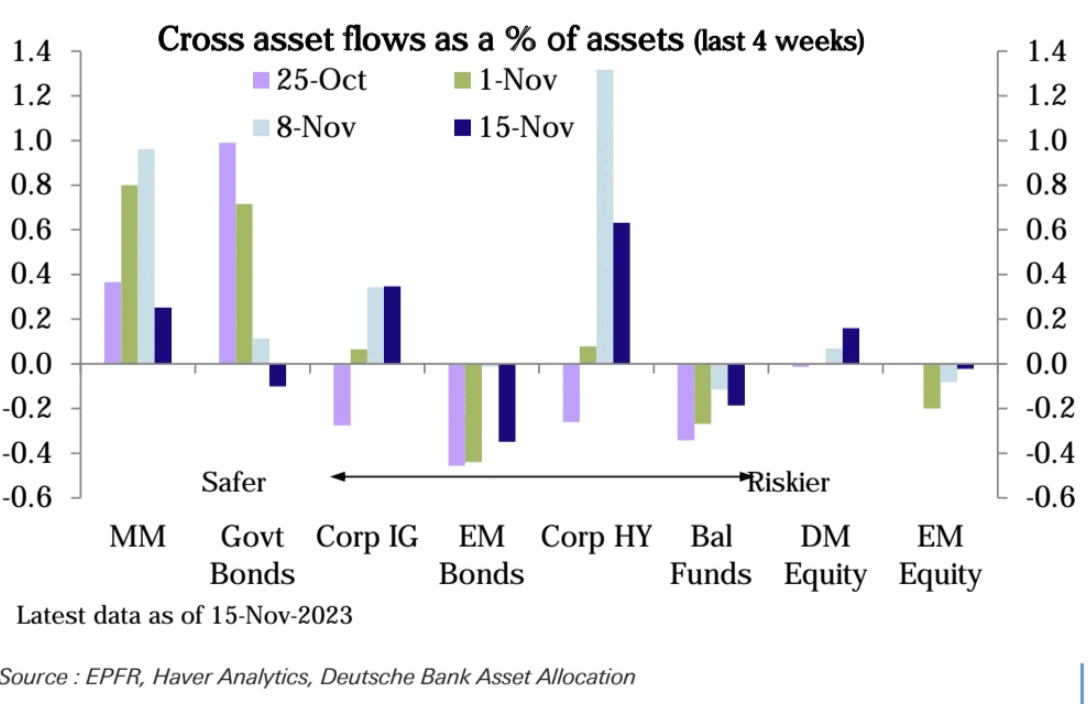

Equity funds ($23.5 billion) received their strongest inflows in two months, mainly from the United States ($25.8 billion), while other regions saw outflows. Money market funds ($20.5 billion) saw fourth week of inflows, but not at the pace of recent times

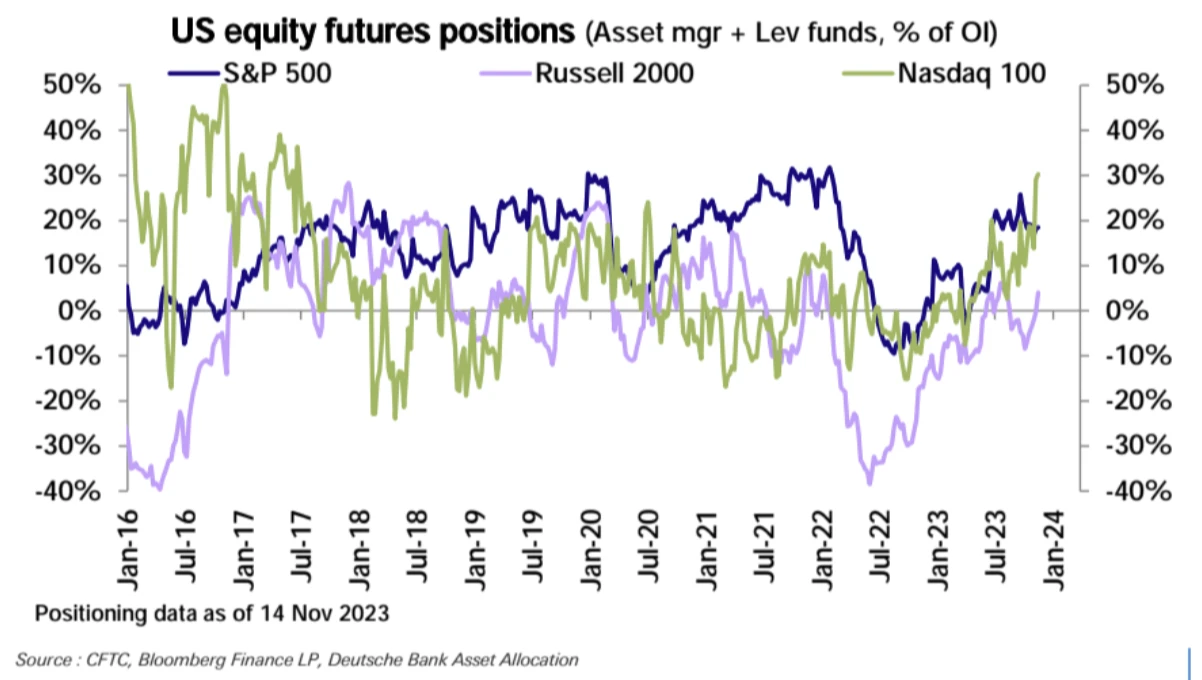

CFTC data (as of November 14), US stock net longs have increased for two consecutive weeks, and major indexes have increased

In bonds, overall net shorts increased as increases in 10yr shorts offset decreases in other durations

Aggregate USD positioning remains close to neutral, with sharp net-long additions to the euro offset by reductions in longs in other currencies

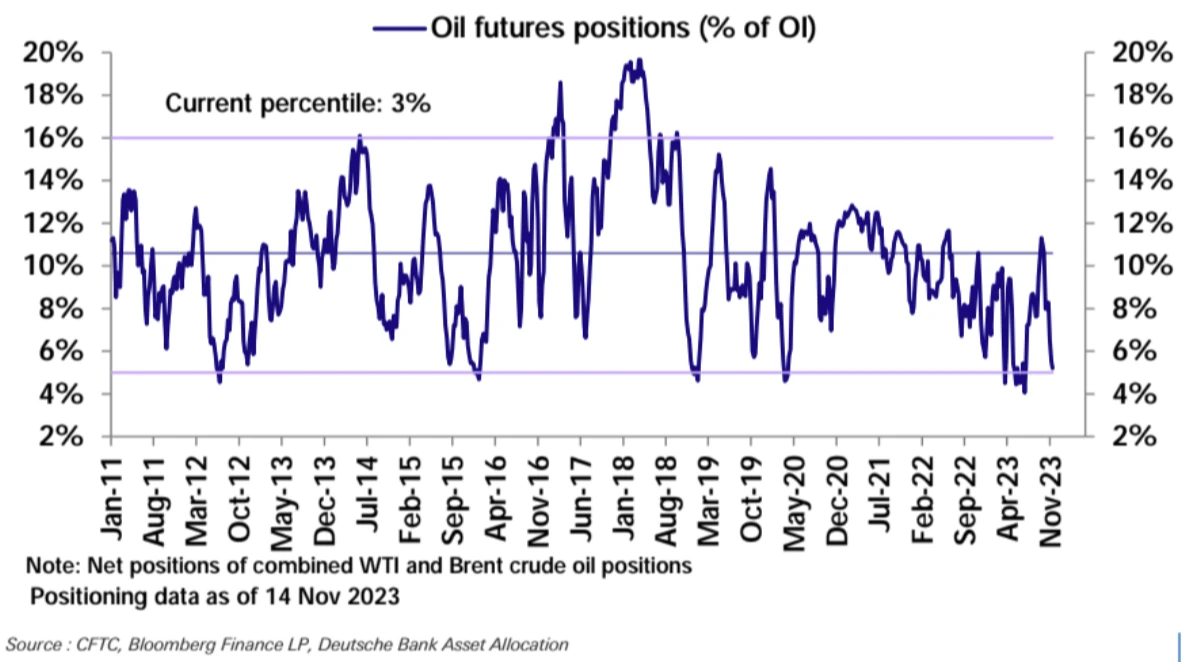

In commodities, investors further reduced their net long positions in oil to historic lows. Copper shorts edge up this week, gold bulls drop sharply from highs

mood

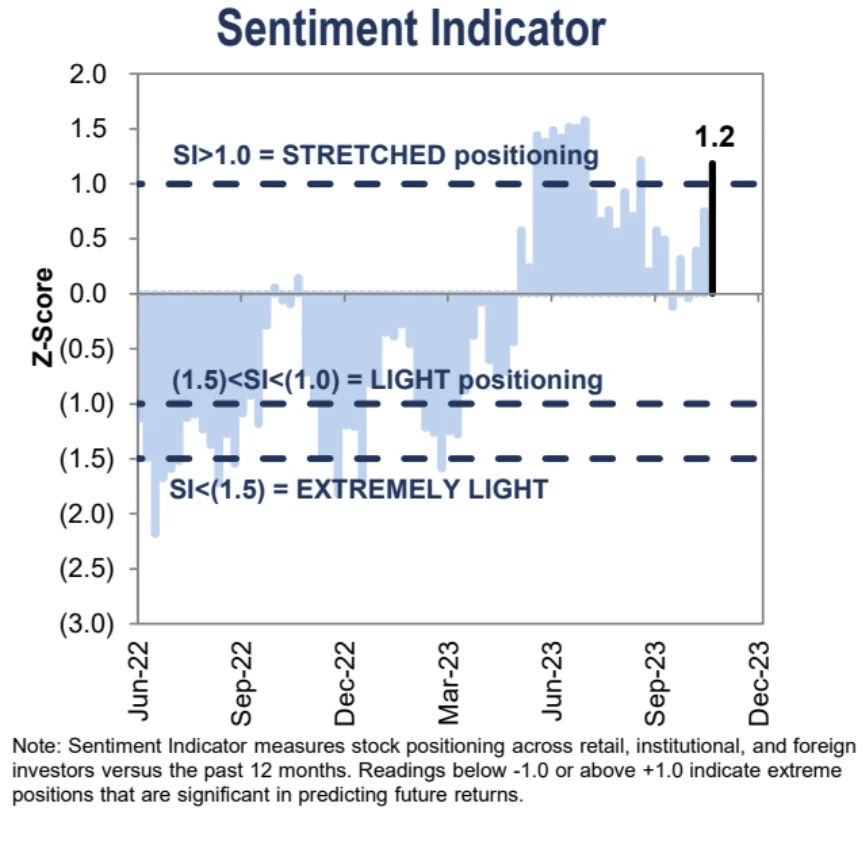

Goldman Sachs: Extreme

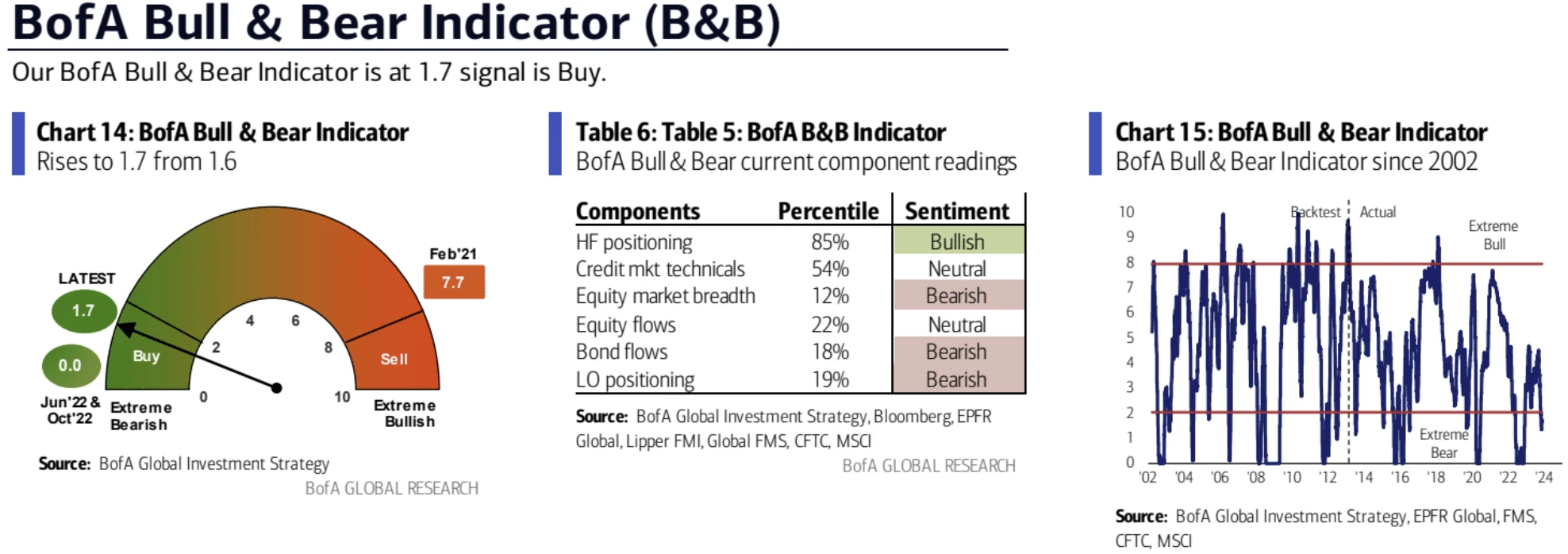

BofA Little Changed: Buy

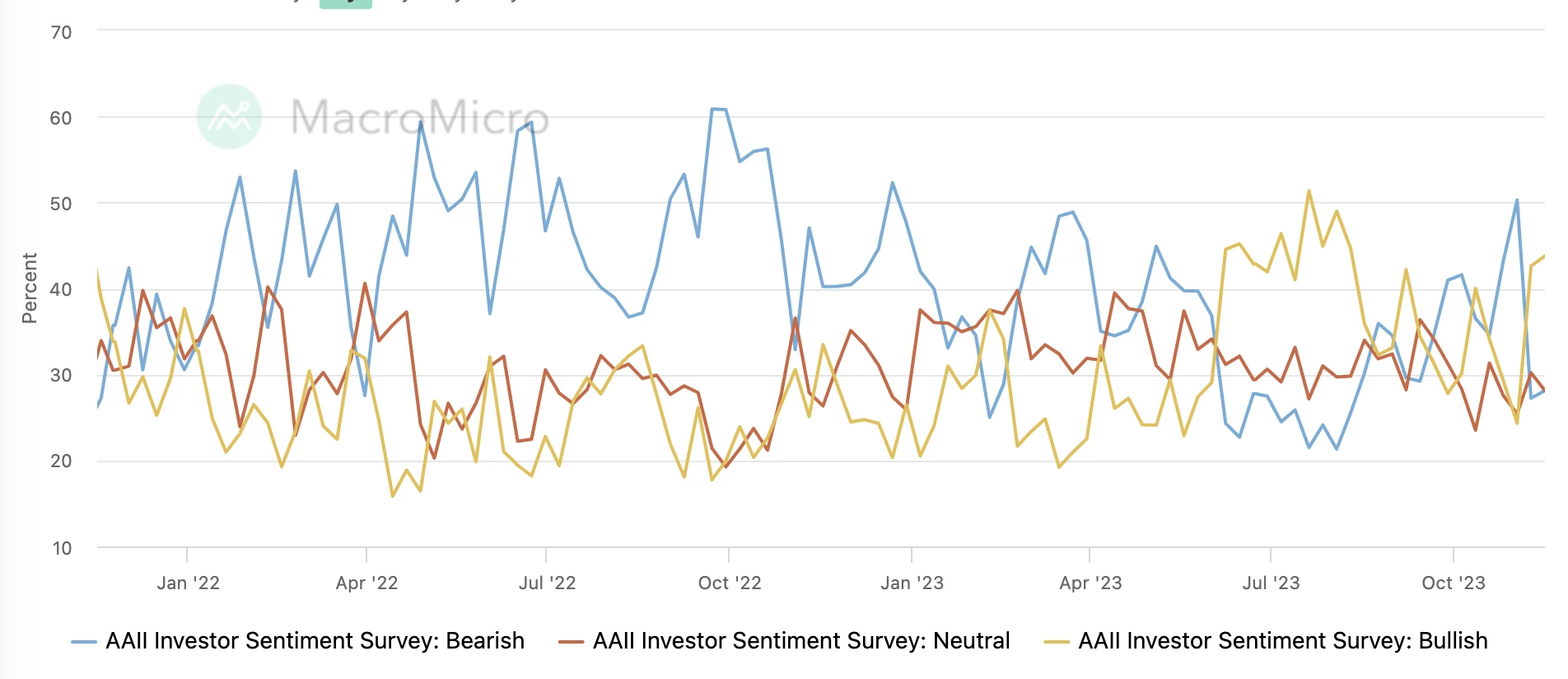

AAII Little Changed: Bullish

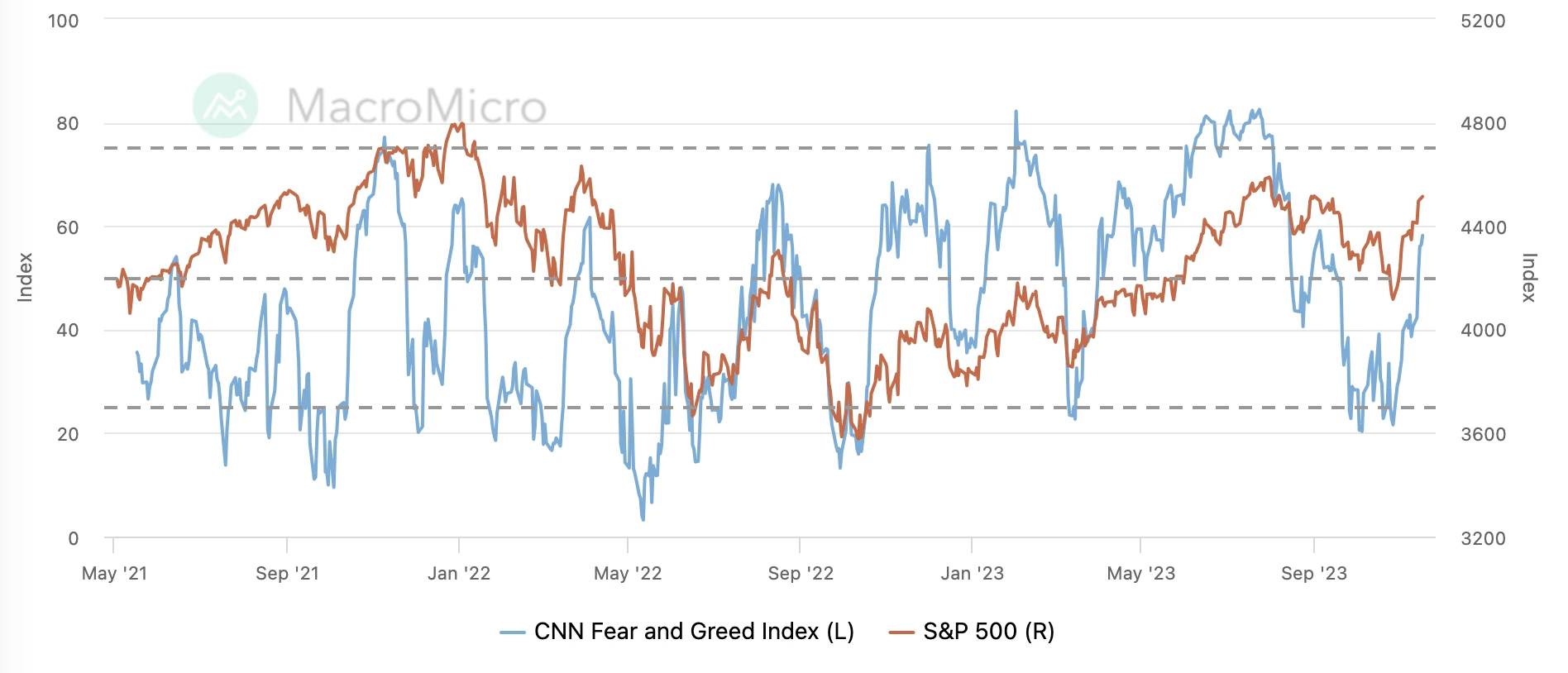

CNN surges: bullish

Follow this week

On Thursday, November 23, the U.S. stock market will be closed for Thanksgiving Day, and will only open for half a day on Friday (many people take a full day off). Therefore, Friday is usually one of the days with the lowest trading volume in the U.S. stock market. Not surprisingly, the market will be around this week. Last weeks closing position fluctuated within a narrow range.

The financial reporting season is coming to an end, and AI leader Nvidia will have its finale. Wall Street expects Q3 revenue to be US$16.079 billion, a year-on-year increase of 171%; adjusted net profit is US$8.419 billion, a year-on-year increase of 478%. The average analyst price target is $628.68.

This weeks auction of 16 billion 20-yr Treasury bonds is seen as another test of the markets supply of U.S. debt. If yields rise again due to poor auction results, this could even trigger a softening of the Feds stance, which might not be a bad thing in the medium term.