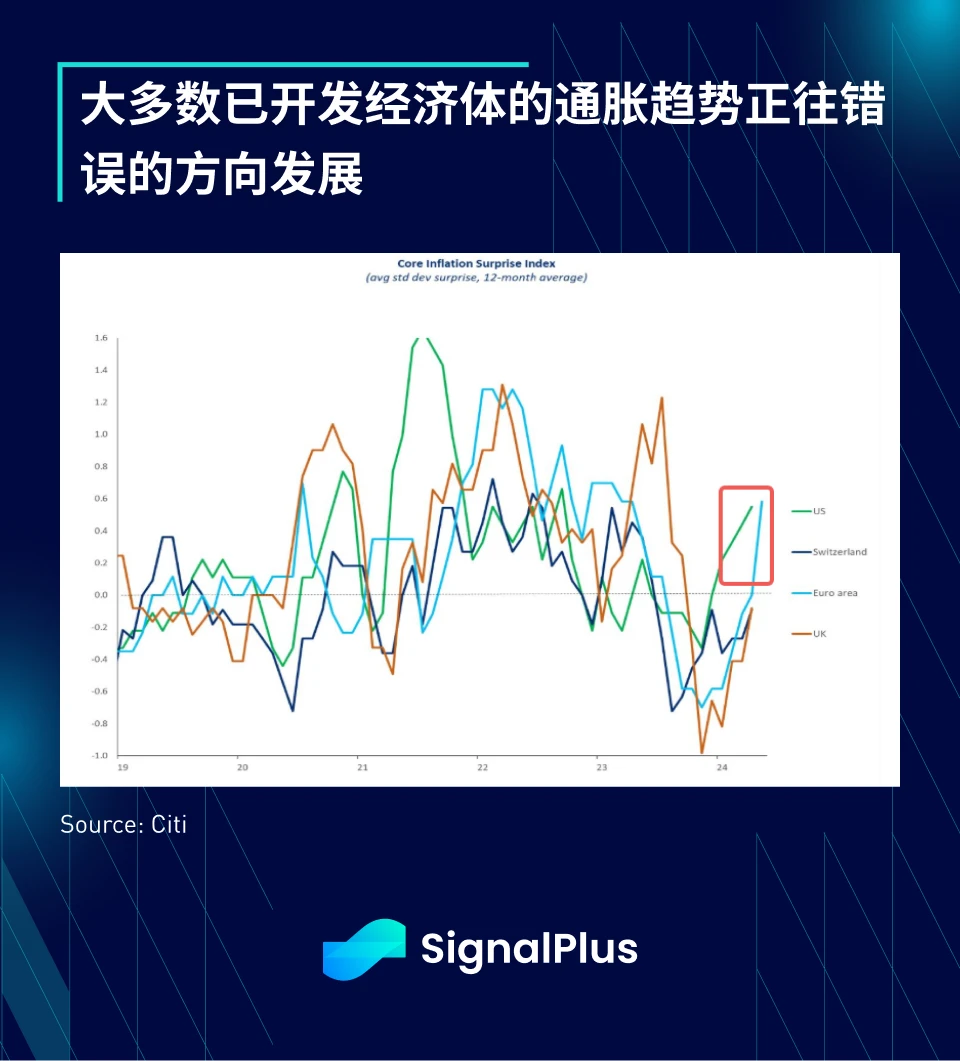

Last week’s economic data triggered quite a bit of rethinking, with US data finally returning to where it was at the start of the first quarter (GDP revised down, consumption falling), while global inflation momentum started to unexpectedly pick up, with Eurozone HICP re-accelerating to 2.9% year-on-year (from 2.7% previously).

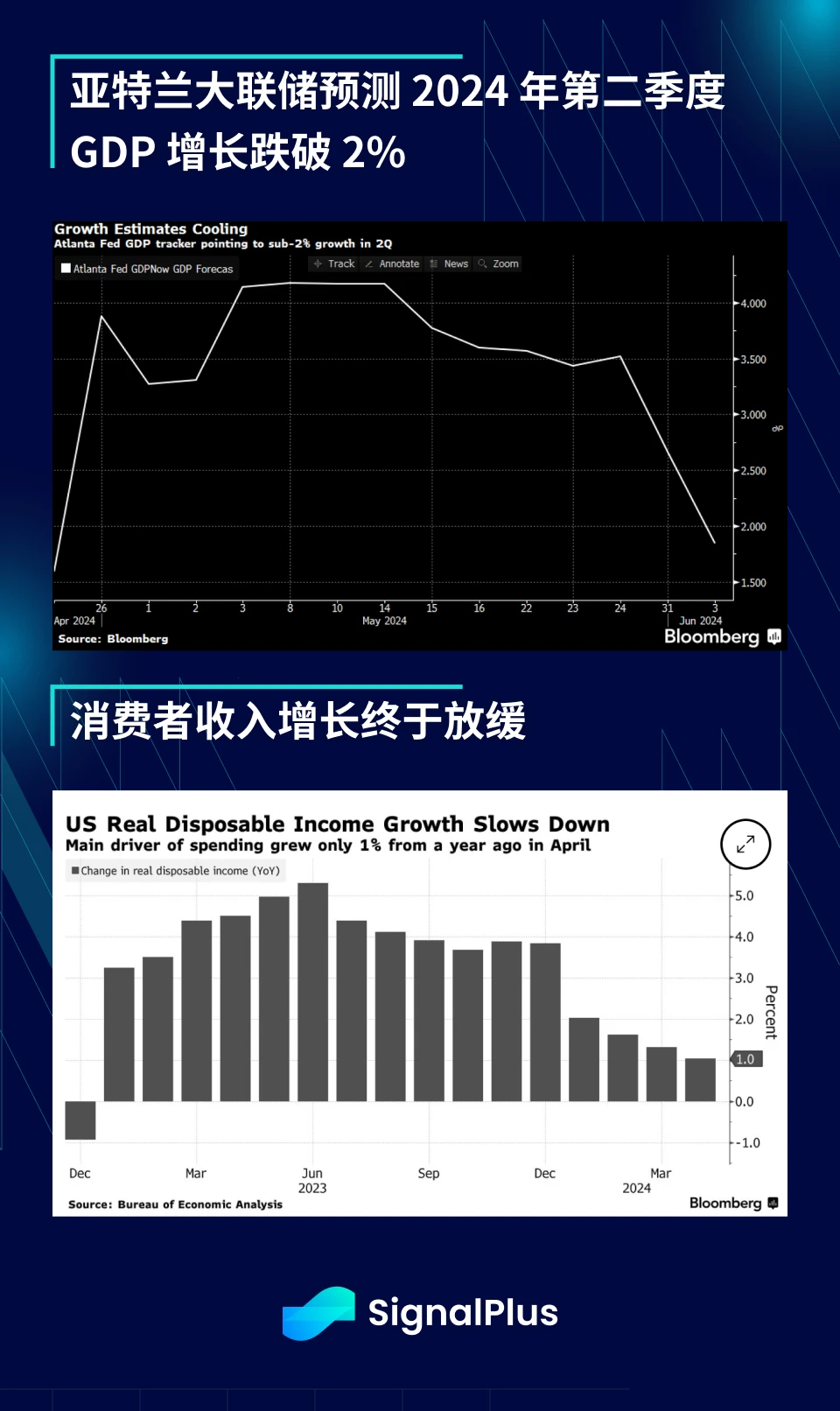

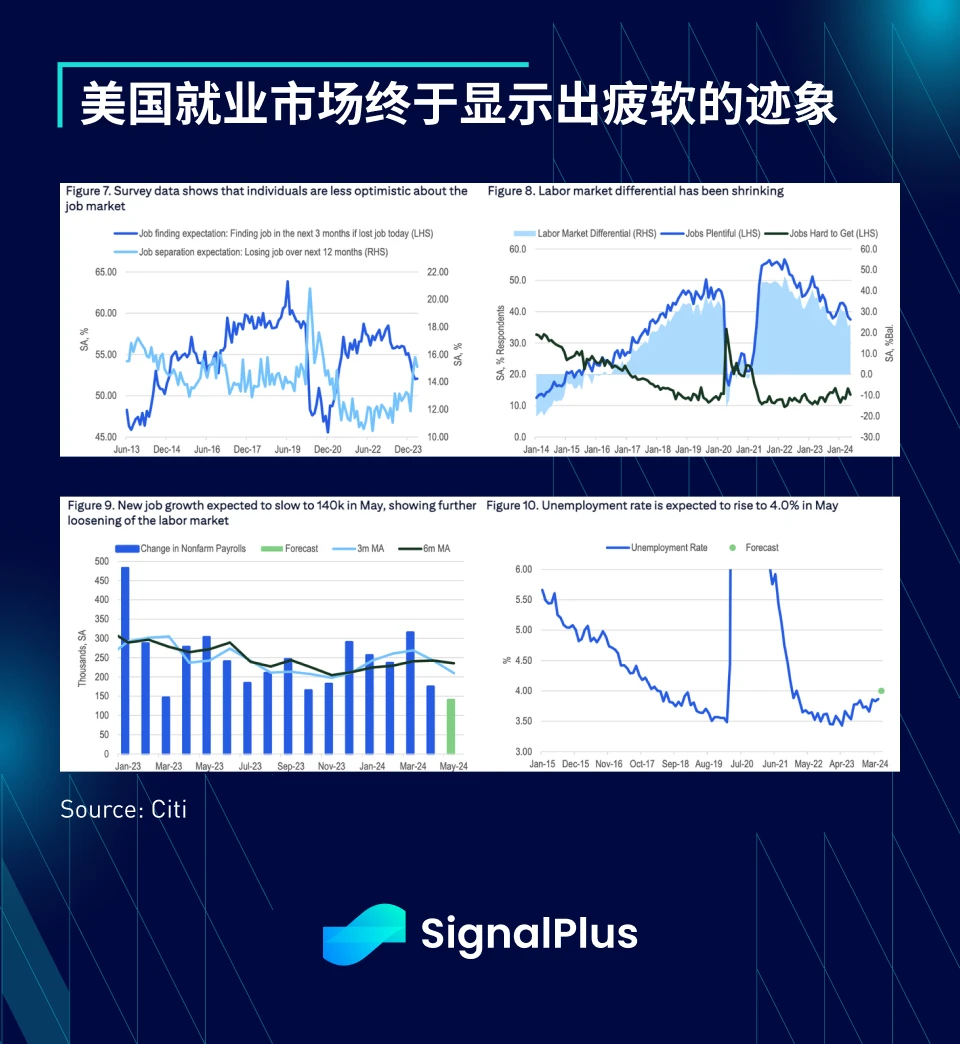

The slowdown in US economic data is now too widespread to ignore, with the Atlanta Feds GDP forecast now falling below 2% and real disposable income growth slowing to below 1%. In addition, rising credit card delinquencies, higher rental costs, and a weak job market all point to a weaker US economy ahead of the election, while the Fed is still dealing with the thorny issue of high inflation and has few meetings left before November.

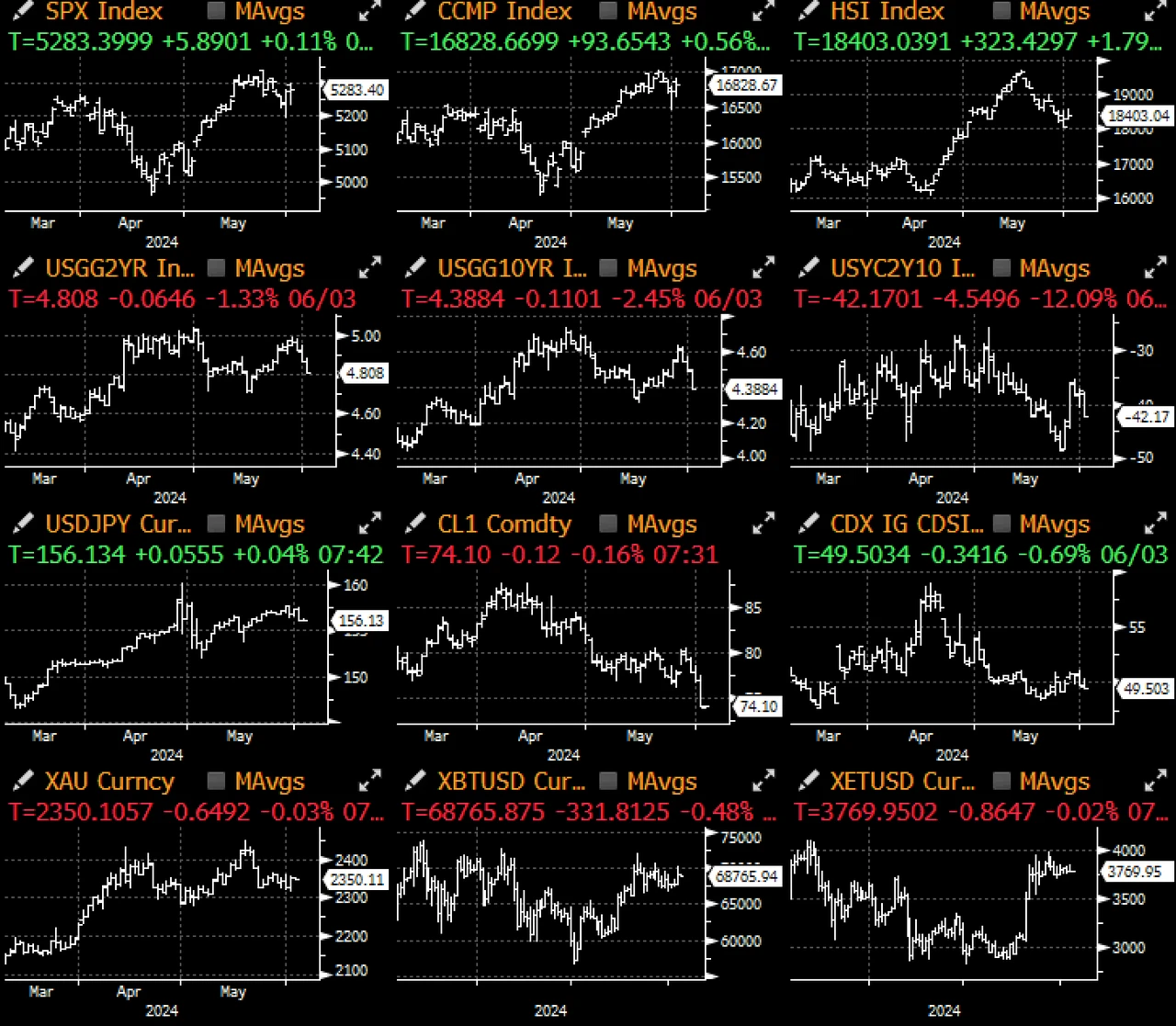

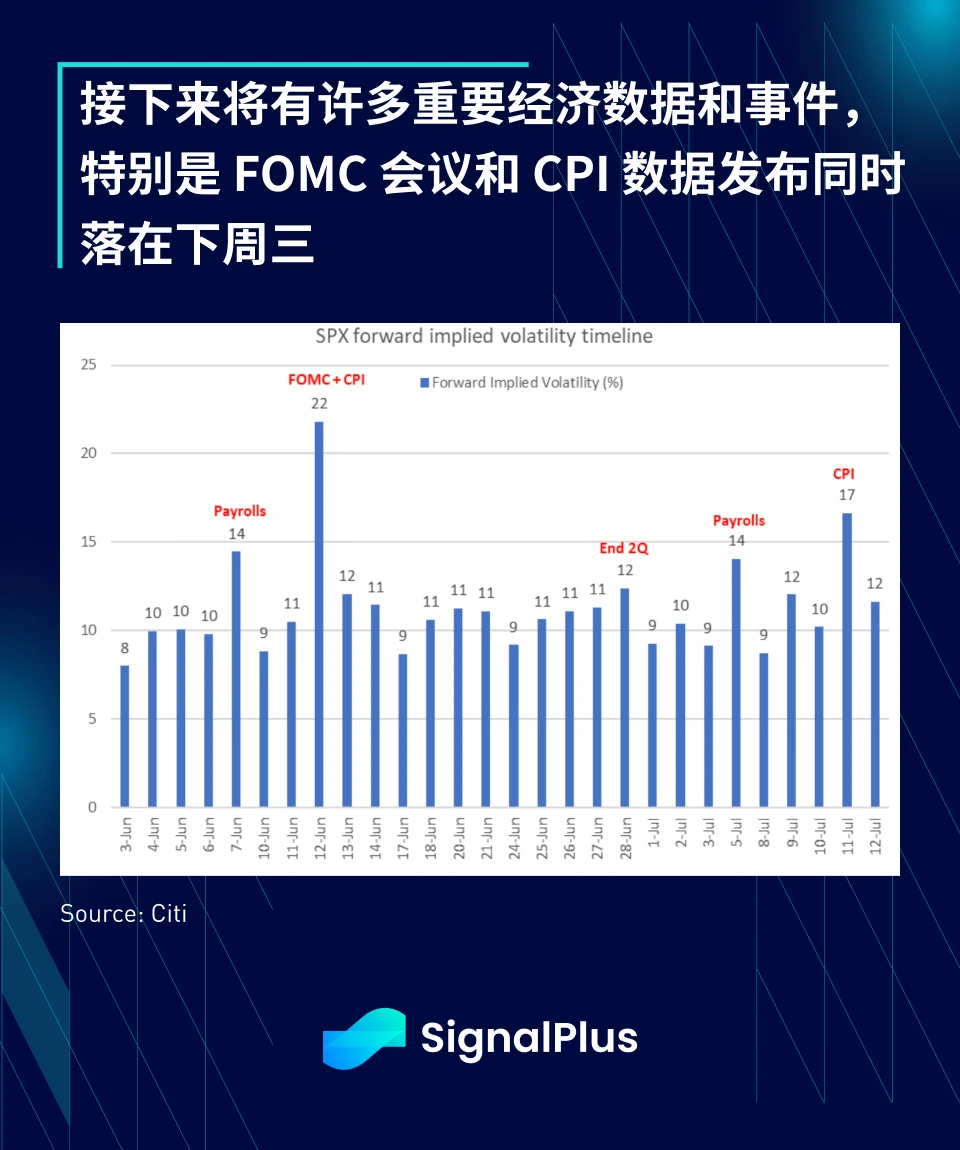

Macro assets have rallied sharply over the past few sessions, fueled by a continued deceleration in PCE last Friday, a 10% drop in oil futures, and hopes for an ideal economic slowdown. This week will see a string of important data releases, including todays JOLTS, Wednesdays ADP and ISM service sector indexes, and Fridays non-farm payrolls.

The non-farm payrolls data may be the most important event of the week, but there will also be a FOMC meeting and CPI data release on the same day next Wednesday. This will be the most anticipated day before the summer, so be sure to fasten your seat belts!

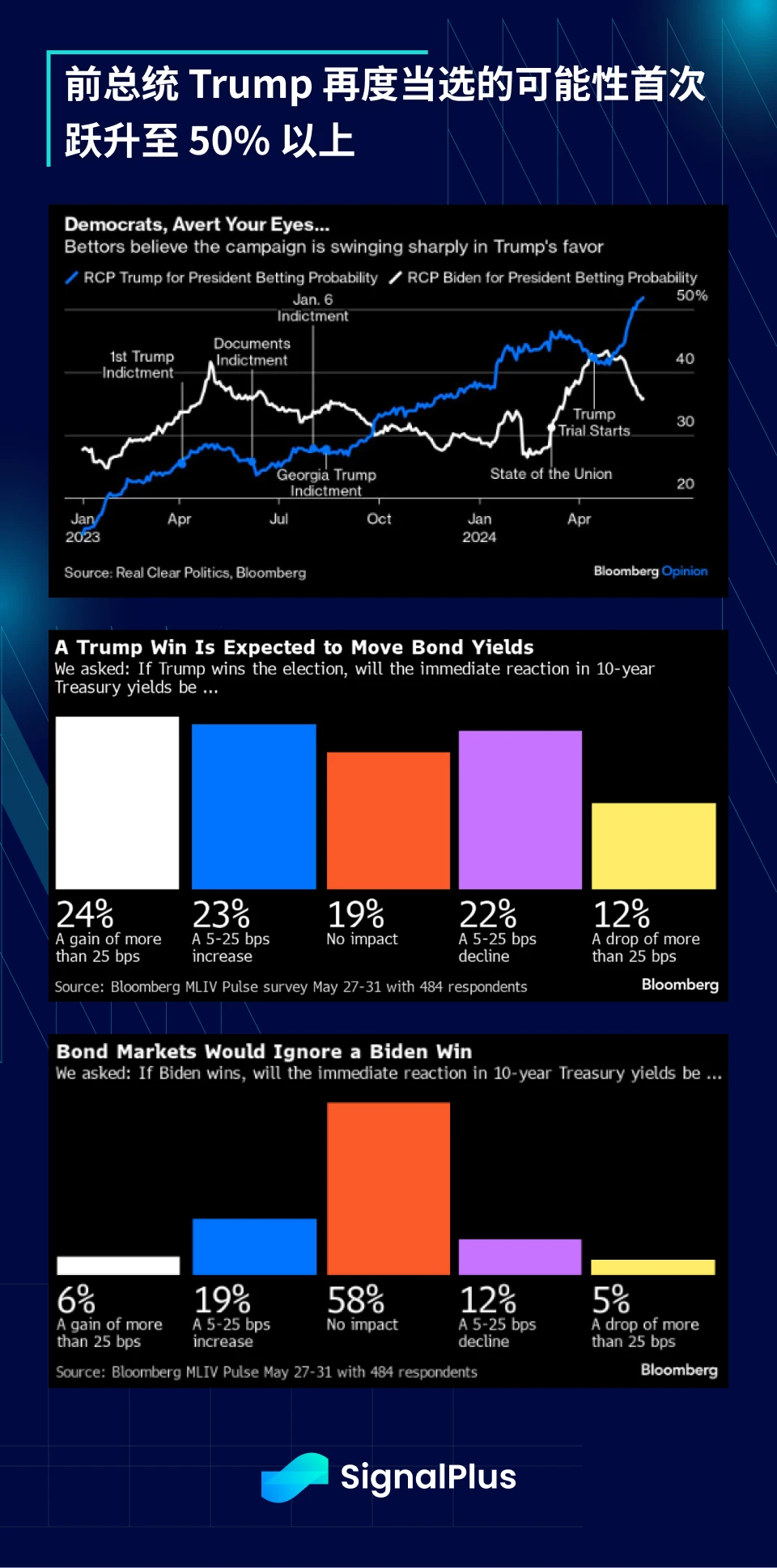

On the election front, former President Trump has benefited greatly from his recent guilty verdict, with his odds of winning the November election jumping to over 50% (compared to Bidens 35%), and it seems that a significant portion of voters see this as a political witch hunt against Trump, which is actually in Trumps favor. If the former president is re-elected, the main impact will be on fixed income, as the market generally expects him to exert new political influence on the Federal Reserve, promote loose monetary policy, free-spending fiscal policy, and further tax cuts, which will definitely make the fourth quarter very interesting, at least for the market.

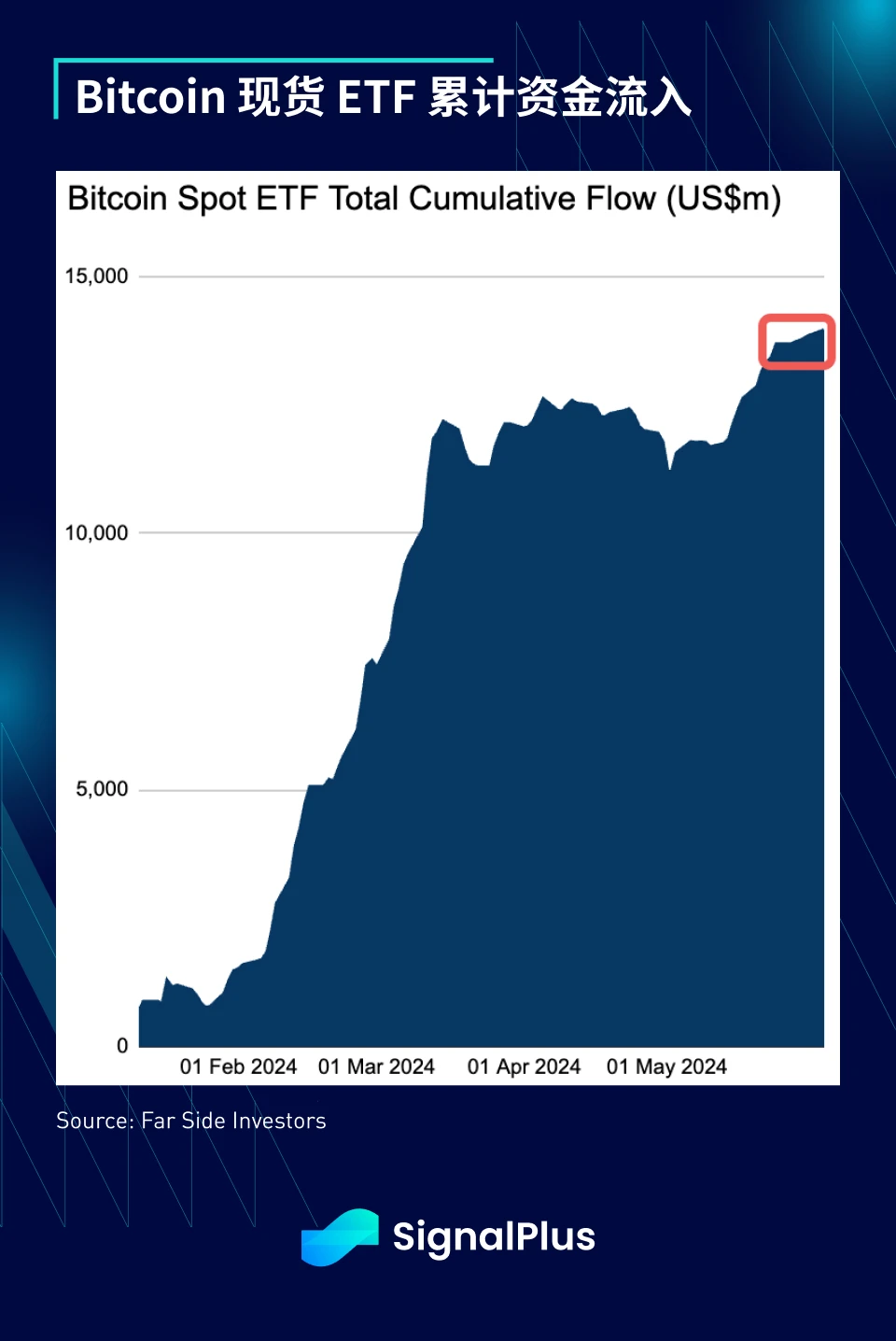

In terms of cryptocurrencies, with the rebound in the US stock market and the overall recovery in risk sentiment, market sentiment has been boosted since last Friday, with BTC challenging $70,000 again and ETH hovering around $3,800. However, trading activity remains sluggish, funding rates are low, and realized volatility is not high, keeping prices within the recent range. We expect this situation to continue at least until Fridays non-farm payrolls data, and the next major fluctuation will have to wait until next Wednesdays CPI and Fed meeting. At present, there seems to be less resistance to the upside, so I wish you all good luck!

You can search for SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time encryption information. If you want to receive our updates immediately, please follow our Twitter account @SignalPlus_Web3, or join our WeChat group (add assistant WeChat: SignalPlus 123), Telegram group and Discord community to communicate and interact with more friends. SignalPlus Official Website: https://www.signalplus.com