Original author: ASXN

Original translation: TechFlow

The Ethereum ETF will be launched on July 23. The market ignores many dynamics associated with the ETH ETF that do not exist in the BTC ETF. We will explore liquidity forecasts, the unwinding of ETHE, and the relative liquidity of ETH:

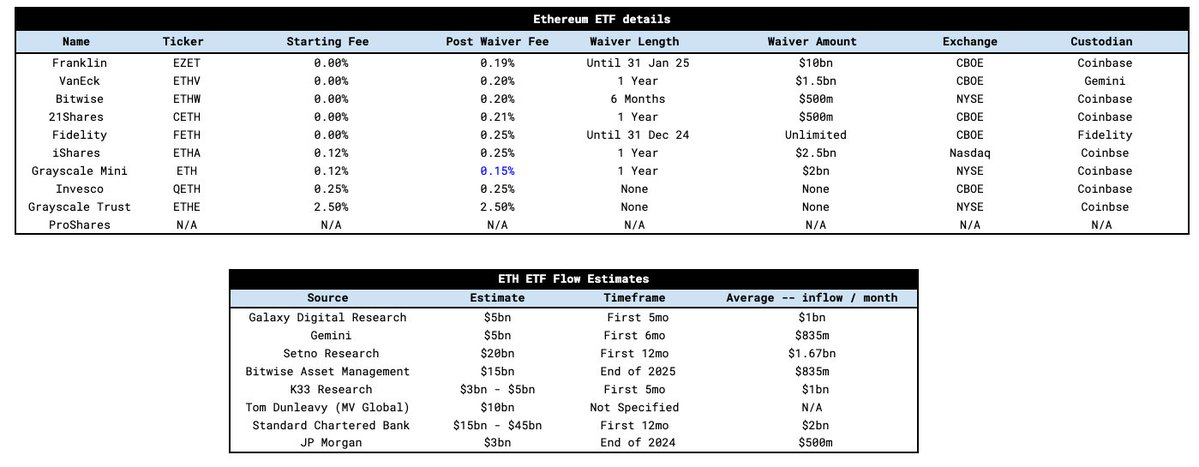

The fee structure of the ETF is similar to that of the BTC ETF. Most providers waive fees for a specified period to help accumulate assets under management (AUM). Similar to the BTC ETF, Grayscale maintains its ETHE fee at 2.5%, an order of magnitude higher than other providers. The key difference this time is the introduction of the Grayscale mini ETH ETF, which did not exist in the previous BTC ETF.

The mini trust is a new ETF product from Grayscale with an initially disclosed fee of 0.25%, similar to other ETF providers. Grayscale’s strategy is to charge those inactive ETHE holders a 2.5% fee while directing more active and fee-sensitive ETHE holders to their new product rather than to low-fee products like Blackrock’s ETHA ETF. After other providers cut Grayscale’s 25bps fee, Grayscale reduced the mini trust fee to just 15bps, making it the most competitive product. In addition, they are transferring 10% of ETHE AUM to the mini trust and gifting this new ETF to ETHE holders. This transition is done on an equal footing, so it is not a taxable event.

The result is that outflows from ETHE will be more gradual than from GBTC, as holders are simply transferring to the mini trust.

Now lets look at liquidity:

There are many estimates of ETF liquidity, and we have listed some below. When these estimates are normalized, the average is around $1 billion per month. The highest estimate provided by Standard Chartered is $2 billion per month, while the lowest estimate provided by JPMorgan is $500 million per month.

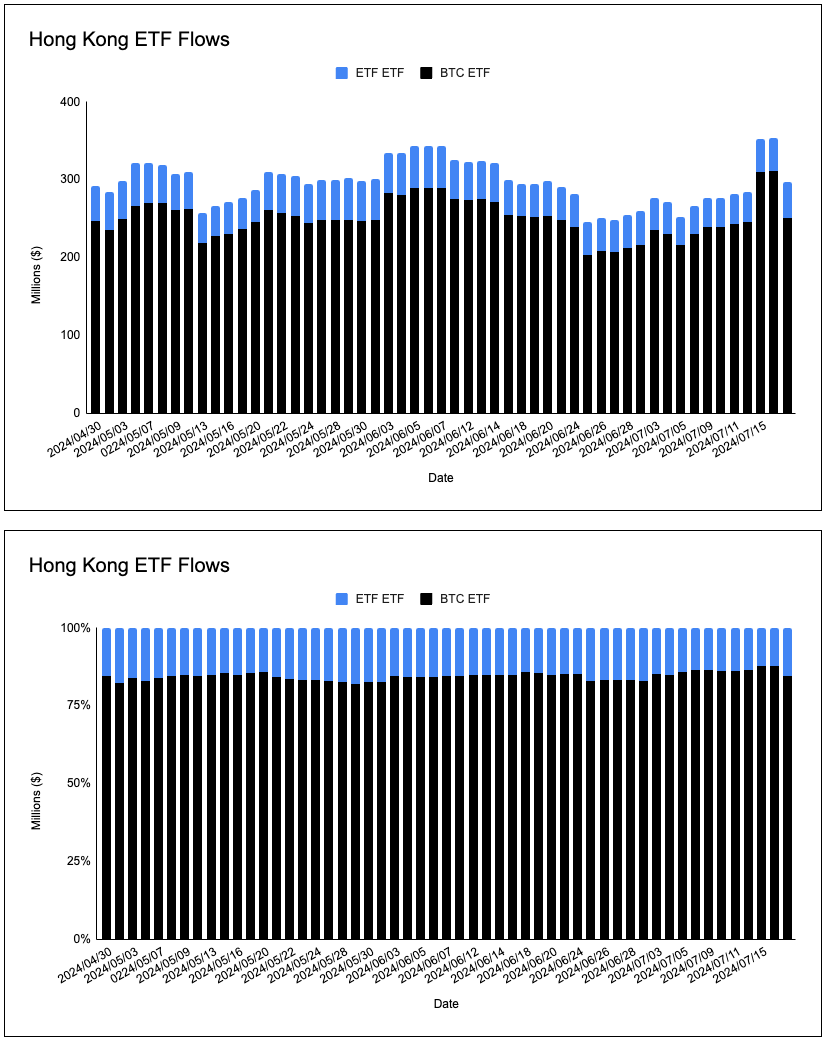

Fortunately, we can use data from Hong Kong and European ETPs and the disappearance of the ETHE discount to help estimate liquidity. If we look at the distribution of AUM of Hong Kong ETPs, we draw two conclusions:

Relative to market capitalization, the AUM ratio of BTC and ETH ETPs is more biased towards BTC. The market capitalization ratio is 75:25, while the AUM ratio is 85:15.

The ratio of BTC to ETH in these ETPs is relatively constant and consistent with the ratio of BTC market capitalization to ETH market capitalization.

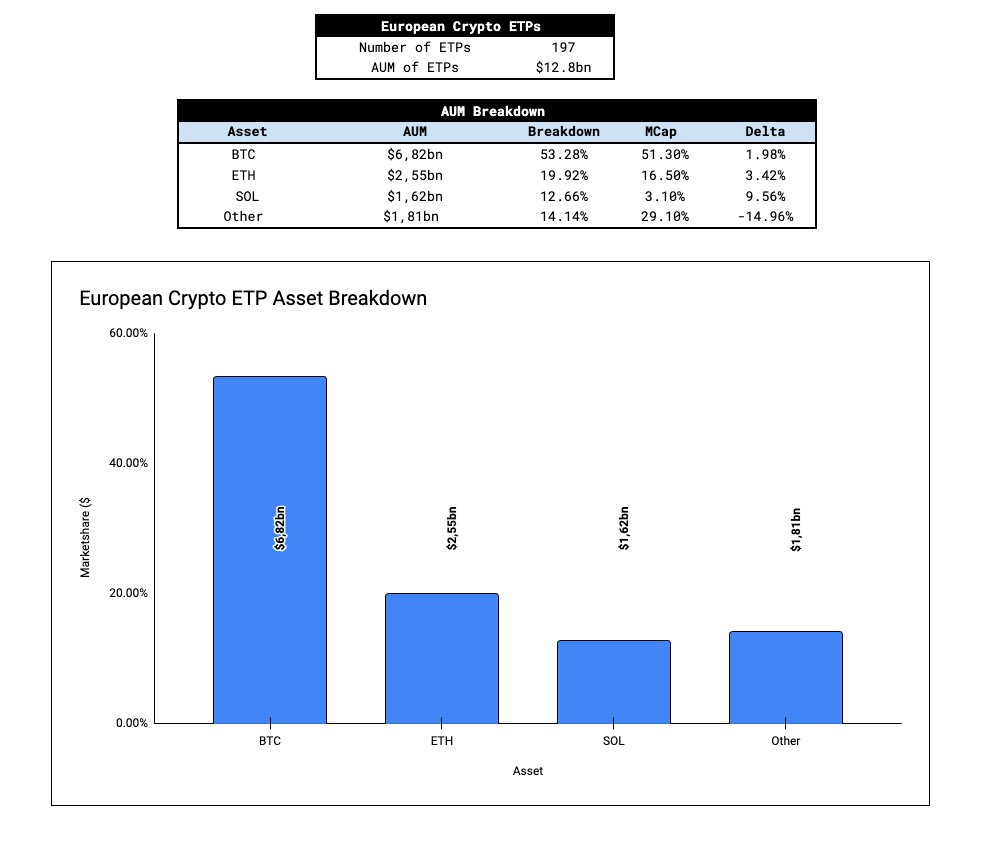

In Europe, we have a much larger sample size - 197 crypto ETPs with a total assets under management (AUM) of $12 billion. After analyzing the data, we found that the distribution of AUM across European ETPs roughly matches the market cap of Bitcoin and Ethereum. Solanas allocation is overweight relative to its market cap, at the expense of other crypto ETPs (anything not BTC, ETH, or SOL). Leaving Solana aside, a trend begins to emerge - the distribution of AUM between BTC and ETH globally roughly reflects the proportions weighted by market cap.

Given that the cause of GBTC outflows was the “sell the news” narrative, it is important to assess the potential for ETHE outflows. In order to model potential ETHE outflows and their impact on price, it is helpful to examine the percentage of ETH supply that is in the ETHE vehicle.

After adjusting for Grayscale mini seed capital (10% of ETHE AUM), ETHE as a carrier, where ETH supply accounts for a similar proportion of total supply as when GBTC was launched. While it is not clear how much of GBTC outflows are turnover and exits, if it is assumed that the proportion of turnover and exits is similar, then the impact of ETHE outflows on price will be similar to GBTC outflows.

Another key piece of information that most people overlook is the premium/discount of ETHE to Net Asset Value (NAV). ETHE has been trading within 2% of NAV since May 24th - while GBTC first traded within 2% of NAV on January 22nd, just 11 days after GBTC converted to an ETF. The approval of a spot BTC ETF and its impact on GBTC is gradually being priced in by the market, and the situation of ETHE trading at a discount to NAV has been more clearly communicated through GBTC. By the time the ETH ETF goes live, ETHE holders will have 2 months to exit ETHE at close to NAV. This is a key factor that will help curb outflows from ETHE, especially direct outflows from the market.

At ASXN, our internal estimate is between $800 million and $1.2 billion in monthly inflows. This is calculated by taking the market cap weighted average of Bitcoin’s monthly inflows and adjusting by Ethereum’s market cap.

Our estimates are supported by global crypto ETP data which suggests that market cap weighted baskets are the dominant strategy (we may see a rotation flow into BTC ETFs adopting a similar strategy). Additionally, with ETHE trading at par prior to launch and the introduction of mini trusts, we are open to potential upside surprises.

Our ETF inflow estimates are proportional to their respective market caps, so the impact on price should be similar. However, one also needs to assess how much of the asset is liquid and ready to be sold - assuming that the smaller the float, the more sensitive the price will be to inflows. There are two idiosyncratic factors that influence ETHs liquid supply, namely the native stake and the supply held in smart contracts. Therefore, there is less liquid and sellable ETH than BTC, making it more sensitive to ETF flows. However, it is important to note that the liquidity gap between the two assets is not as large as some have suggested (ETHs cumulative +-2% order book depth is 80% of BTCs).

Our estimates of liquid supply are as follows:

As we get closer to the launch of ETFs, it is important to understand the reflexivity of Ethereum. Its mechanism is similar to BTC, but Ethereums burning mechanism and the DeFi ecosystem built on it make the feedback loop more powerful. The reflexive loop is roughly as follows:

ETH flows into ETH ETF → ETH price increases → Interest in ETH increases → DeFi/chain usage increases → DeFi fundamentals improve → EIP-1559 burn increases → ETH supply decreases → ETH price increases → More ETH flows into ETH ETF → Interest in ETH increases → …

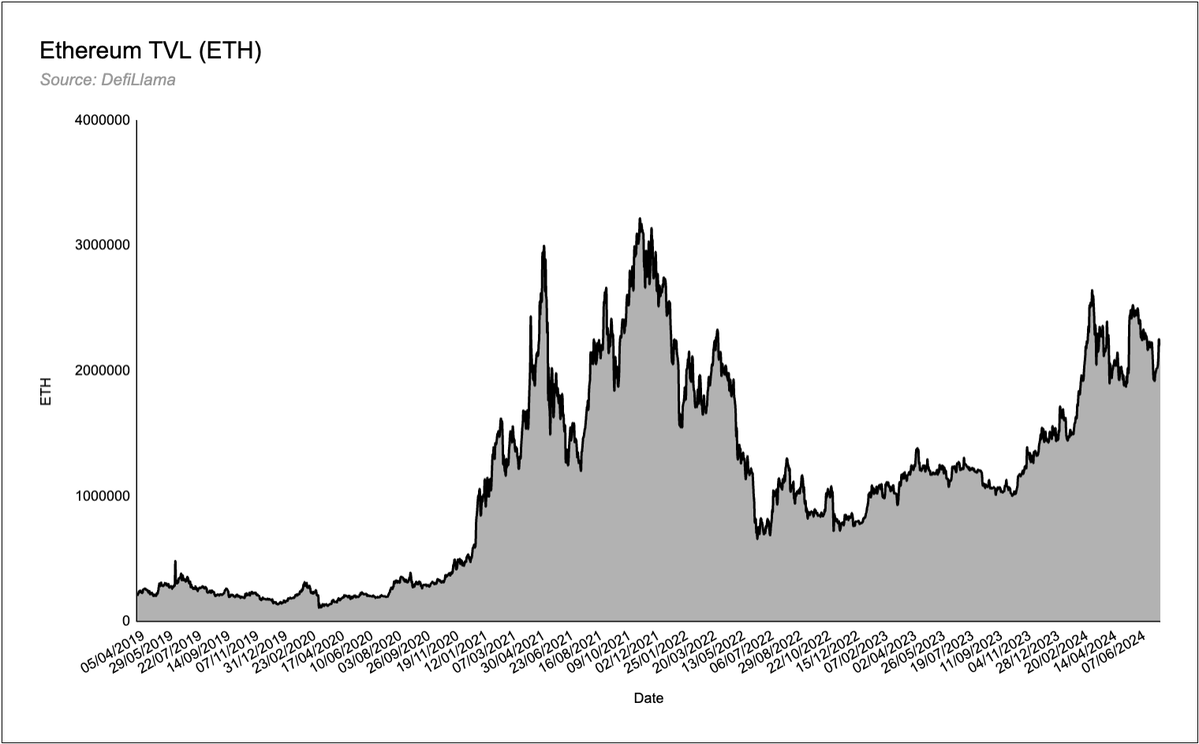

An important factor missing from the BTC ETF is the ecosystem wealth effect. In the emerging Bitcoin ecosystem, we do not see a lot of gains being reinvested into base layer projects or protocols, although there is some small interest in ordinarys and inscriptions. Ethereum, as a decentralized application store, has an entire ecosystem that will benefit from continued inflows into the base asset. We believe that this wealth effect has not received enough attention, especially in the DeFi space. There is 20M ETH ($63B) of total value locked (TVL) in Ethereum DeFi protocols, and as the price of ETH rises, ETH DeFi becomes more attractive as TVL and revenue in USD surge. ETH has a reflexivity that does not exist in the Bitcoin ecosystem.

Other factors to consider:

What will the rotation flow from BTC ETF to ETH ETF look like? Assume that there is a portion of BTC ETF investors who are unwilling to increase their net cryptocurrency exposure but want to diversify their investments. In particular, traditional financial (TradFi) investors prefer market capitalization-weighted strategies.

How well does traditional finance understand ETH as an asset and Ethereum as a smart contract platform? Bitcoin’s “digital gold” narrative is both simple and well-known. How well is Ethereum’s narrative (e.g., settlement layer of the digital economy, three-point asset theory, tokenization, etc.) understood?

How will previous market conditions affect ETHs liquidity and price trend?

Traditional finance decision-makers have chosen two crypto assets to bridge their worlds - Bitcoin and Ethereum. These assets have gone mainstream. How does the introduction of spot ETFs change the way traditional finance capital allocators think about ETH, given that they are now able to offer a product that can charge fees. Traditional finances desire for yield makes Ethereums native yield through staking a very attractive proposition, and we believe that staking ETH ETFs is a matter of time, not a matter of if. Providers can offer zero-fee products and simply stake ETH in the background to earn a yield that is an order of magnitude higher than a regular ETH ETF.