OKX Ventures: A detailed explanation of the six core asset markets in the RWA track

Original author: Esme Zheng, OKX Ventures

In the current market environment, "Real-World Assets" (RWA) are rising rapidly. In July this year, Coingecko pointed out in its second quarter 2024 crypto industry report that Meme Coin, artificial intelligence and RWA became the most popular categories, accounting for 77.5% of network traffic.

Traditional financial giants such as Citi, BlackRock, Fidelity and JPMorgan Chase have also joined the game. According to Dune Analytics data, RWA narratives have ranked second in growth since the beginning of this year, up 117%, second only to Meme. This article will comprehensively sort out the development status and future opportunities of the RWA track.

TL;DR

1. RWA is one of the fastest growing DeFi fields, with TVL doubling in 2023 and the value of on-chain assets growing by 50% since the beginning of 2024, reaching $12 billion (excluding stablecoins). The fastest growing and largest sectors are the private credit market (76%) and U.S. debt products (17%), while the rest are precious metal stablecoins led by gold, real estate tokens, etc.

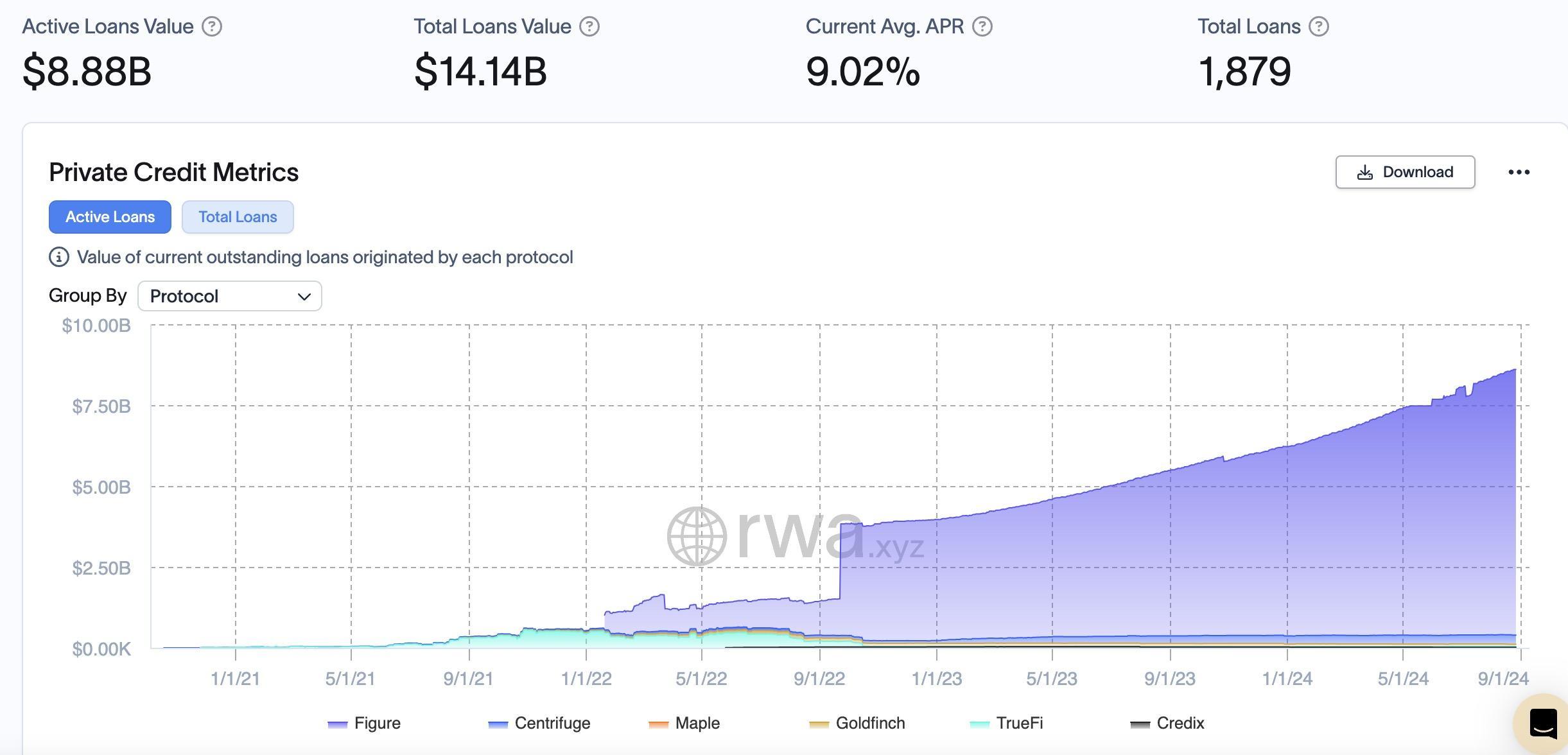

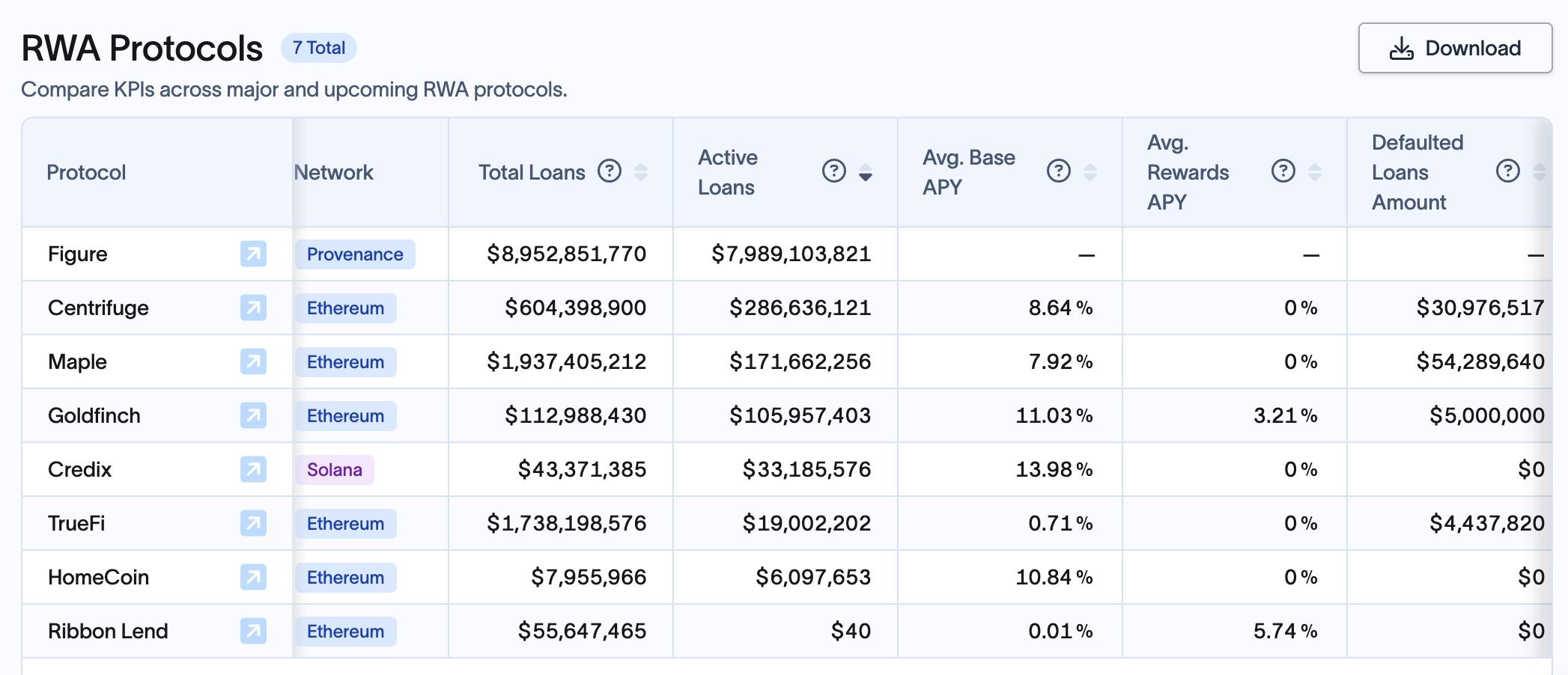

2. Currently, nearly 15 mainstream issuers offer more than 32 tokenized U.S. debt-related products, with total assets exceeding $2 billion, a 1,627% increase from the beginning of the year. The six mainstream on-chain credit protocols, Figure, Centrifuge, Maple, Goldfinch, TrueFi, Credix, etc., have a total active loan amount of $8.88 billion, a 43% increase from the beginning of the year.

3. Following the successful adoption of stablecoins on-chain and the attractive net interest margins earned by off-chain centralized issuers, the next stage of RWA evolution will be driven by tokenized U.S. Treasury issuance, where token holders capture the lion’s share of the net interest margin by investing directly in real-world assets that are short-term, liquid, and backed by the U.S. government.

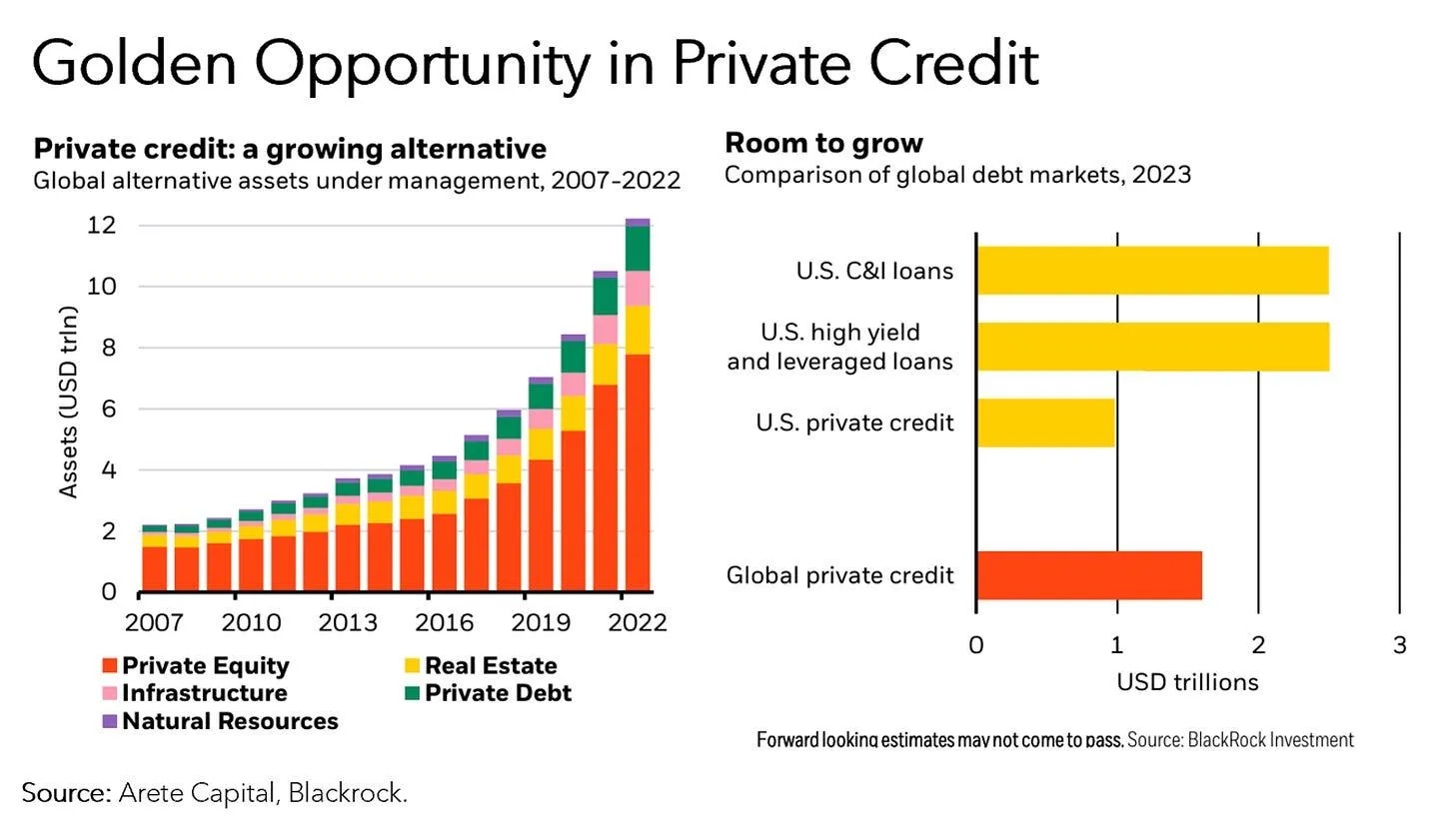

4. The on-chain private credit lending market faced major challenges after the collapse of centralized financial bad debts, and is now experiencing a recovery driven by the RWA narrative. Although the total amount of on-chain credit currently accounts for less than 0.5% of the traditional $1.5 trillion private credit market, the sharp upward trend indicates that the on-chain credit field has great potential for further expansion.

5. The application scenarios of real-world asset tokenization in the traditional financial field involve a large number of asset issuance, transactions and other operations. For financial institutions that control core assets, compliance and security are the main demands. RWA needs to exist in "trusted finance" or "verifiable finance" and needs to be a "regulated cryptocurrency". Especially in the context of stablecoins, they still require a large number of off-chain intermediaries to conduct audits, compliance and asset management, all of which require a trust foundation.

1. Current status of the RWA track

1. Market supply and demand

1. The core logic of RWA is to map the income rights of financial assets in the real world (such as interest-bearing assets such as U.S. Treasury bonds, fixed-income securities, and equity assets such as stocks) to the blockchain, and obtain the liquidity of on-chain assets by mortgaging off-chain assets. For physical assets such as gold and real estate, it is to introduce them to the chain and use blockchain technology to improve the convenience and transparency of transactions.

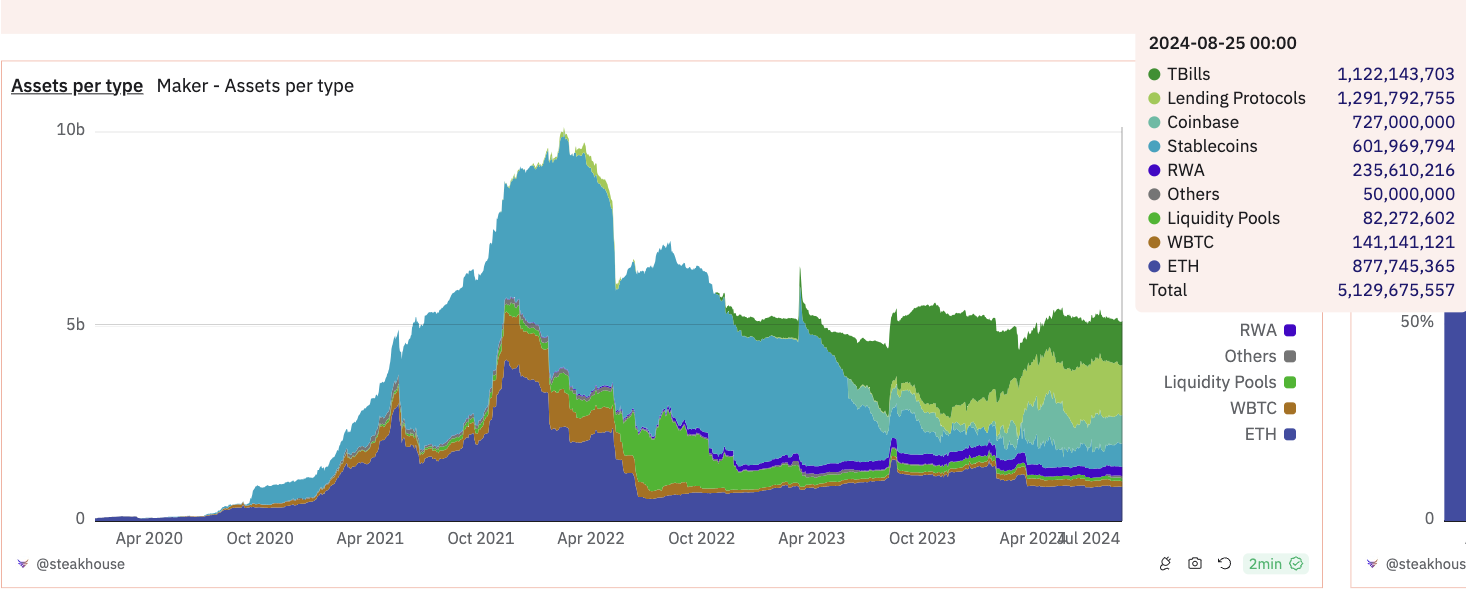

2. In the context of the Fed's continuous interest rate hikes and balance sheet reduction, high interest rates have greatly affected the valuation of risk markets, and balance sheet reduction has greatly extracted liquidity from the crypto market, causing the yield of the DeFi market to continue to decline. At that time, the risk-free yield of US Treasury bonds as high as 5% became a hot commodity in the crypto market. The most popular one is the behavior of MakerDAO to purchase US Treasury bonds as reserve assets. In addition to increasing asset diversity, stabilizing exchange rates, and reducing single-point risks, the most important thing is to meet the unilateral demand of the Crypto world for the yield of real-world financial assets.

Source: Dune / @steakhouse

3. There are a large number of stablecoins circulating in the market. In a high-interest environment, holders do not get any benefits at all, and are actually paying opportunity costs. Centralized stablecoins privatize profits and socialize losses. More types of RWA assets are needed to effectively utilize these stablecoins, generate benefits for users, and bring more liquidity to the DeFi market.

4. For large, established asset managers such as Franklin Templeton and WisdomTree, tokenization represents the opening of new distribution channels to reach new customer segments that prefer to hold their assets digitally on a blockchain rather than in a traditional brokerage or bank account. For them, tokenized Treasuries are their “beachhead market.”

5. The traditional financial sector is increasingly focusing on combining with DeFi technology, reducing costs and increasing efficiency through asset tokenization, and solving inherent problems in traditional finance. Mapping real-world assets (such as stocks, financial derivatives, currencies, equity, etc.) to the blockchain not only expands the application scope of distributed ledger technology, but also makes the exchange and settlement of assets more efficient. In addition to exploring new distribution channels, it also focuses on the significant efficiency improvements and innovations that technology brings to the traditional financial system.

2. Market size:

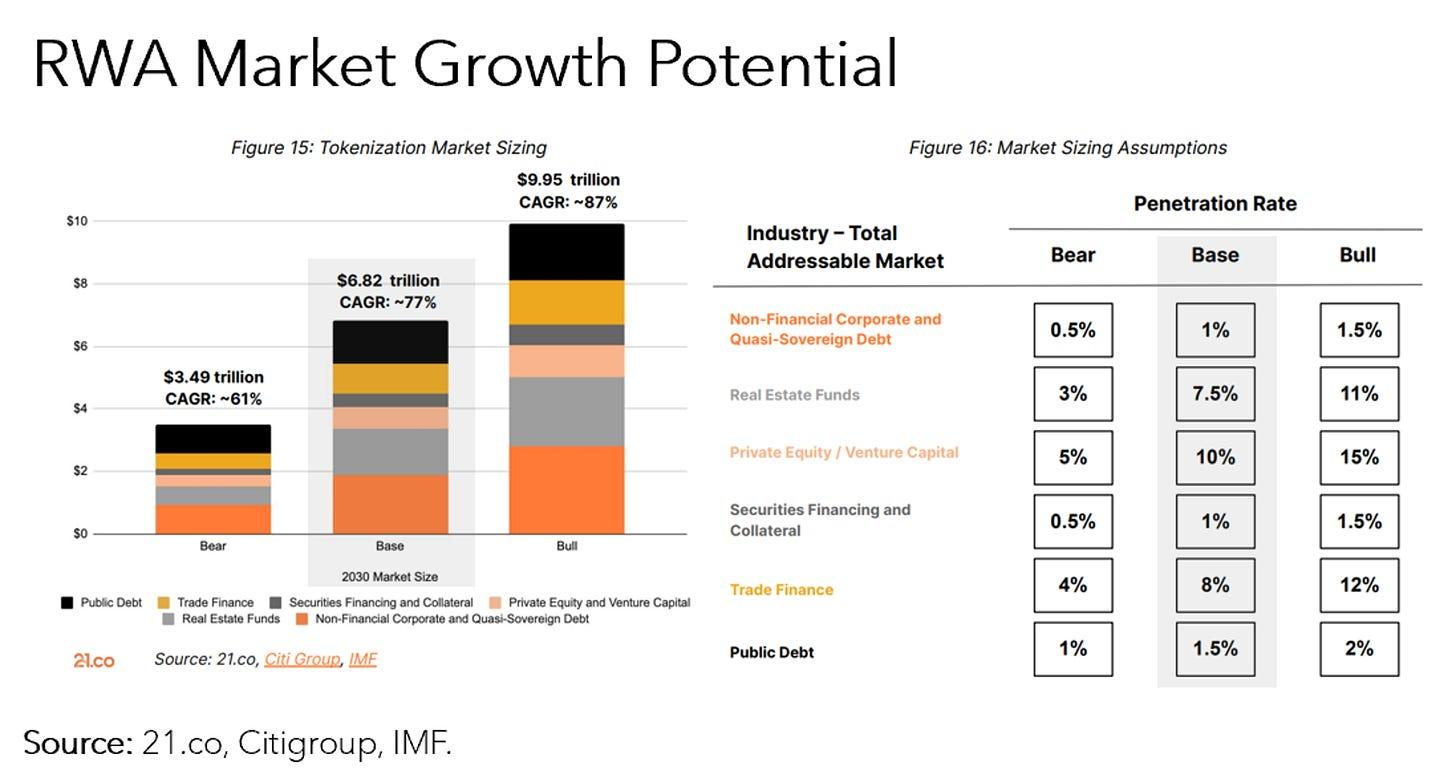

The asset size of RWA chain is about 12 billion, and the total market value of stablecoins exceeds 180 billion US dollars. Through blockchain technology, the digitization of traditional financial assets can not only improve transparency and efficiency, but also attract more users to enter this emerging market. According to reports from 21.co, Citi and IMF, the total value of tokenized assets is expected to grow to 6.8 trillion US dollars in 2030 under basic market conditions.

Source: 21.co, Citigroup, IMF

Private credit and US Treasuries are the leading assets being tokenized - the markets have grown from millions of dollars to $8.8 billion in total loan value (63% y/y growth) and over $2 billion in Treasuries (2100% y/y growth) respectively. Tokenized Treasuries are still an emerging space with huge potential - Franklin Templeton, BlackRock and Wisdomtree are early leaders in this space.

Source: rwa.xyz

The Fed’s policies have a direct and significant impact on the expansion and pattern of the RWA DeFi field:

In the third quarter of 2022, private credit-backed RWAs accounted for 56% of the total RWA TVL, while the share of U.S. Treasury-backed RWAs was 0%.

In the third quarter of 2023, the share of RWAs backed by private credit fell to 18% of total RWA TVL, while the share of RWAs backed by U.S. Treasuries rose to 27%.

As of the end of August 2024, when this article was published, RWAs backed by private credit accounted for 76% of total TVL, and the share of RWAs backed by U.S. Treasuries stabilized at 17%.

Source: rwa.xyz

1) Market promoters:

The growth of interest-bearing (interest-bearing, fixed-income) RWA is rapid. Since 2024, the on-chain value of non-stablecoin RWA has increased by $4.11 billion, mostly from government bonds, private credit, and real estate tokens. The current overall growth and ecological improvement are mainly attributed to the following three aspects:

1. Institutional interest and new products, e.g.

Institutions such as BlackRock and Superstate have launched new on-chain Treasury products and T-bills funds.

Ondo launches USDY, Centrifuge collaborates with Maker and BlockTower, etc.

2. Complete infrastructure, e.g.

M^0 Labs develops institutional-grade stablecoin middleware that can be used as a building block for other products.

Ondo Global Markets creates a two-way system that enables seamless transfers between on-chain tokens and off-chain accounts.

3. Integration with DeFi, for example

Morpho allows the creation of non-custodial vaults to pass RWA returns to DeFi users; combined with Centrifuge, it supports collateralized lending.

TrueFi launched Trinity, which allows users to deposit tokenized U.S. Treasuries as collateral to mint dollar-pegged assets that can be used in DeFi.

DAO’s Diversification of Assets (Maker)

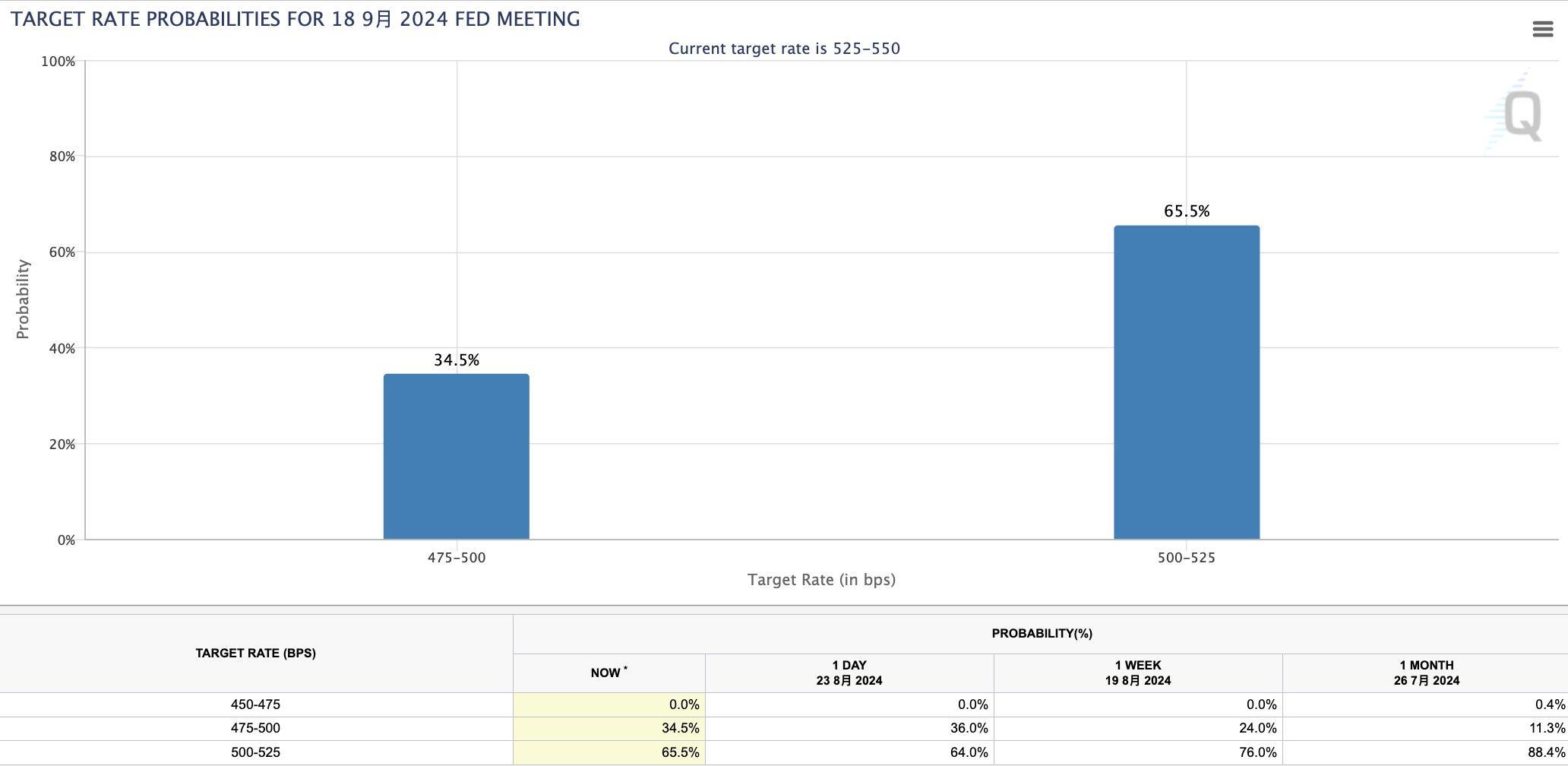

Given the latest statement by Fed Chairman Powell, the Fed has sent a dovish signal for the first time since the start of the rate hike cycle, indicating that its focus is shifting from controlling inflation to supporting economic growth and employment. The trend of a rate cut cycle has gradually formed, which is expected to stimulate the return of leveraged funds. Currently, the CME Fed Watch tool shows that a 25 basis point rate cut in September is most likely. However, the August CPI and non-farm data will be released soon. If the data exceeds expectations, the probability of a 50 basis point rate cut in September will increase.

As high interest rate policies continue, T-bill will still be the first choice for idle funds, and the trend of continuous interest rate cuts will have a profound impact on the market. On the one hand, the low interest rate environment may stimulate investors to seek higher yield opportunities and drive funds into the high-yield DeFi field. On the other hand, the decline in the yield of traditional assets may prompt more RWAs to be tokenized in order to seek higher returns on the DeFi platform. By then, the market competition landscape may change, and more capital will flow into high-yield RWA application scenarios combined with DeFi technology, further promoting the development of the entire on-chain economy.

Source: CME FedWatch

2) Main user portraits:

According to Galaxy Digital's 2023 full-year statistics, most RWA on-chain demand is driven by a small number of native cryptocurrency users, rather than new cryptocurrency adopters or traditional financial users turning to the chain. Most of these addresses interacting with RWA tokens were active on the chain before these assets were created. The following data is analyzed only for addresses holding tokenized treasuries and mainstream private credit assets:

Unique addresses: As of August 31, 2023, there are 3,232 UAs holding RWA assets. As of August 26, 2024, there are 61,879 holding addresses, an increase of 1,815%.

Average age of addresses: 882 days (about 2.42 years), indicating that these users have been active since around April 2021.

Average RWA age: 375 days, indicating that these assets are relatively new compared to the addresses.

The oldest address interacting with RWA dates back to March 22, 2016, which is 2,718 days old.

The distribution shows that the wallet addresses are concentrated around 700-750 days old.

Number of addresses by age group:

<1 year: 17% (545 addresses)

1 to 2 years: 27% (885 addresses)

2 to 3 years: 36% (1,148 addresses)

3+ years: 20% (654 addresses)

According to the Transak report, the total number of RWA token holders on the Ethereum chain alone exceeded 97,000 in mid-2024, with a total of more than 205,000 unique addresses. These tokens added about 38,000 holders last year.

RWA tokens have also seen a significant increase in overall DEX volume since the beginning of 2024. DEX volume was around $2.3 billion in December 2023, surging to over $3.6 billion by April 2024.

And so far in 2024, as traditional financial institutions have significantly increased their adoption of RWA, we can foresee that more and more traditional financial users will gradually enter the crypto field, bringing new growth momentum and incremental funds.

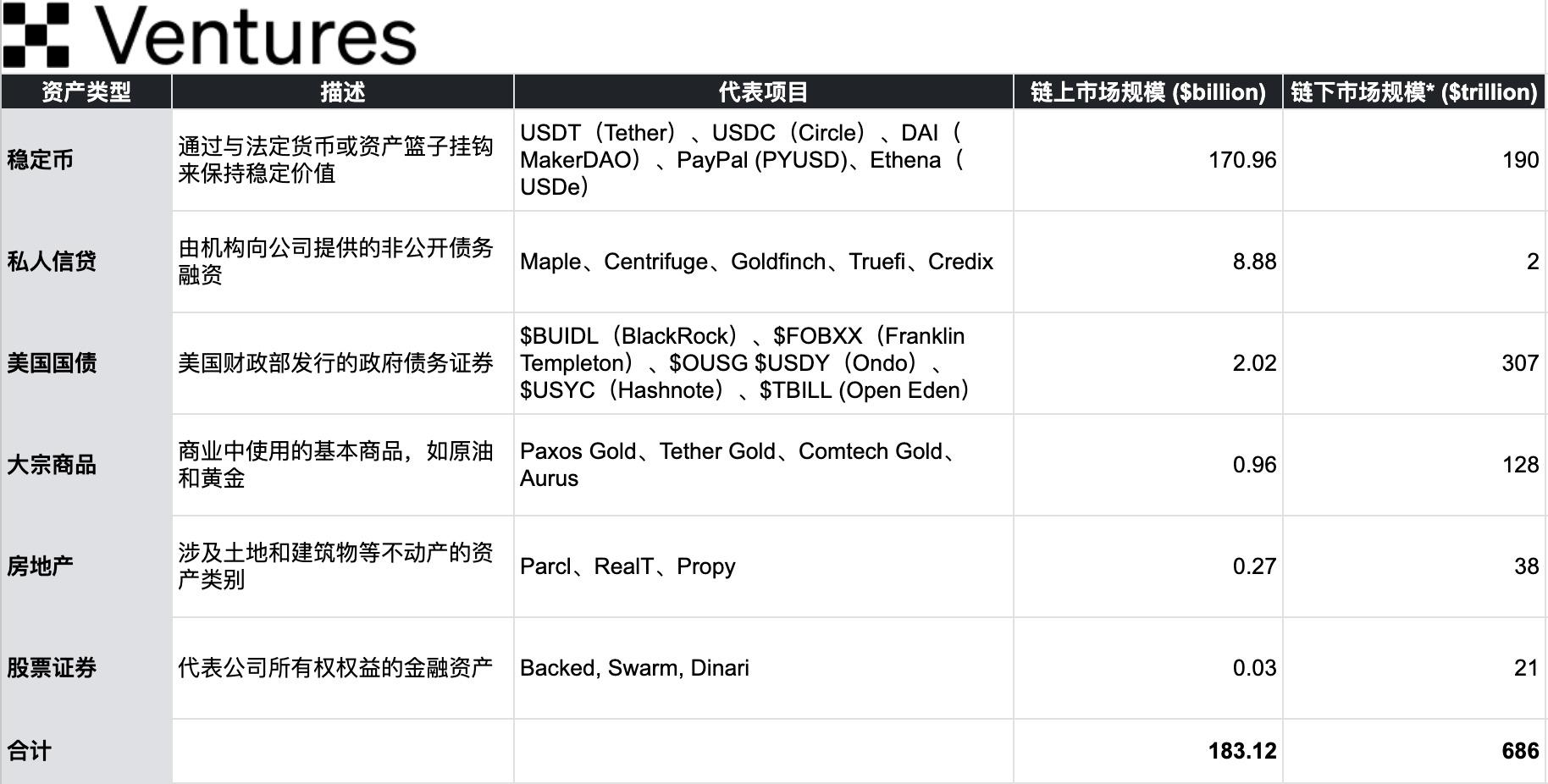

2. Detailed explanation of the six core assets

The tokenized RWA market is divided into 6 categories according to asset class, which are ranked in order of market capitalization: stablecoins, private credit, government bonds (US bonds), commodities, real estate, and equity securities:

Source: OKX Ventures, rwa.xyz, Statista, 21.co

The total market value of real-world assets (RWA) on the chain is $18.312 billion, while the total market value of traditional assets off the chain is $685.5 trillion. Assuming that the total market value of traditional assets off the chain increases by 1 basis point (1 bps, 0.01%) every day, this will bring about an increase of about $6.85 billion, which is close to 37% of the market value of on-chain assets. From this perspective, even a small increase in off-chain assets can have a huge boost to on-chain assets.

1. Stablecoins

Stablecoins have demonstrated clear product-market fit (PMF) in the market and created significant monetization opportunities. For example, in the first quarter of this year, Tether’s earnings exceeded Blackrock’s ($1.48 billion vs. $1.16 billion), despite having a fraction of Blackrock’s assets under management ($70 billion vs. $8.5 trillion).

Market Conditions:

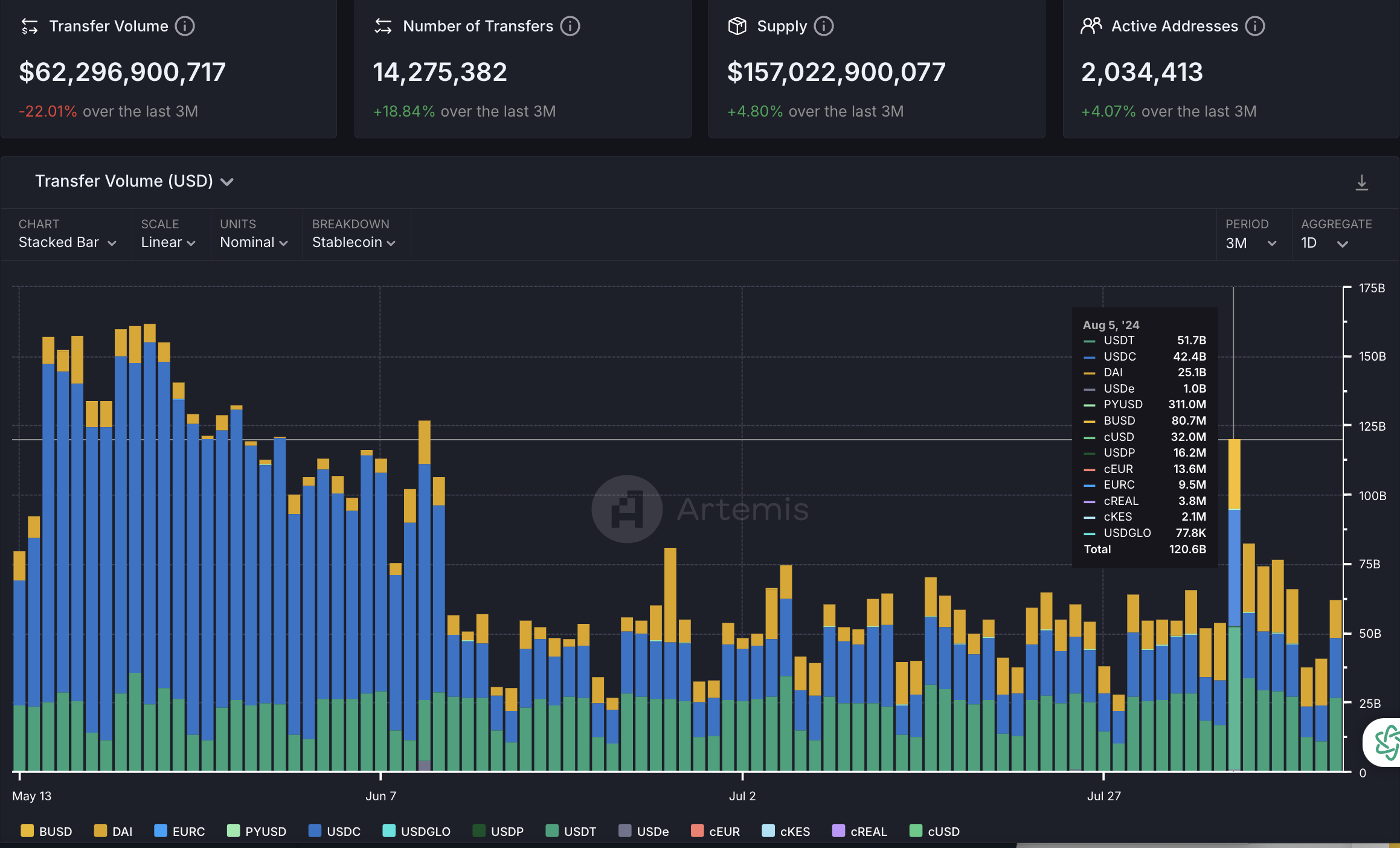

The current market value of stablecoins is approximately US$170 billion , with a monthly transaction volume of up to 1.69 trillion, more than 17 million monthly active addresses, and a total number of holders exceeding 117 million.

Centralized stablecoins still occupy an absolute dominant position: USDT accounts for nearly 70% of the market share, about 114.57 billion US dollars; USDC accounts for 20%, with a market value of about 33.44 billion US dollars;

The market share of decentralized stablecoins remains stable: DAI accounts for 3%, with a market value of approximately US$5.19 billion; Ethena accounts for 2%, with a market value of approximately US$3.31 billion;

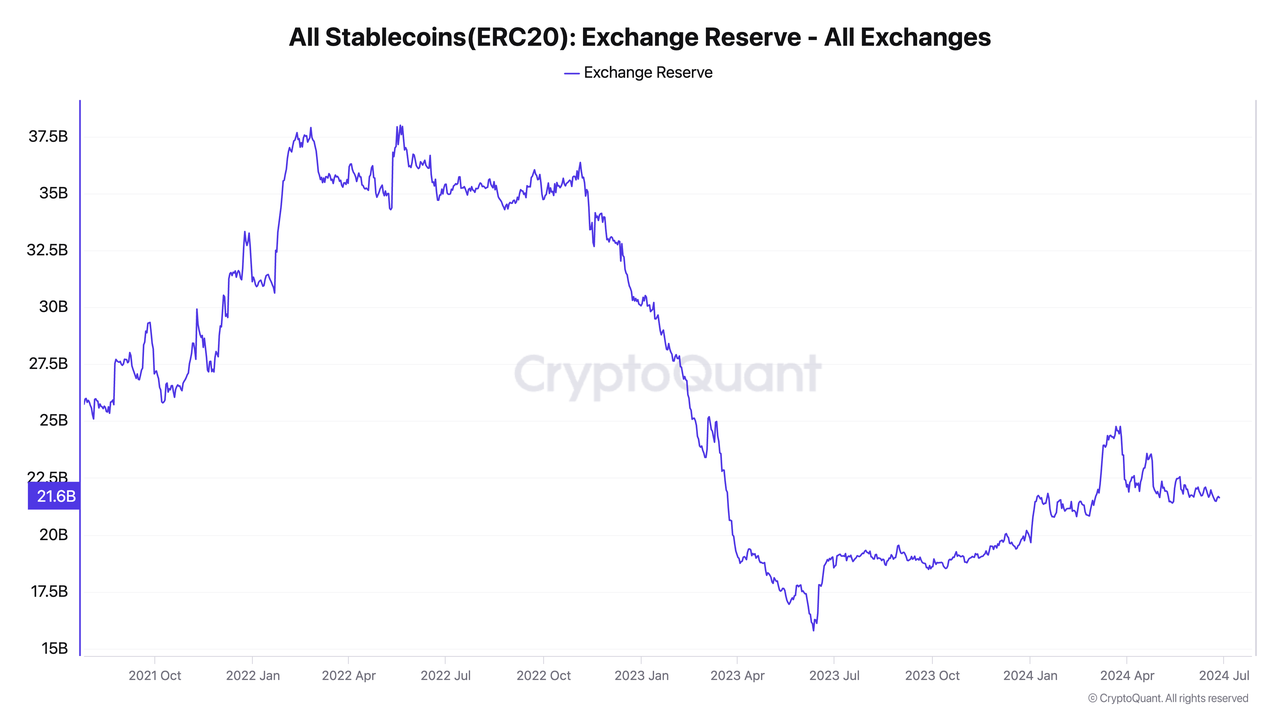

There are approximately 21.63 billion stablecoins stored in centralized exchanges, accounting for 13.2% of the total supply; the remaining circulation, approximately 48.38%, is on Ethereum, 35.95% is on Ethereum, and about 1%-3% is on BSC, Arbitrum, Solana, Base, Avalanche, and Polygon chains respectively.

Source: CryptoQuant, Artemis

Main market issues:

Imbalanced value distribution: Centralized stablecoins often privatize profits but socialize potential losses, resulting in uneven distribution of benefits.

Lack of transparency: Centralized stablecoins like Tether and Circle have serious transparency issues, and users are forced to take unnecessary risks. For example, during the SVB bankruptcy, the market had no way of knowing whether Circle or Tether had any financial exposure to SVB, nor was it clear in which banks their reserves were held. Similarly, Tether has been using part of its reserves for lending and investment activities. According to the audit report issued by TBO, approximately 6.5% of the reserves have been loaned out, approximately 4% have been invested in precious metals, and approximately 2.5% have been classified as other investments. Tether's operating model makes it vulnerable to bank runs, and liquidity crunch could become a potential black swan event.

Decentralized stablecoins have limited scalability: Decentralized stablecoins face scalability challenges because they typically require over-collateralization of large amounts of assets. As the demand for stablecoins grows, relying solely on a single crypto asset as collateral may not be able to meet demand. In addition, poorly designed algorithmic stablecoins have failed many times, exposing the risks of insufficient collateral and unstable mechanisms.

Popular players

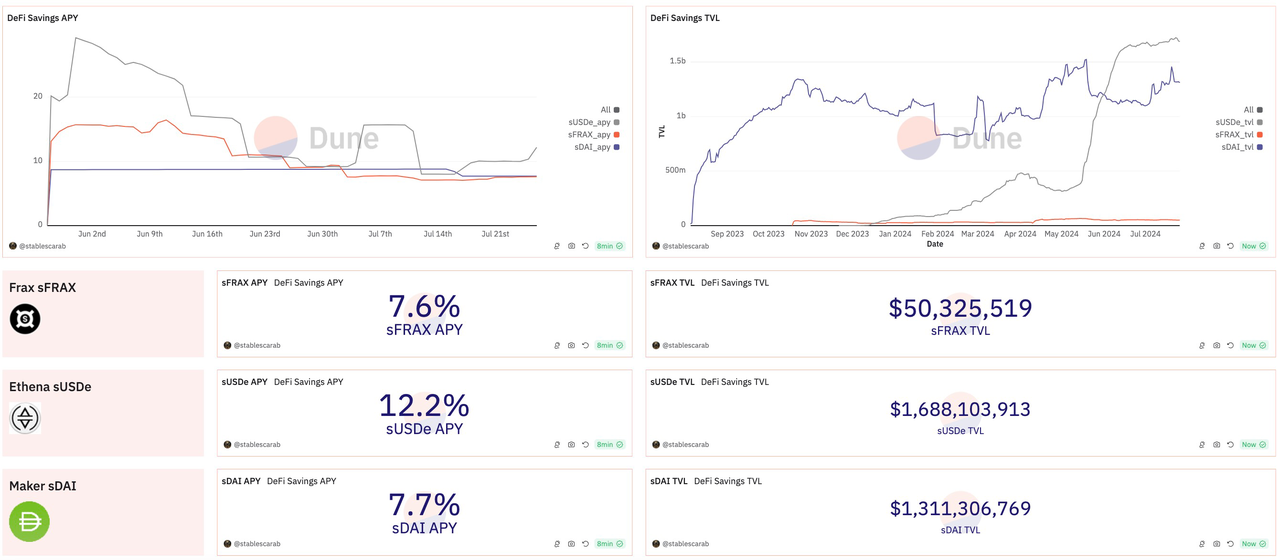

Ethena: Offers a relatively high APY of up to 12.2%, with a current sUSDe TVL of approximately 1.7 billion; the market value has increased by 978% since its launch at the beginning of the year. The Delta Hedge strategy adopted by Ethena is particularly attractive in a bull market environment. When long positions dominate, funding rates are generally favorable for short holders. This strategy allows Ethena to remain stable while attracting traders who want to hedge against market fluctuations and profit from positive funding rates during bull markets.

Maker (now Sky): APY 7.7%, current sDAI TVL is about 1.3 billion; more than 2 billion DAI are deposited in DSR, which is 38% of all DAI in circulation. Since the founder Rune announced the offer of up to 8% yield in August last year, deposits have increased by 197%, and the market value has stabilized at just over 5 billion US dollars. The collateral TVL is 7.74 billion US dollars and the collateral ratio is 147%. Maker integrates US Treasuries into its portfolio, diversifying its income sources and enhancing income stability. Integrate pledged stETH and use it as collateral to mint DAI. It also lifts the 15% slashing penalty for pledges, promoting stability and aligning the interests of holders with the sustainability of the ecosystem.

Source: Dune / @stablescarab

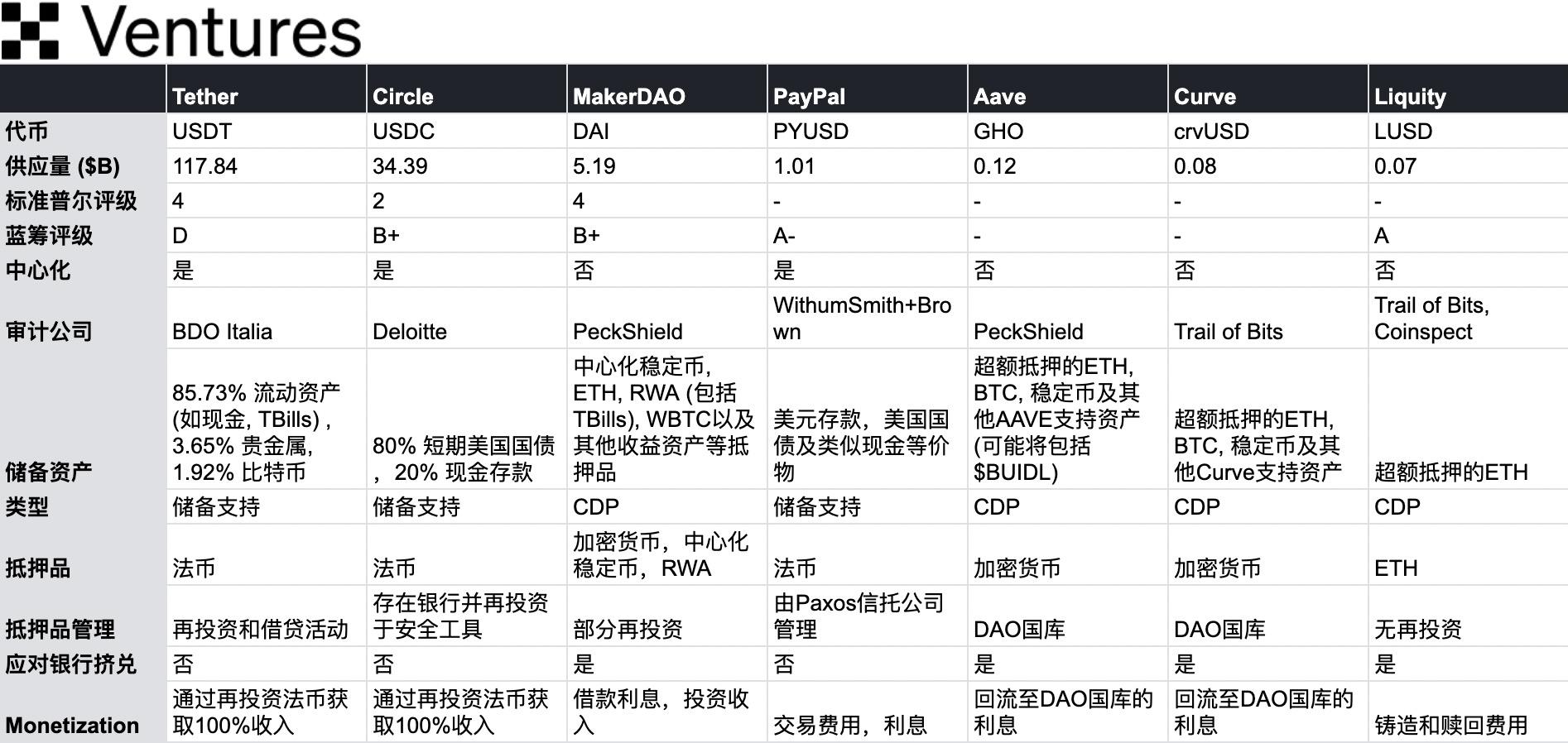

List of mainstream stablecoins

Source: OKX Ventures

Future Outlook:

DAI has thrived largely due to the huge subsidies paid by Curve holders to the 3 pools, which provided a strong moat. As Maker transforms into a more centralized Sky ecosystem, this strategy, while pragmatic, has sparked widespread controversy in the community. Many people worry that the shift to USDS will cause Maker to lose its original decentralized advantage and eventually be swallowed up by more reliable alternatives. Whether it can realize its vision of combining US debt and subDAO models to rapidly scale the Sky ecosystem in the future remains to be seen.

In contrast, Liquity has chosen a completely opposite path. Its v2 $BOLD, a fully Ethereum-native stablecoin backed only by ETH (and LST), will attract a large amount of collateral as currently regulated. Will the insistence on maximum decentralization and elasticity of CDPs make it a niche market product? We look forward to users voting with their real money.

The increasing popularity of low-volatility assets in the stablecoin field. After the education of the market in the last cycle, everyone is more conservative and rigorous in the underlying risk control of crypto-financial assets, especially in the selection of collateral and risk control measures behind currency issuance. Most of the high-risk algorithmic stablecoin projects represented by LUNA, which used high volatility and endogenous assets as collateral in the last cycle, have disappeared.

Due to the clear and simple business lines, regulatory costs are more controllable and consistent. Large financial companies are beginning to target relatively profitable and easy-to-enter stablecoin businesses. Paypal’s PYUSD has reached a circulation of 1 billion, and its market value has increased by 155% since it announced its entry into Solana on May 29. The supply of PYUSD on the Solana chain has also increased by nearly 4685%. Similarly, JD.com’s plan to launch a stablecoin pegged to the Hong Kong dollar is also an attempt to get a piece of the pie while seeking new growth points for digital finance.

Circle is still waiting for more legislative guidance, especially on reserve reporting and liquidity requirements . Circle has always emphasized transparency and switched from Grant Thornton to Deloitte for audits to increase confidence in its reserves. Tether's transparency issues have long been controversial. While Tether claims that all of its USDT is backed by an equivalent amount of fiat currency reserves, there has been a lack of transparency about the specific details and independent audits of its reserves. In 2024, U.S. regulators are pushing for more transparency and compliance requirements, and Tether is expected to be subject to these requirements as well.

2. Private credit:

Through the tokenization of credit agreements, financial institutions provide loans to businesses through debt instruments.

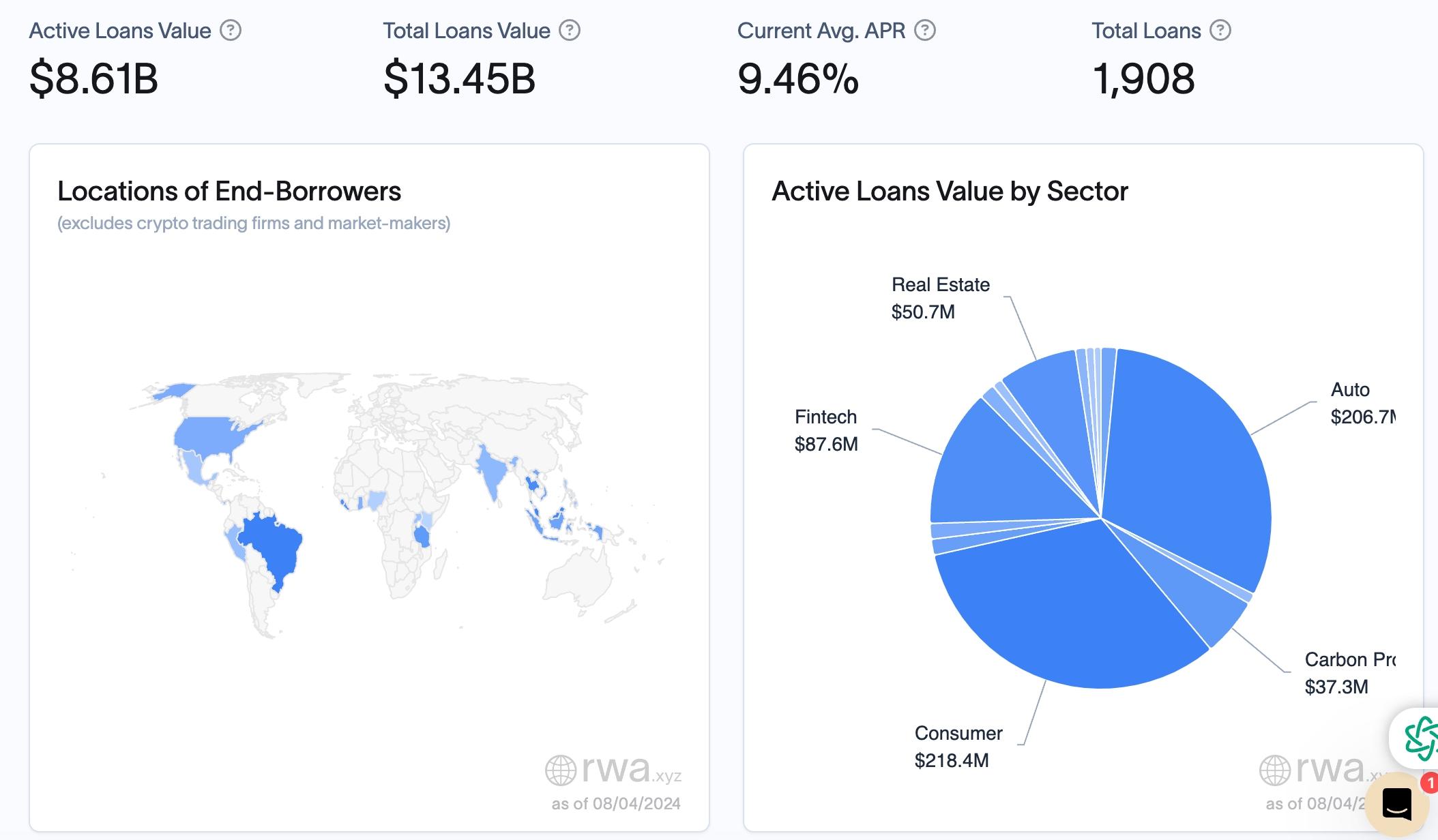

In traditional finance, private credit is a massive $1.5 trillion market. Crypto credit protocols have tokenized over $13 billion in loans, with over $8 billion currently loaned to real-world businesses, generating returns for on-chain lenders. For on-chain traders, private credit is attractive due to its higher yield potential. For example, lending stablecoins through protocols such as Centrifuge can earn an average annualized yield of 8.7%, exceeding the typical 4-5% annualized yield on platforms such as AAVE, but with increased risk.

Source: rwa.xyz

Consumer loans accounted for the largest share of $218.4 M in the entire loan portfolio, showing its strong demand in the overall loan portfolio. Automotive industry loans followed closely with an amount of $206.7 M. The amount of loans to the fintech industry was $87.6 M, which, despite its relatively small share, showed rapid growth, reflecting the impact of technological innovation on the financial market. Real estate, including residential and commercial real estate financing ($50.7 M) and carbon project financing ($37.3 M), although accounting for a smaller share, also plays an important role in its specific field.

The advantages of on-chain credit issuance and distribution are most evident in significantly reduced capital costs. More efficient institutional DeFi infrastructure can significantly save capital costs and provide new distribution channels for existing and new private credit products. Driven by the tightening of banking business, an important niche market is being opened up in the traditional financial sector. This shift to non-bank lending provides good opportunities for private credit funds and other non-bank lenders, attracting the interest of pension plans and endowment funds seeking smoother and higher returns.

Private credit, as part of alternative assets, has grown significantly over the past decade or so. Although it currently accounts for a relatively small proportion of the global debt market, it is an expanding market with huge room for growth.

Demand-side logic

1. Financing requirements:

Enterprises: In the real world, many enterprises (especially small and medium-sized enterprises) need low-cost financing to support operations, expansion or short-term capital turnover.

Difficulty in Financing: The loan procedures of traditional financial institutions are complicated and time-consuming, making it difficult for companies to quickly obtain the funds they need.

2. Credit Protocol Tokenization:

Tokenization: By tokenizing credit agreements, financial institutions can convert debt instruments into tokens that can be traded on the chain. These tokens represent debt instruments such as loans or accounts receivable of enterprises.

Simplified processes: Tokenization simplifies the financing process, allowing businesses to obtain funds faster and more efficiently.

Lender Logic

1. Related Opportunities:

Higher yields: Investing in private credit can often yield higher returns than traditional debt instruments because businesses are willing to pay higher interest rates in exchange for quick financing.

Diversify investment portfolio: Private credit provides users with diversification opportunities and spreads risk.

2. Risks and Challenges:

Difficulty understanding: Users may find it difficult to understand the workings of private credit, especially those involving off-chain assets.

Default risk: Users worry that borrowers may run away, resulting in loan defaults. In particular, if the off-chain asset audit is not transparent, borrowers may use a receivables voucher to borrow money on multiple platforms, increasing the risk of default.

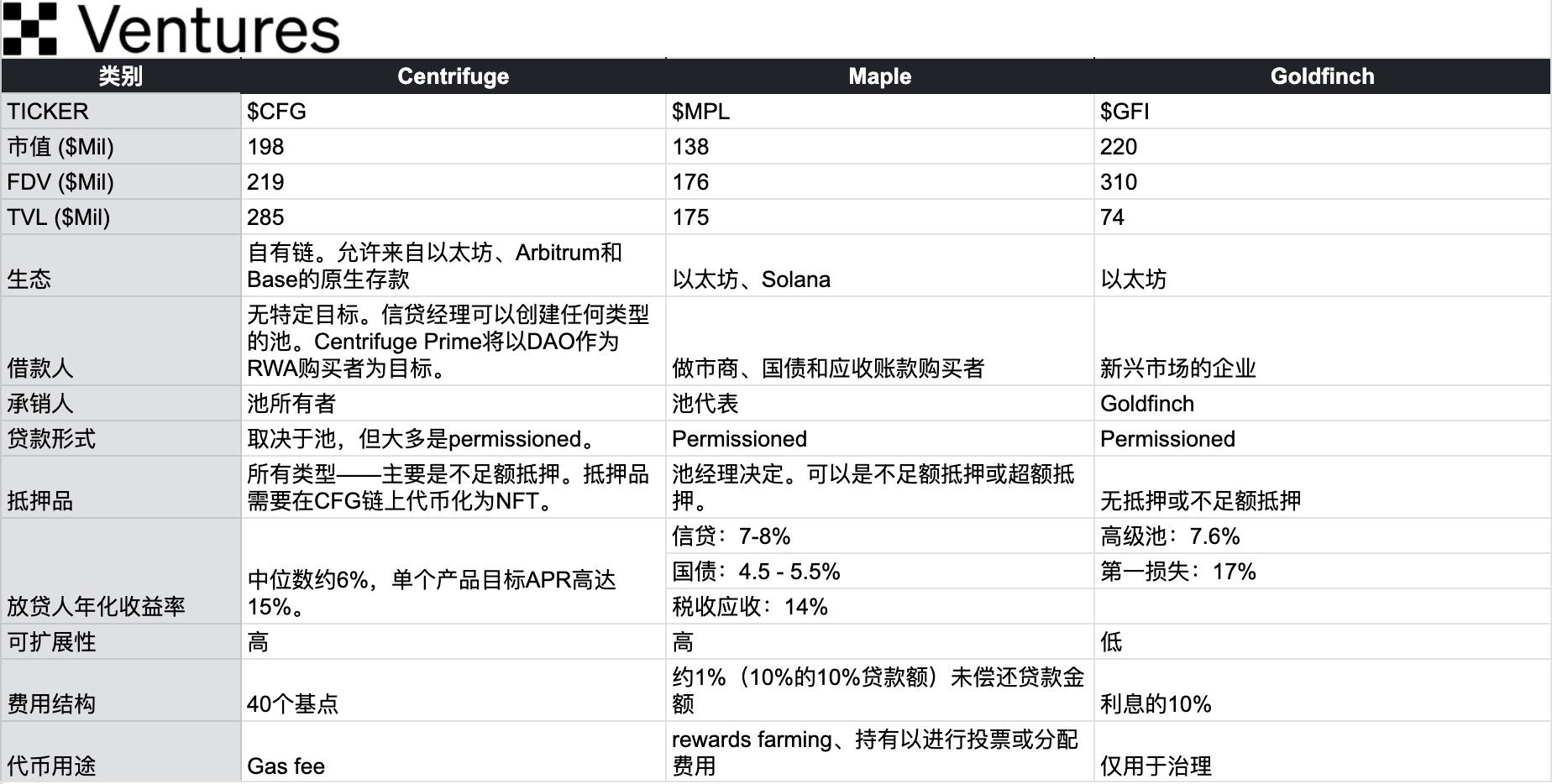

Representative projects:

1. Maple Finance: Provides on-chain private credit, and through tokenized credit agreements, it provides companies with rapid financing while providing lenders with high-yield investment opportunities. Similar models include TrueFi (which also provides U.S. Treasury products like Maple) and Goldfinch.

2. Centrifuge: Matching platform; tokenize accounts receivable and other debt instruments, match lenders and borrowers through the on-chain market, simplify the financing process, reduce financing costs, and meet the credit needs of small and medium-sized enterprises.

Source: OKX Ventures

Use cases for on-chain supply chain finance:

Automatic payment through smart contracts: After predefined conditions are met, smart contracts can automatically issue payments to suppliers. Set up a clear default handling mechanism, which is automatically triggered by smart contracts to protect user interests.

Invoice Tokenization: Invoices can be tokenized to facilitate their trading and provide liquidity to suppliers.

Transparent audit: Blockchain provides an immutable ledger, which simplifies auditing and due diligence. However, it is still necessary to conduct strict audits of off-chain assets through independent third-party auditing agencies to ensure the authenticity and uniqueness of assets and reduce the risks of multi-platform borrowing.

Risk assessment: Introduce a chain-based credit scoring system to conduct risk assessment on borrowing companies and help users make more informed decisions.

Problems solved on the chain:

Transactions are slow and opaque: Blockchain improves transparency and speeds up transactions in supply chain finance, benefiting all parties involved.

High transaction costs: Smart contracts can automate many processes in supply chain finance, reducing paperwork and middlemen, thereby reducing costs.

Credit access: DeFi can provide more democratic financing channels for small and medium-sized enterprises (SMEs) that traditionally have weak bargaining power.

3. Treasury bond products:

Tokenized government debt instruments. Referring to the concept of ETF, this type of asset can be likened to BTF (Blockchain Transfer Fund). The RWA U.S. Treasury product tokens on the chain represent the right to hold and distribute the income generated by these debts, rather than the ownership of the Treasury bonds themselves, which involves more deposits and withdrawals and compliance issues.

In a high-interest environment, some cryptocurrency players have begun to focus on traditional financial assets to achieve diversification. As interest rates rise, demanders seek safe and stable assets, and products such as government bonds naturally become their choice.

The wave of adoption of tokenized treasuries is driven by a combination of fewer DeFi yield opportunities (due to lower demand for on-chain leverage) and a shift in trader demand for short-term money-like instruments that benefit from tight U.S. monetary policy. This trend is also reflected in the large influx of off-chain bank deposits into money market funds, driven by low bank deposit rates and long-term exposure to unrealized asset losses. The emergence of institutional DeFi infrastructure is expected to further drive the growing global trend of demand for safe, income-generating, and liquid real-world assets.

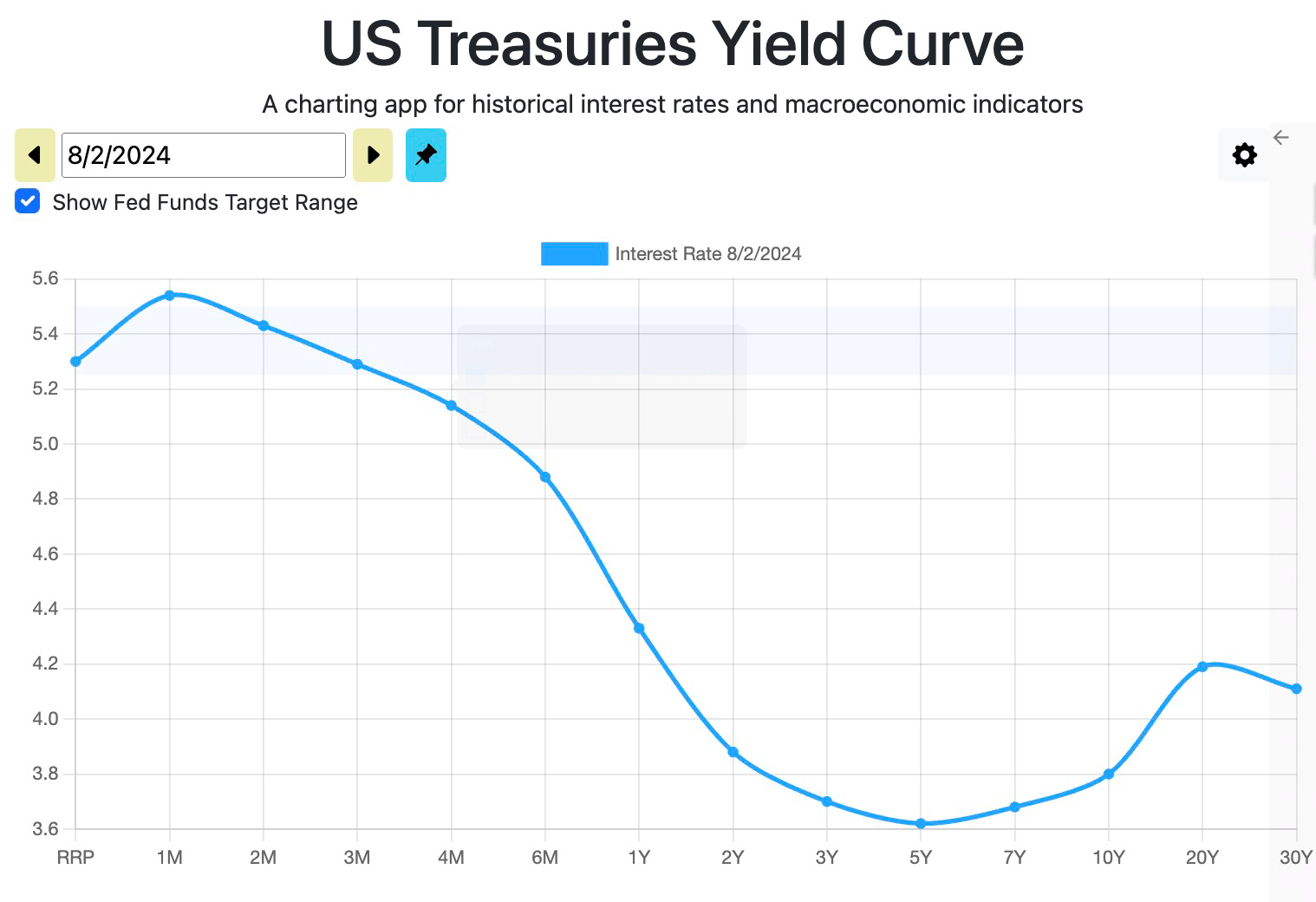

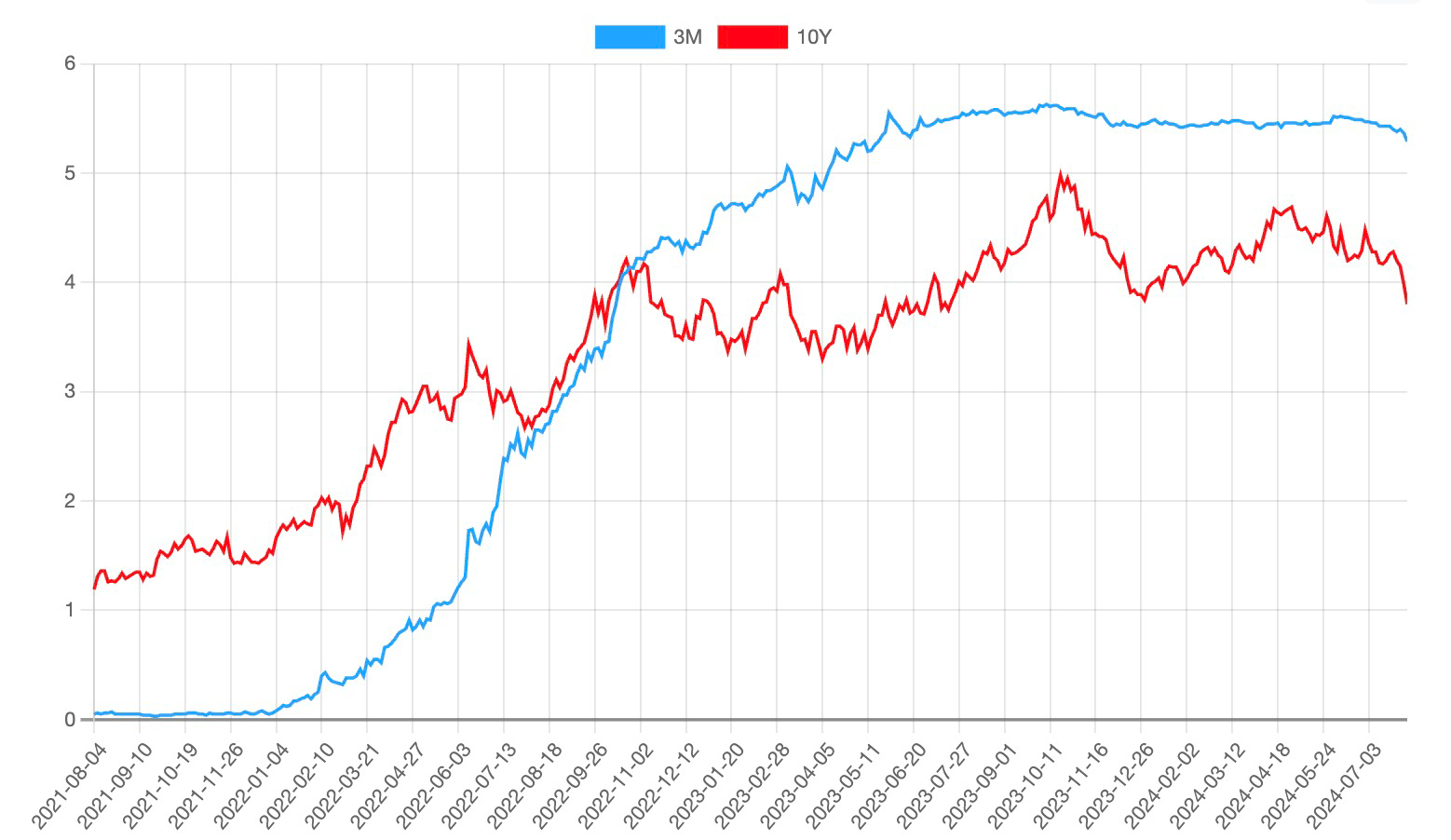

The current shape of the yield curve indicates that short-term interest rates are higher and long-term interest rates are lower. Most products choose to hold 1-month to 6-month Treasury bills, and some products even hold overnight reverse repo and repo securities in search of higher returns.

Why choose US bonds:

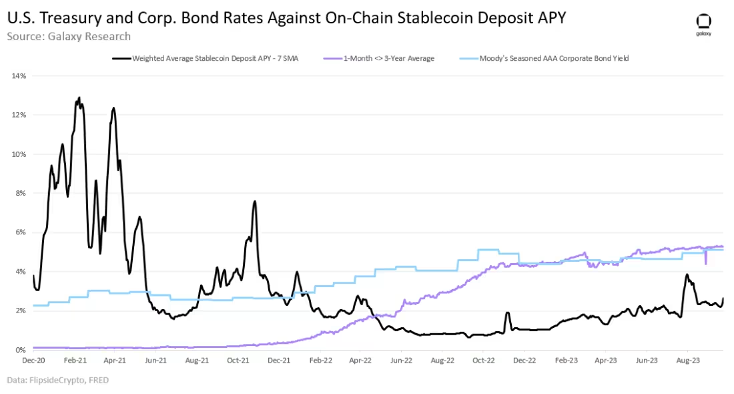

1. Yield: Short-term US Treasury bonds > AAA corporate bonds > DeFi stablecoin deposits (tokenized Treasury bonds are attractive)

Source: Galaxy Research

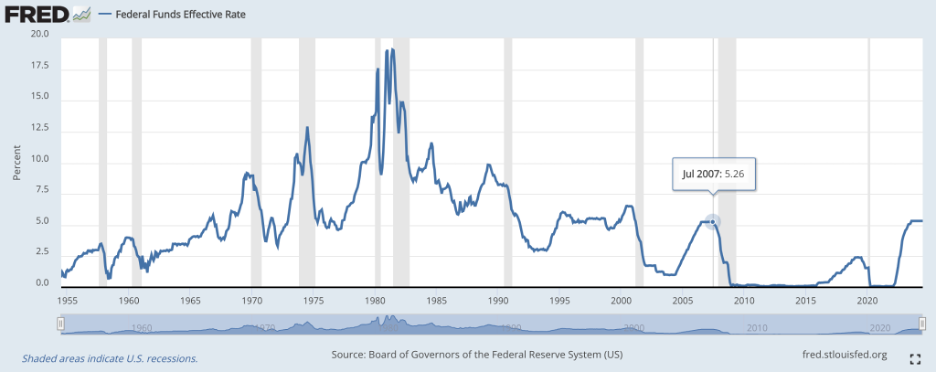

2. The Fed’s dramatic shift in monetary policy has pushed the benchmark interest rate to its highest level since 2007 (5.33). This has created new demand for certain types of RWAs for native-DeFi users seeking higher returns on crypto assets.

Source: fred.stlouisfed.org

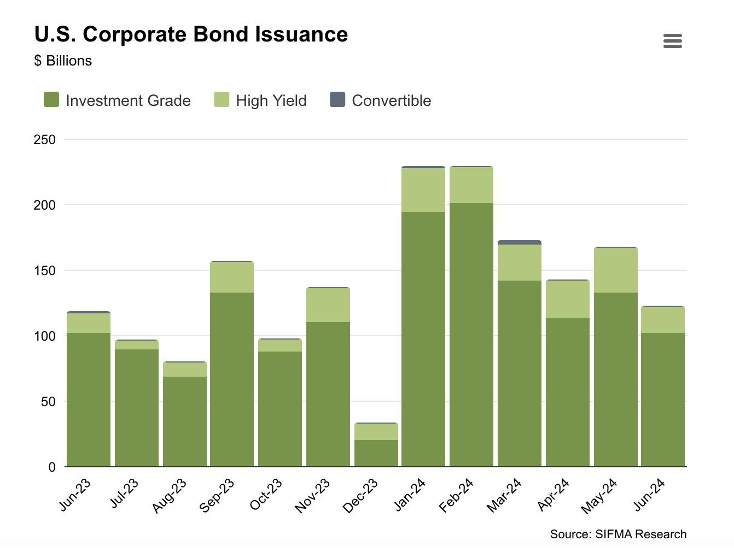

3. U.S. Treasury bonds are government-backed debt securities (widely considered a relatively safe and reliable type of income asset, with the only risk being a default by the U.S. government). In contrast, corporate bonds are debt securities issued by companies that may offer higher yields than Treasury bonds, but are also more risky. The global bond market size increased to approximately $140.7 trillion, up 5.9% year-on-year, indicating that the global fixed income market is still growing significantly. In the first two quarters of 2024 alone, U.S. companies issued $1.06 trillion in corporate bonds (more than the first three quarters of 2023 combined, $1.02 trillion).

Source: SIFMA Research

Rising interest rates have stimulated the launch of projects to tokenize U.S. Treasury bonds, such as:

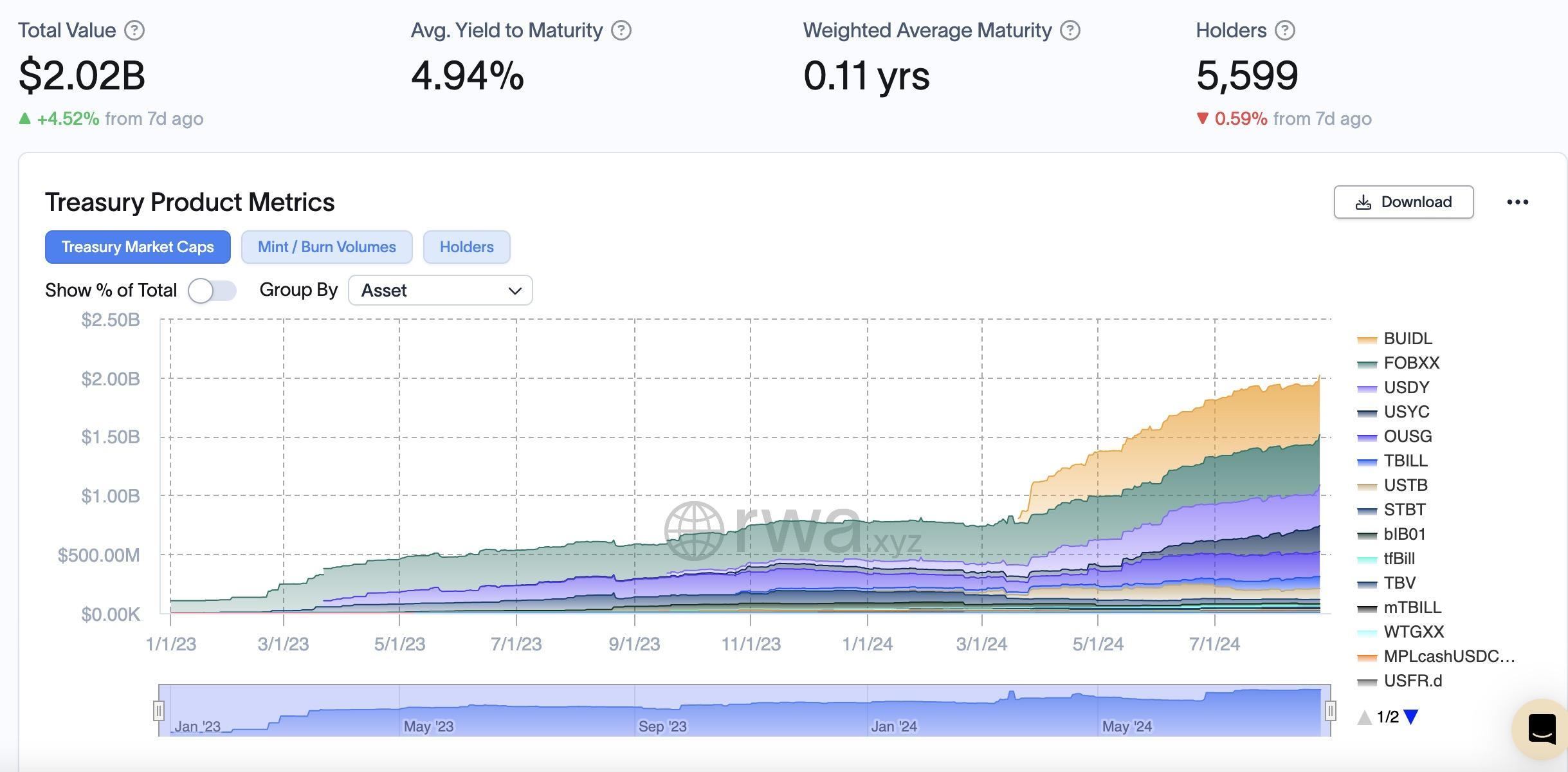

Franklin Templeton: Launched the Franklin On-Chain U.S. Government Money Fund (FOBXX) in 2021, the first public blockchain fund registered in the U.S. The fund has a yield of 5.11% and a market value of $400 million, making it one of the largest on-chain U.S. debt products.

BlackRock (Securitize): Launched the BlackRock USD Institutional Digital Liquidity Fund ($BUIDL) on Ethereum in March 2024. Currently, it leads the market with over $500 million in AUM.

Ondo: Launched the Ondo Short-Term U.S. Government Bond (OUSG) , which provides access to short-term U.S. Treasury bonds with a yield of 4.68% and a market cap of approximately $240 million. A large portion of OUSG is invested in BlackRock’s BUIDL. Ondo also offers the USDY yield stablecoin with a market cap of over $300 million.

As interest rates rise and U.S. bond yields become more attractive, this category has seen significant growth. Other projects include Superstate, Maple, Backed, OpenEden, etc.

Market value and market share:

Source: rwa.xyz

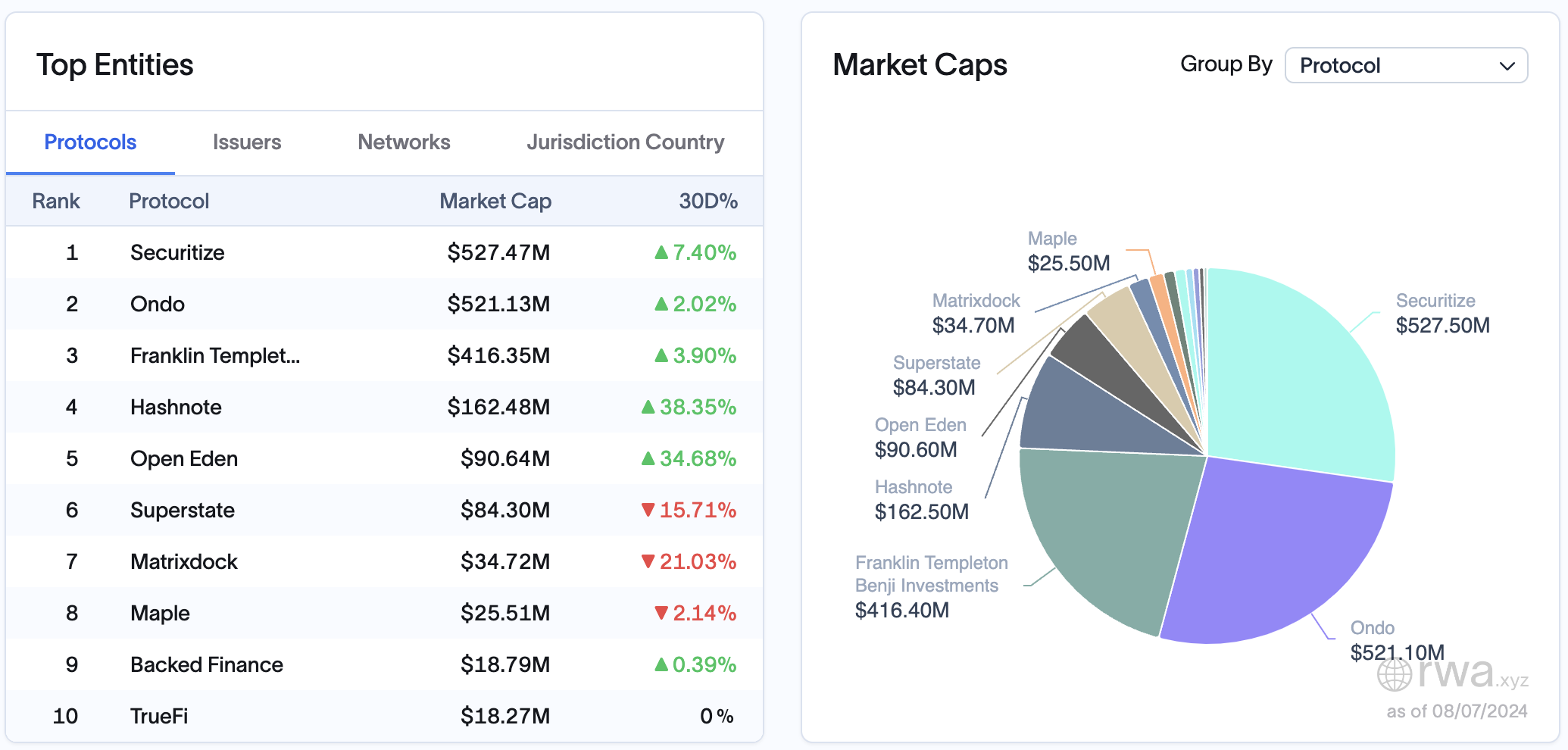

In terms of market capitalization, the top five protocols are Securitize, Ondo, Franklin Templeton, Hashnote and OpenEden; and the highest single product issuance is:

$BUIDL (BlackRock fund issued through Securitize), $510 Million, up 74% quarterly;

$FOBXX (Franklin Templeton), $428 million, up 12% quarterly;

$USDY (Ondo), $332 Million, up 155% quarterly;

$USYC (Hashnote), $221 Million, quarterly growth of 156%;

$OUSG (Ondo), $206 Million, quarterly growth of 60%;

$TBILL (OpenEden), $ 101 Million, up 132% quarterly.

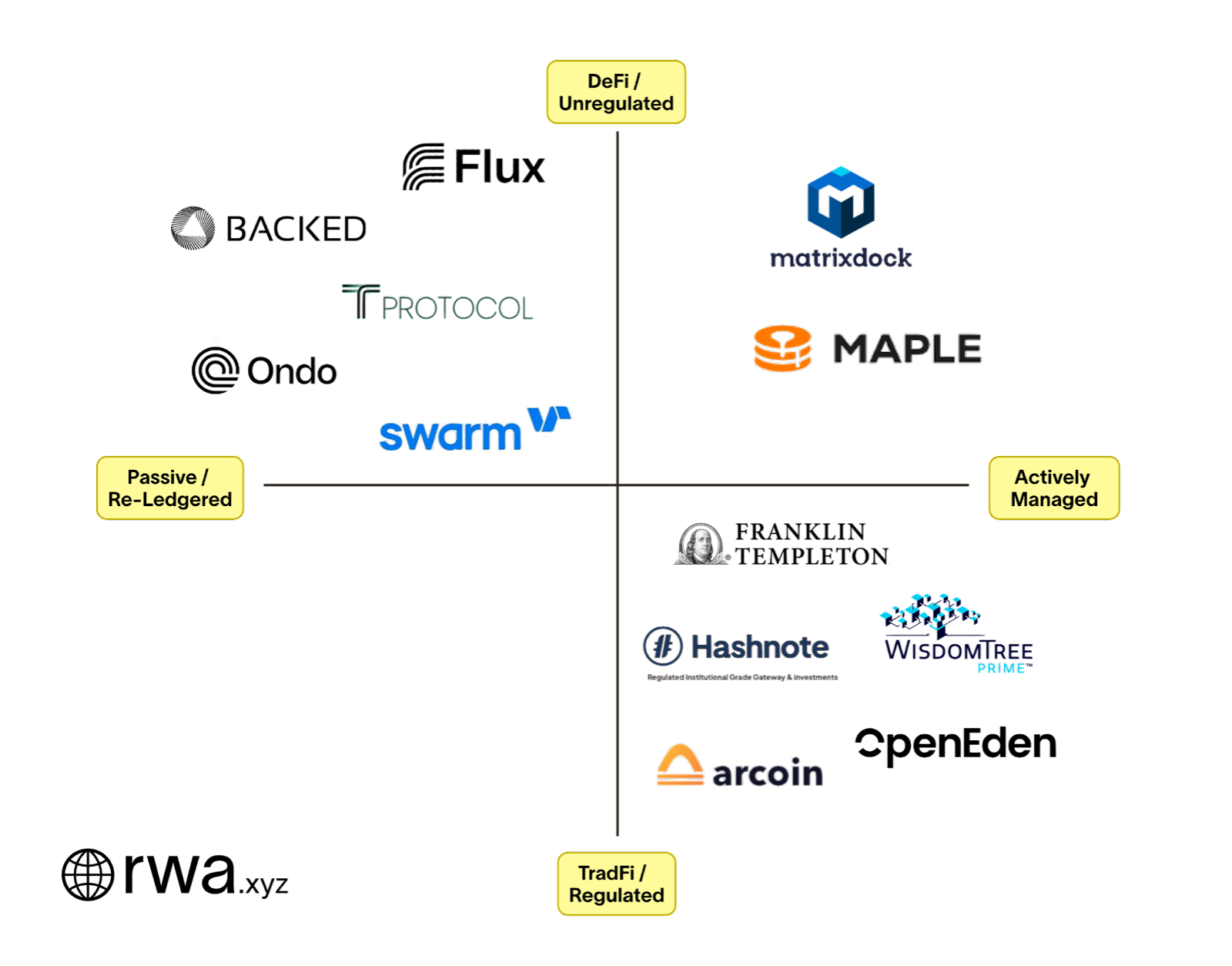

Asset Classification:

Actively Managed

Definition: U.S. Treasury products are actively managed by a portfolio manager designated by the company, who is responsible for managing the portfolio of underlying assets.

Features: Optimize returns and manage risks through active investment strategies, and the management method is closer to traditional actively managed funds.

Reledgered

Definition: U.S. Treasury products are designed to simply represent or mirror a financial instrument, such as a publicly listed ETF, which itself is not on-chain.

Features: Usually passively managed, its purpose is to re-register existing financial instruments through blockchain technology so that they can be traded and managed on the chain.

Source: rwa.xyz

Three companies, Ondo Finance, Backed, and Swarm, are all mirroring the BlackRock/iShares Short-Term Treasury Bond ETF. Ondo buys from a US issuer on Nasdaq (CUSIP: 464288679), while Backed and Swarm buy from an Irish issuer/UCITS (ISIN: IE 00 BGSF 1 X 88). To put it simply, Ondo does not actively manage a Treasury bond portfolio. Instead, it "outsources" the management to SHV, which in turn is managed by BlackRock/iShares. Companies like Ondo will act as distributors for BlackRock because DeFi protocols will not interact directly with asset managers. This is simpler for BlackRock, which does not have to manage the compliance of thousands of projects that want exposure to its funds.

Source: OKX Ventures, rwa.xyz

For each product under the agreement, institutions and qualified investors can make corresponding decisions based on the three most important criteria: 1) principal protection; 2) return maximization; 3) convenience.

Principal Protection:

Some large institutional products operate in regulated jurisdictions, ensuring minimal legal and compliance risks; they rely on regulated fund managers and custodian service providers, providing greater transparency and investor protection. Some other products rely more on investment managers to perform their management duties, and investors need to carefully evaluate the legal environment and regulatory situation in the jurisdictions where these products are located.

Yield Maximization:

Actively managed products rely on the investment strategy and execution capabilities of fund managers to optimize the portfolio and maximize returns. These products are mainly concentrated in short-term Treasury bonds and repurchase agreements, which are in line with the current yield curve shape. Re-registered products outsource portfolio management to ETF managers. Investors can directly view the historical performance of these managers and choose products that match their return goals and risk preferences.

Convenience:

Some large institutional products provide access through official mobile applications, which enhances the user experience, simplifies the investment process, and is suitable for self-managed retail investors. Some other product processes are more complicated, involve multiple steps of manual operation, and require a high learning cost.

In the future, actively managed products may weaken the competitive advantage of on-chain re-registration products by compressing their pricing. In addition, users should also consider whether these US Treasury tokens are simply used as certificates of their investment holdings, or whether they can also be used as payment tokens or collateral to expand usage scenarios and increase income sources.

4. Commodities

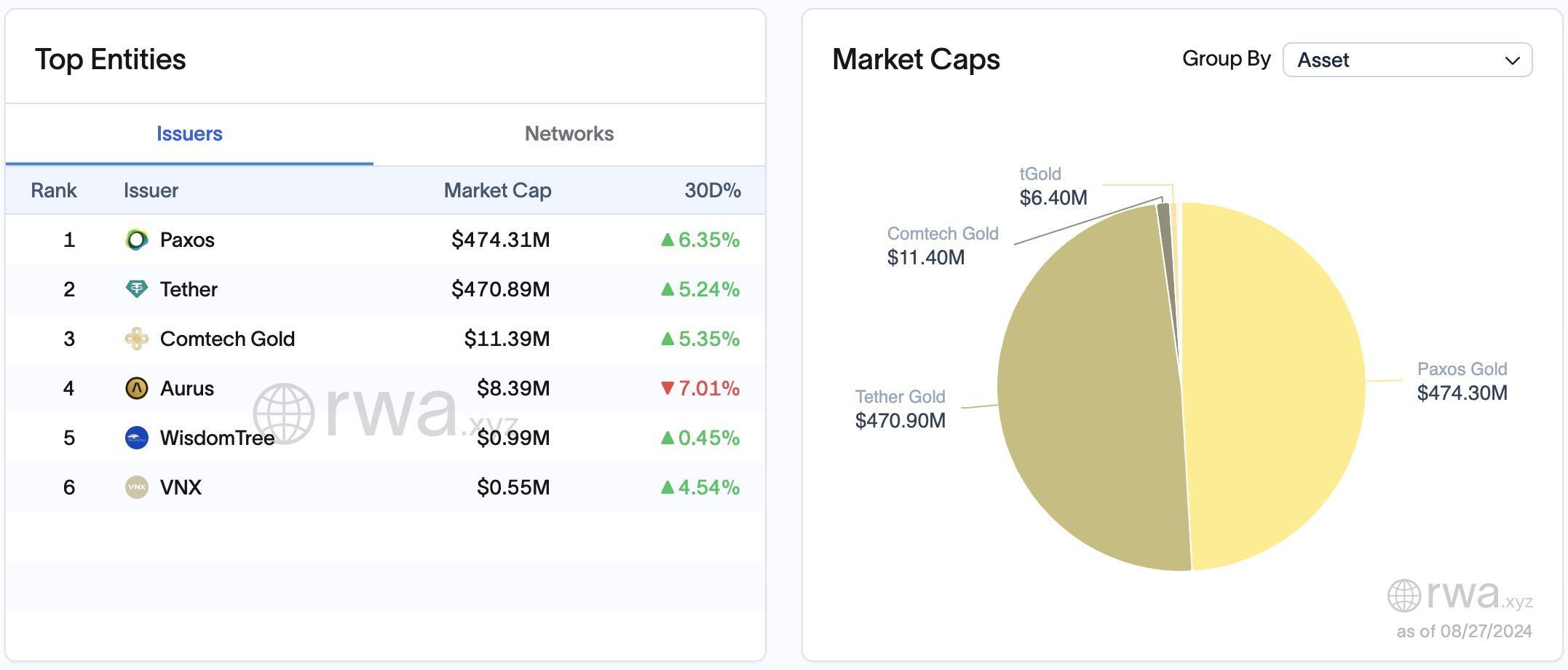

Tokenization of natural resources represents the rights and interests of actual commodities. The total market value of the current commodity token market is close to $1 billion, among which precious metals (especially gold) have received the most attention. Gold-backed stablecoins such as PAX Gold (PAXG) and Tether Gold (XAUT) account for nearly 98% of the market value of the tokenized commodity market. With the price of gold breaking through $2,500 per ounce, the total market value of gold in the world has exceeded $13 trillion, which also provides a huge market space for the tokenization of gold and its integration in DeFi platforms.

Source: rwa.xyz

Other metals taking market share include silver and platinum. As the RWA tokenization space matures, we may see tokens for other commodities (such as crude oil) and even crops. For example, farmers in Uganda could use the same financial tools as traders in New York to manage their coffee crops, thereby expanding market access. There is an opportunity for global trade to move more to blockchain.

5. Real Estate

Tokenizing physical assets such as homes, land, commercial buildings, and infrastructure projects. Making real estate tradable on-chain through tokenization introduces a novel investment model that improves accessibility, enables fractional ownership, and has the potential to increase liquidity. Nonetheless, real estate’s inherent illiquidity has limited the pace of its on-chain adoption. The long-term nature of real estate transactions and the small size of buyers make it challenging to connect sellers with buyers on-chain, especially given that the industry has traditionally operated on legacy systems.

Difficulty and Challenges:

1. Market demand:

Real estate market conditions: The success of tokenized real estate projects depends largely on the health of the real estate market. In some areas with depressed real estate markets (such as parts of Japan and Detroit), the lack of speculative value and investor interest makes it difficult for tokenized projects to attract enough buyers and investors.

2. Long-term rental income distribution:

Ongoing management: Tokenized real estate involves the distribution of long-term rental income, which requires ongoing property management and maintenance. This increases the complexity and cost of operations and requires the support of a professional team to ensure the stability of rental income and the preservation of property value.

Operational friction: Difficulty in depositing, withdrawing and redistributing rent in legal currency, verification of whether rent is actually paid and information transparency.

3. Insufficient liquidity:

Transaction Challenges: While tokenization increases accessibility and fractional ownership of real estate investments, the inherent illiquidity of real estate limits the speed of its on-chain adoption. The long-term nature of real estate transactions and the small size of buyers make it challenging to connect sellers with buyers on-chain.

Traditional Operations: The industry has traditionally operated on legacy systems, and switching to a blockchain platform requires time and adaptation, especially for market participants who are accustomed to traditional transaction models.

Platforms such as RealT and Parcl are committed to injecting liquidity into the market by simplifying property division, allowing sellers to easily divide their assets and obtain tokenized shares. In addition, the Parcl platform also allows users to speculate on the value of real estate in different locations (such as different US cities) through its on-chain trading mechanism, further broadening the investment channels in the real estate market.

6. Stock Securities:

Security Token Offering is essentially the tokenization of some assets or rights that are difficult for traditional companies to IPO through blockchain technology, allowing users to invest in corporate securities by purchasing these tokens. However, the STO track has been around for quite some time, and many listed companies in STO projects are traditional companies, which often lack novelty and high growth potential, and are therefore not attractive enough to investors. In addition, STOs usually only allow users who have passed KYC verification to participate in transactions, with high investment thresholds and greater transaction complexity, and face compliance and regulatory barriers, and it is very difficult to comply with laws across jurisdictions.

In contrast, direct crypto tokens are more flexible and active in trading, and often offer more profit opportunities. Therefore, they are far more attractive to many users than STOs.

Operational model, Source: Tiger research

Some projects such as Swarm and Backed have broken through regulatory restrictions and allowed global stocks and funds to be traded on the chain, such as COIN and NVDA in the US market, and index funds such as the core S&P 500. By tokenizing the income rights of equity and funds, Solv Protocol can also create FNFTs representing stocks and funds, making these assets tradable on the DeFi market; and also provide compliance tools for these assets, ensuring that all transactions comply with regulatory requirements through smart contracts and on-chain identity verification (such as KYC/AML).

Difficulty and Challenges:

However, the business model of tokenizing existing securities is not competitive and attractive enough in the long run, especially after global financial giants enter the market. In the face of competition from large asset management companies, the initial profit model of charging service fees is difficult to maintain, the market will enter a price war, and the profit margin will be compressed.

Hypothetically, tokenizing existing securities (e.g. Tesla stock) could make money by charging users a service fee (let’s say 5 basis points). These fees are charged by the provider of the tokenized service for handling and managing these tokens. However, if such a service becomes very popular and gains a large number of users, large global asset management companies (such as Blackstone Group, etc.) may enter this market. These large companies have stronger capital and resources and can provide the same service at a lower fee. As more companies enter the market, the fees for providing tokenized services will gradually decrease, which may eventually trigger a price war (race to the bottom), that is, competitors continue to lower fees to attract more customers. This will make the model that initially made money by charging service fees unsustainable, because higher fees will be replaced by lower fees, eventually resulting in meager or even disappearing profits.

3. Future Prospects

Integration of DeFi and RWA: The combination of DeFi protocols and tokenized assets is one of the main trends in the future. By integrating DeFi protocols with tokenized assets, such as allowing U.S. Treasury tokens to be mortgaged and borrowed, more financial products will achieve composability and instant liquidity without redemption, which will stimulate the flywheel effect in the DeFi field. In particular, the combination of licensed products leveraging unlicensed products will bring a wider range of application scenarios and promote the growth of TVL. This innovation will not only attract institutional clients, but also a wider range of crypto users, especially in the fields of payment and financial services, where tokenized assets are expected to replace the role of some centralized stablecoins.

Emerging services and professional needs: As asset tokenization progresses, new service providers will emerge to meet the demand for professional skills and knowledge. For example, smart contract legal experts, digital asset custodians, on-chain financial managers, and blockchain financial reporting and monitoring providers will become key players in driving the market to further mature. At the same time, the improvement of institutional compliance and regulatory frameworks will bring greater market access and trust to these service providers. It is arguable that anonymity may become an increasingly scarce asset in the future as institutional participation and regulatory transparency requirements continue to increase.

Cross-border transactions and global markets: The cross-border transaction capabilities of blockchain technology will further promote the entry of tokenized assets into the international market and simplify the traditional international asset trading process. This is particularly important for emerging markets, enabling them to attract global capital and drive economic growth. In the future, RWA projects that can help achieve seamless interoperability between different blockchain platforms, especially those that provide a wider range of asset selection and optimize liquidity, will have a clear competitive advantage.

Technological Advancement and Process Optimization The success of RWA tokenization depends heavily on efficient and secure technology. With the advancement of blockchain technology, especially in terms of scalability, security, and standardized protocols, RWA tokenization will become more efficient. The development of new protocols will simplify the tokenization process, enhance interoperability between platforms, and provide users with a more user-friendly experience. These technological advances will continue to drive the growth of RWA adoption in various industries, ultimately reshaping the landscape of the global financial industry.

Reference:

https://www.coindesk.com/opinion/2024/05/07/blackrock-ondo-superstate-the-biggest-movers-in-the-rwa-sector-in-q1/

https://www.steakhouse.financial/projects/tokenized-tbills-2023

https://areteresearch.substack.com/p/the-real-world-asset-thesis-the-next

https://www.galaxy.com/insights/research/overview-of-on-chain-rwas/

https://docs.openeden.com/treasury-bills-vault/introduction

https://www.ustreasuryyieldcurve.com/

https://dune.com/lindyhan/ondo-usdy-ousg

https://thedefiant.io/news/research-and-opinion/centrifuge-quietly-sets-pace-in-real-world-assets-race

https://reports.tiger-research.com/p/how-mantra-is-leading-the-rwa-market-eng

https://transak.com/blog/transak-state-of-rwa-tokenization-report-2024

https://www.rwa.xyz/blog/tokenized-treasuries-report

Disclaimer

This article is for reference only. This article only represents the author's views and does not represent the position of OKX. This article is not intended to provide (i) investment advice or investment recommendations; (ii) an offer or solicitation to buy, sell or hold digital assets; (iii) financial, accounting, legal or tax advice. We do not guarantee the accuracy, completeness or usefulness of such information. Holding digital assets (including stablecoins and NFTs) involves high risks and may fluctuate significantly. You should carefully consider whether trading or holding digital assets is suitable for you based on your financial situation. Please consult your legal/tax/investment professionals for your specific situation. Please be responsible for understanding and complying with local applicable laws and regulations.