Table of contents

Table of contents

introduction

introduction

Development of Decentralized Derivatives Exchange

Why does the Crypto market need derivatives?

Historical Data Review

Decentralized Perpetual Contract Trading Protocol

Why do we need a decentralized derivatives exchange?

What are the current challenges facing decentralized derivatives exchanges?

Head project research and data analysis

Future direction

Waves

final summary

Summary

Crypto derivatives trading first started in 2011, but a new chapter was officially started after BitMEX invented the perpetual contract. The market blossomed in 2019, and the bull market will reach the peak of trading volume in 2021

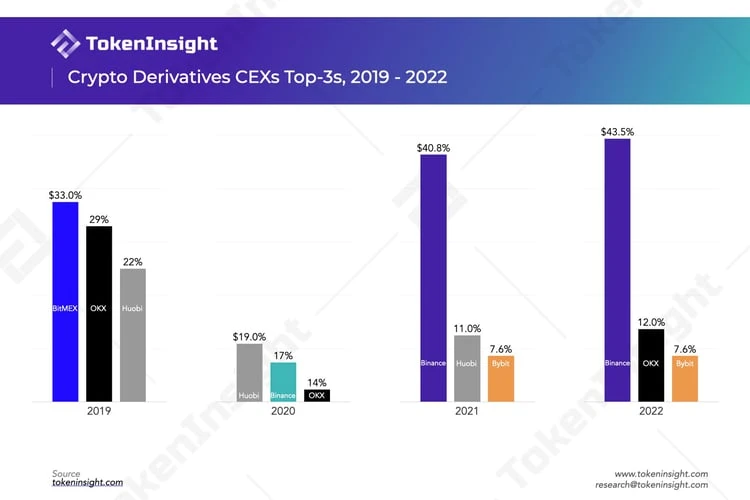

The top three derivatives exchanges in 2019 are BitMEX, OKX, Huobi; in 2020 they are Huobi, Binance, OKX; in 2021 they are Binance, Huobi, Bybit, in 2022 they are Binance, OKX, Bybit (FTX originally had a place)

Decentralized derivatives exchanges have obvious advantages over traditional centralized derivatives exchanges in terms of asset transparency, user asset control, anti-censorship/privacy, and on-chain composability.

Insufficient liquidity, high transaction costs, low product usability, and poor feature richness are the main problems faced by decentralized exchanges

Over the past roughly 10-month period, the total trading volume on decentralized derivatives exchanges reached $478 B. While this figure is roughly equivalent to two weeks of Binance derivatives trading volume in the current market environment, this figure was essentially zero at the beginning of last year

dYdX will be the leading decentralized exchange before Q3 in 2022, but there are signs of being surpassed by GMX in terms of trading volume after Q3; it has been surpassed by GMX in some cases in terms of platform revenue, and GMX has already ranked first in terms of TVL

According to the current market development trend, the market size of decentralized exchanges is expected to increase by more than 10 times within a year

From the perspective of decentralization, dYdX is the lowest compared to GMX, Perpetual and Drift. At the same time, the vAMM mechanisms of Perpetual and Drift are less adaptable to the market than the other two protocols

From the perspective of fee structure, compared with GMX and Perpetual, the source of fees is more abundant, which provides assistance for the good development of the agreement, and the fee model is also better, which is conducive to user incentives. dYdX keeps all platform revenue for itself

dYdX, GMX, and Perpetual all have well-established token economies, encouraging users to participate in protocol governance and token staking. However, in terms of effect, dYdX and Perpetual will be slightly inferior to GMX, mainly because the actual income received by users after participation is lower

The next development direction of the decentralized derivatives exchange mainly includes providing more diverse trading mechanisms and products, striving for market share, deploying new chains, and realizing the concept of complete decentralization (especially dYdX), etc.

introduction

introduction

FTX Sued for Misappropriation of User Fundsfile for bankruptcy, causing approximately $8 billion in user funds to be irretrievable, and millions of users being affected had a dramatic impact on the industry. As the fuse of the incident, the entire Crypto market has gradually escalated concerns about the security of users funds. Affected by this, more and more centralized exchange users withdraw their funds deposited in institutions. At the same time, in order to enhance user confidence and enhance their own transparency, some exchanges have also gradually carried out Proof of Reserve or issued audit reports, and disclosed the wallet addresses of exchanges.

Although such measures can alleviate the anxiety of the market to a certain extent, the sluggish market is still sending a cold signal. Affected by FTX, other centralized exchanges have also experienced a so-called liquidity crisis, and have suspended withdrawals and even rumors of bankruptcy. As the Vice President of AAX Exchange has announcedresign, its exchange has withdrawn coins since November 13Suspend withdrawalSince then, as of the 29th, the withdrawal has not been resumed. Japan ExchangeBitfrontannounced the cessation of operations. Genesis hiredrestructuring consultant, it is rumored that it will go bankrupt and reorganize.BlockFiAlso filed for bankruptcy reorganization on the 28th.

The so-called a gentleman does not stand under a dangerous wall, given the choice, many users will still choose to transfer their assets to a place where they are more at ease.

For the needs of transactions, inCentralized exchange, and then traded on the exchange. After DeFi Summer, decentralized exchanges developed rapidly, and were quickly welcomed by users because they solved the liquidity problem of long-tail currencies. At the same time, the liquidity of some mainstream currencies is no less than that of centralized exchanges. Therefore, decentralized spot exchanges have become the choice of many users. Users no longer need to deposit funds in centralized institutions, but can complete transactions by storing them in their own wallets.

The liquidity of spot trading is slightly easier to solve than derivatives, and AMM (Automated Market Maker, automated market maker) is slightly weak in derivatives trading. The vAMM that had been tried before also failed because the assets in the pool were seriously tilted when the market price was unilaterally trending, and the transaction price could not be anchored to the index price.

Since the outbreak of Crypto derivatives trading in 2019, the market size has continued to expand, and more and more companies have emerged and focused on this field. In the decentralized world, there have also been a large number of protocols focused on derivatives trading since last year. As a product with strong user demand, the decentralized derivatives exchange still has a big gap from the centralized products so far. But maybe this is where the opportunity lies, decentralized derivatives trading has not yet emerged a similarUniswapProducts appear, and more and more protocols are added continuously.

This is the purpose of our writing this report. We hope to sort out the market situation of decentralized derivatives exchanges, especially the most popular perpetual contract products. The report will clarify the status quo of decentralized perpetual contract transactions from several leading protocols, including dYdX, GMX, Perpetual Protocol, etc., conduct data analysis, and look forward to the future development trend of this segmented track.

Development of Decentralized Derivatives Exchange

A Brief Review of the History of Crypto Derivatives Trading

The first Bitcoin derivatives trading platformICBIT was born in 2011, providing delivery futures trading mainly based on Bitcoin. Subsequent exchanges such as Huobi and OKEx also imitated and launched similar delivery products. The derivatives trading market at that time was still in its infancy, and the market size was small.

BitMEXIt is a key exchange that truly develops and expands Bitcoin (Crypto) derivatives trading. Founded in 2014, BitMEX only offered delivery futures trading of Bitcoin at the beginning. Until 2016, BitMEX invented the Perpetual Swap, a futures contract with no expiration date. The two parties to the transaction pay the Funding Fee to narrow the gap between the futures price and the spot index price as much as possible.

At the end of 2017, CBOE and CME also began to provide digital currency derivatives transactions, and they are also the first batch of compliant digital currency derivatives exchanges.

After 2019, Crypto derivatives transactions began to explode. In that year, the Crypto derivatives trading market was mainly composed of BitMEX,Huobi DMas well asOKExoccupied.

The DeFi Summer that started in 2020 ignited Ethereum, making $ETH a popular asset besides Bitcoin, and the huge fluctuations also made it amplify the trading volume in the derivatives trading market.

In August 2020, Binance released two contract products, U-based and Coin-based. Among them, coin standard is an inverse contract (Inverse contract), which means that the collateral and settlement are all in digital currency; while the U standard contract is a product that uses legal currency/stable currency as collateral assets and settlement, which is more similar to traditional financial the form of the industry.

In April 2021, the dYdX Layer 2 product will be officially released, allowing perpetual contracts to be traded on a decentralized platform. In August of the same year, the dYdX Foundation issued $DYDX as a platform incentive, and the trading volume subsequently increased significantly.

In September 2021, GMX officially released products on Arbitrum, which supports users to participate in spot and perpetual contract transactions of some currencies, and can also participate in market making by minting $GLP. The Avalanche version of the product will be available in January 2022.

Founded in May 2019, the FTX exchange reached its peak two years later with more than 1 million users. But in November 2022, due to misappropriation of user funds and large losses, FTX applied for Chapter 11 bankruptcy proceedings.

Why does the Crypto market need derivatives?

hedging risk

The demand for derivatives in the Crypto market is similar to the demand for derivatives in the traditional financial market, the most important of which is risk hedging. For example, for miners, the number of bitcoins they will obtain in the future is basically certain, and the cost of mining is also predictable, but the price of bitcoins cannot be predicted. In order to eliminate such uncertainty, miners can use Bitcoin derivatives transactions to lock in future prices while guaranteeing their own profits.

There are many similar trading behaviors. For example, for currencies with high demand in a short period of time, such as participating in the IEO of the exchange, or participating in public chain node voting, a large number of currencies are required. And these coins may experience huge price fluctuations before and after the event. By using derivatives transactions, you can eliminate the risks brought about by these fluctuations to a certain extent and manage your own risk exposure.

speculate to make money

Crypto transactions are different from traditional financial industries. Crypto supports 24*7 uninterrupted transactions and has greater volatility. This also makes this market a paradise for speculators. The flexibility of derivatives trading itself has attracted a large number of speculators to make money through the limited margin and the characteristics of fighting big with small things in contract trading.

Increase leverage to magnify returns

The leverage of Crypto derivatives trading is generally high. The highest leverage of 500 times has appeared in the market, and there are many users who trade with 100 times leverage. When the market volatility is relatively high, higher leverage can bring more potential returns (of course, it also brings higher potential risks). And when the market is deserted, it can also artificially create fluctuations by increasing leverage.

The use of high leverage in the Crypto market is a common situation, which is why the average usage period of a contract user is not long.

Historical Data Review

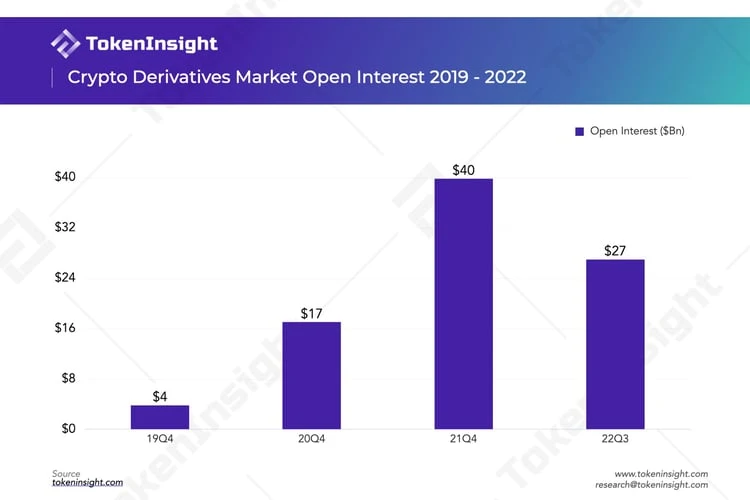

We have summarized the historical transaction data of Crypto derivatives. As we said before, the derivatives exchange market will be officially opened after 2019 and will reach its peak during the bull market in 2021.

From the perspective of quarterly transaction volume, the transaction volume in Q1 of 2019 was only $264 B, and it increased nearly 8 times in Q1 of 2020. By Q1 of 2021, the transaction volume reached an astonishing $16,590 B, which is the highest in Q1 of 2019. 62.8 times.

If you are interested in previous derivatives reports, you can click on the link below to view:

TokenInsight 2021 Digital Asset Trading Annual Report

TokenInsight 2020 Digital Asset Futures Exchange Annual Report

After peaking in Q2 2021, the trading volume of derivatives will begin to decline. In Q4 of the same year, the transaction volume was only about half of Q2. With the end of the bull market in Q4 last year, the follow-up transaction volume continued to shrink. But since this year fromTerracollapse to 3 ACBankruptcy, FTX filed for bankruptcy protection and other incidents continued. Although the price continued to fall, the violent fluctuations also caused the transaction volume to decline, but it did not shrink very much.

The historical trend of total open interest in the market is also roughly the same as the trend of trading volume. Despite the recent degree of deleveraging in the market, the current level of open interest is still about 7 times that of the same period in 2019.

In terms of market share, we selected the top three in the derivatives market in the past four years, and their market shares are shown in the figure below.

Before 2020, because the birthplace of perpetual contracts was BitMEX, BitMEX has always occupied the largest market share. After 2020, centralized derivatives exchanges will flourish, and the market concentration will decrease compared to before. At that time, Huobi occupied the first position in the market, followed byBinance, OKX (also known as OKEx at the time), these three were also called the Big Three at the time. After 2021, with the efforts of Binance, it began to surpass other exchanges and firmly occupied the first position in the market. In addition, as Huobi announced its withdrawal from the Chinese mainland market and cleared its users that year, although it was still in second place, it was far behind Binance. Huobi’s trading volume had dropped a lot in the fourth quarter of that year.

OKX has performed well this year. Although it is also affected by the policies of mainland China, OKX will start to focus on overseas markets in 2022. At the same time, after the incident of FTX misappropriating user funds, it reacted quickly and quickly announced the wallet address of the exchange and the wallet address that users can verify by themselves.Asset Merkle Tree Proof. It has become the second place in the market share of derivatives.

Decentralized Perpetual Contract Trading Protocol

In a real sense, it should mark the start of decentralized derivatives trading after Layer 2 officially starts operation. The two main representatives are the launch of dYdXs Layer 2, and the deployment of GMX and Perpetual Protocol on Arbitrum. Of course, we mainly discuss trading products of the perpetual contract type here, and options, synthetic assets and other categories are not considered for the time being.

After dYdX issued $DYDX in August 2021, the trading volume on its platform also increased significantly. On August 1st,Cumulative trading volume on dYdX is $3.4 B, 4 months later, that is, at the end of the same year, the cumulative transaction volume has reached $322.6 B, an increase of nearly 95 times.

And the average daily trading volume of GMX in the last two months is about $250M. Compared with centralized exchanges, this figure is almost half of the trading volume of BitMEX exchange (2022.12.1).

The above data on decentralized perpetual contract transactions was almost zero at the beginning of last year. According to the data collected by TokenInsight, we have found more and more decentralized protocols focusing on this field, and we will see more in the future. Of course, we also have reasons to believe that the trading share of decentralized derivatives in the future will be the same as that of spot trading, from a small business to becoming an important part of the market composition.

Why do we need a decentralized derivatives exchange?

Advantages of decentralization

Decentralized protocols tend to provide greater transparency

All transaction data on DEX is transparent and open, and anyone can check every transaction record on the blockchain browser. Through on-chain data analysis, users can even gain insight into many valuable first-hand information, such as observing giant whale transactions, identifying rat warehouses, verifying whether there is Wash-Trading on the exchange, and so on. In CEX, every transaction of the user and information such as the exchanges capital reserves will not be made public. Similar to a black box, users need to fully trust CEX, and this also gives CEX many possibilities for doing evil.

Decentralized protocol allows users to maintain control of their assets at all times

walletwallet, and have control over their own funds (Self-Custody).

Decentralized protocols improve censorship resistance/privacy

As the economic and political influence of cryptocurrencies continues to expand, government regulation is also showing increasingly stringent trends. Due to the characteristics of its own corporate entity, CEX is more likely to be subject to the laws and regulations of the country where the business is located, such as KYC (Know Your Customer) and Anti-Money Laundering (AML) (Anti-Money Laundering), etc. Users are often required to upload personal information, certificates, etc. when registering . American users even need to complete annual tax declaration work like stock trading in CEX transactions with national licenses. And DEX can be regarded as an agreement composed of codes, not a corporate legal person, so it is naturally resistant to censorship, and users hardly need KYC certification.

On-chain composability

becauseDEXDue to the permissionless feature, many DEX products can not only be regarded as a separate product, but also can be accessed by other application layer DeFi products and provide underlying liquidity. In this way, DEX is in the liquidity layer between the blockchain and the application layer. In the future, it can play a role similar to Lego building blocks in the DeFi ecology, with extremely high chain composability. Below we take GMX as an example to analyze.

yield aggregator

In July 2022, Umami Finance launched in partnership with GMX and TracerDAO (now renamed Mycelium)USDC Vault, the principle is that 50% of the $USDC deposited by the user will be mint to obtain income for $GLP, and the other 50% will be used to hedge the risk exposure of $GLP in TracerDAO. In Q4 of the same year, Umami Finance will launch GLP Vault.

At the same time, as of November 23, 2022, Umami has helped GMX attract up to $160,000,000 in transaction volume through GMXs Referrals program (that is, new users who use the umami referral code can get a 10% fee discount) To GMX, $18,000 was awarded, and all will be deposited into the Treasury.

DeCommas

DeCommas is a cross-chain DeFi automation layer. It develops a set ofDelta neutral strategy, that is, 50% of the $USDC deposited by the user will be mint into $GLP; the other 50% will be mortgaged into AAVE, lent cryptocurrencies such as $ETH or $BTC, and then sold as stable coins, thereby hedging the risk assets in the portfolio The impact of market volatility. The strategy is expected to be released in Q1 of 2023.

at Yield Yak$GLP Mining Projectborrow money

borrow money

Vesta Finance is an overlending protocol built on Arbitrum. Currently the platform has$GMX Vault and $GLP Vault, users can mortgage $GMX or $GLP to lend the platform stablecoin $VST.

Insurance/Cover

Holders of $GMX can buy it on Nexus MutualCover, that is, when contract failures, economic attacks (including oracle machine failures, etc.), and governance attacks occur, users can obtain corresponding compensation on the platform.

What are the current challenges facing decentralized derivatives exchanges?

Liquidity is poor compared to centralized exchanges

CEX usually provides market maker services on the platform. As a counterparty, it provides more liquidity for users to buy and sell cryptocurrency transactions. It does not only rely on the users own transaction needs, so it has higher liquidity. However, many DEX products are limited by the size of LPs and traders, and the size of the liquidity pool is small, which will also bring high slippage and impermanent losses to participants.

higher transaction costs

Users only need to pay extremely low transaction fees to CEX, such asBitMEXThe commission for taking orders is 0.075%, and the commission for placing orders even reaches negative -0.010%, which means that users can get rebates from the platform. However, DEX often has high transaction costs, and due to its decentralized nature, it also needs to bear additional on-chain transaction processing costs, but this part of the cost can be very low in Layer 2 such as Arbitrum.

Product use experience and high barriers to getting started

CEX often has a better user experience, which is similar to the operation of traditional investors in stock trading, so users can get started quickly. However, due to product innovation in DEX, users need to learn new trading rules and trading steps, which undoubtedly increases the learning cost and entry barrier for users.

Insufficient product richness

At present, the decentralized derivatives exchange track is still in the early stage of development, and the product functions are mainly perpetual contracts and spot transactions; and after years of development in CEX, the current derivatives product functions are more diversified. Such as currency-based contracts, grid strategies, etc., can meet rich user needs. At the same time, the number of trading pairs of DEX is far less than that of CEX. For example, Binance can support hundreds of trading pairs, while dYdX and GMX only support 38 and 8 trading pairs respectively.

Head project research and data analysis

In this section, we will mainly introduce four leading projects in the decentralized derivatives trading track, GMX, dYdX, Perpetual Protocol and Drift. First of all, we will introduce the basic situation of the project at this stage, hoping to give readers a brief understanding of the project. Next, we will conduct an in-depth analysis from the perspective of project mechanism, fee structure and distribution, token economy and security, and compare projects, so that readers can form a more comprehensive understanding of the current decentralized perpetual contract trading track. Know.

A Quick Look at These Four Projects

GMX

GMXis a decentralized derivatives trading protocol created by an anonymous team. GMX on September 1, 2021 atArbitrumLaunched on , and will go live on January 5, 2022Avalanche. GMX currently supports spot trading and perpetual contract trading with a leverage of up to 50 times. The orders supported by GMX include market orders, limit orders, and trigger orders (take profit/stop loss orders).

The core mechanism of GMX is the GLP liquidity pool. The GLP pool consists of a basket of assets that acts as the traders counterparty in the transaction and provides liquidity for all transactions on the platform. GMX uses a dynamic pricing mechanism toChainlinkThe provided dynamic aggregation oracle feeds the price, so that the transaction can be executed with zero slippage.

GMX contains two native tokens. in,$GMXIt is the utility and governance token of GMX. Holders of $GMX tokens can obtain GMX governance voting rights or choose to pledge tokens to obtain rewards. $GLP is GMXs liquidity provider token. Holders of $GLP, that is, liquidity providers can obtain a certain percentage of platform transaction fees as rewards for providing liquidity.

dYdX

dYdXEthereumEthereumDecentralized derivatives trading protocol on the network, powered byAntoni JulianoCreated in August 2017. The core team of dYdX consists ofCoinbaseIt is composed of software engineers from well-known cryptocurrency companies.

dYdX executes trades using the order book model familiar to traditional market makers, providing traders with a wide variety of order products and liquidity. Currently, dYdXs trading products are mainly perpetual contracts, which support perpetual contract transactions with up to 20 times leverage and custom slippage.

In addition to the well-known order book trading mechanism, another feature of dYdX is that it utilizesLayer 2 Solution Starkwares transaction engine to increase transaction throughput and reduce transaction fees. But the order book mechanism and reliance on external trading engines somewhat increases the centralization of dYdX. in the nextv 4 In the development plan, dYdX plans to transition from Starkware to its own development based onCosmosdYdX Chain, its native blockchain, to build a fully decentralized derivatives exchange.

$DYDX is the native governance token of dYdX. In addition to voting rights for governance, token holders also receive transaction fee discounts based on the size of their holdings. Additionally, holders can stake $DYDX to secure pools to earn rewards.

Perpetual Protocol

Perpetual ProtocolandYenwen FengandShao-Kang LeeCo-founded decentralized derivatives trading protocol. Perpetual Protocol originally published in December 2020 atGnosis Chain(formerly xDai). Its v2 version,Curie, launching on Arbitrum in November 2021.

Perpetual Protocols trading products are mainly perpetual contracts. Currently, the orders supported by Perpetual Protocol include market orders, limit orders and stop loss orders. It supports perpetual contract transactions with up to 10 times leverage and custom slippage.

Perpetual Protocol uses a virtual AMM (vAMM) transaction model. Although vAMM also uses the constant function equation of AMM, unlike the traditional AMM model, vAMM is only used as a price discovery tool, there is no real liquidity, and there is no counterparty in the transaction. However, vAMM v 1 has issues with long-short skew in open interest and high slippage. To solve the problem of high slippage, Perpetual Protocol launched the v2 version, usingUniswap v3Provides centralized liquidity as an execution layer to reduce transaction slippage. In addition, v2 adds a cross-margin mechanism and enriches the types of collateral, while allowing users to create markets without permission.

$PERP is the native utility token of the Perpetual Protocol. The primary function of $PERP is governance. Token holders can participate in governance voting or stake tokens to earn rewards.

Drift

Drift ProtocolandDavid LuandCindy LeowCo-founded decentralized derivatives trading protocol. The core contributing team behind Drift is Drift Labs.

Drift v 1 in November 2021 atSolanalaunched on Currently, Drift v2 has been launched on its internal mainnet and is planned to be officially launched in the near future. At this stage, Drift supports spot trading, perpetual contract trading with up to 10 times leverage, lending, and passive liquidity supply. The order types supported by Drift include market orders, limit orders, and advanced conditional orders (such as stop-limit orders, etc.).

Drift v 1 is similar to the Perpetual Protocol mentioned in this article, using vAMM as its core mechanism. But the biggest difference is that the liquidity of its vAMM is dynamically variable, which can provide deeper liquidity around the price to solve the slippage problem. At the same time, Drift v 1 is integrated with the order book, allowing users to submit limit orders against vAMM. Drift v2 is an upgraded version of v1. Compared with v1, v2 increasesInstant (JIT, Just-In-Time) Liquidity Auctionmechanism andPassive Liquidity Pool, to encourage market makers to provide more sufficient liquidity for transactions. For detailed mechanism description, please move to the project mechanism section below to read.

Currently, Drift Protocol has not issued its own native token.

Project Mechanism

One of the core problems to be solved in derivatives trading is liquidity. In terms of this core mechanism, dYdX, GMX, Perpetual Protocol and Drift have implemented it in several completely different ways.

The traditional model of dYdX attracts market makers to provide liquidity, but the degree of decentralization is lower than that of GMX.

image description

dYdX trading interface, source: dYdX official website

The implementation of dYdX’s on-chain order book relies on its construction on Layer 2. The order book is different from AMM. It lowers the barriers for users and market makers to participate in transactions, and at the same time can provide liquidity continuously for a long time. It is also an established model familiar to traditional market makers. dYdXs trading and matching engine throughAmazon Web Services(AWS) hosting, it is worth noting that dYdX is not strictly a fully decentralized derivatives exchange, its order book and trade matching engine are still centralized. But dYdX is actively developing v4, which is expected to go live in Q2 2023, which will feature a fully decentralized order book and matching engine and achieve extremely high order book throughput.

Instead of adopting dYdXs order book model, GMX innovated aGLPmechanism. The GLP liquidity pool provides liquidity for transactions and consists of a variety of assets, includingwBTC、 wETHstable currencystable currencywait. Under this mechanism, the platform divides users into two categories, namely traders and liquidity providers.

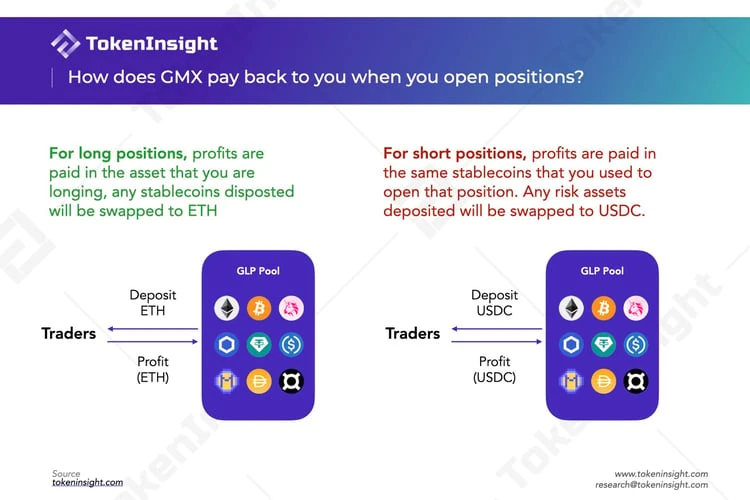

For traders, if they want to do leveraged trading, they need to deposit collateral in the GLP pool first. According to the rules of the exchange, the collateral for opening short and opening long is different.

For example, when a trader is long ETH, it can be described as borrowing ETH from the GLP pool; and when a trader is short ETH, borrowing the stable currency corresponding to ETH from the GLP pool, This corresponds to two different collaterals, but the assets in the pool are not actually lent. When closing a long position, if the trader makes a profit, the long asset (ETH in this case) will be withdrawn from the pool as a profit to the trader, and if the loss is lost, the initially deposited asset will be deducted and put into the GLP pool , that is, the currency of the profit and loss is the same as the currency of the collateral. Therefore, the GLP pool is equivalent to the counterparty of the trader.

For liquidity providers, $GLP can be minted/destroyed by injecting/withdrawing a specific asset into the GLP pool, and a certain fee will be charged for both minting and destroying. Each asset in the pool has a corresponding target weight, which is adjusted according to market conditions. If the current weight of an asset is higher than the target weight, a higher fee will be charged when depositing the asset, and as an incentive, the fee for withdrawing the asset will be reduced, and vice versa.

The price of the GLP pool is provided by Chainlinks oracle, and its price is based on some centralized exchanges such as Binance andBitfinex. This enables GLP to have extremely high capital efficiency and achieve zero slippage in transactions (the oracle machine feeds prices to provide the optimal transaction execution price), and at the same time, liquidity providers do not face impermanent losses because they do not need to discover prices.

Perpetual and Drift iterate based on AMM, but the effect has not yet met expectations

The AMM mechanism proposed by Uniswap uses the constant function of x*y=k to realize the exchange of certificates, but this mechanism is not suitable for derivatives transactions, and there are also problems such as high slippage and impermanent losses. In order to solve the limitations of AMM, Perpetual Protocol proposesVirtual AMM(virtual AMM). While implemented using the same formula, there is no actual storage pool of assets (k). Tokens will eventually be stored in vaults via clearinghouses, and vAMMs are only used for price discovery. Since liquidity is not provided by liquidity providers but by traders themselves, there is no impermanent loss. In addition, the value of k is manually set by the operator according to the market situation, which realizes slippage management to a certain extent.

However, vAMM v 1 is not suitable for highly volatile markets, relying on insurance premiums when open interest is heavily skewed, while traders still face high slippage. In order to solve these problems, vAMM v2 is combined with Uniswap v3 as the execution layer, and a liquidity provider is introduced, so that each transaction occurs directly between traders and market makers through the liquidity pool, reducing insurance premiums and tilting the market Participation makes the protocol more secure. For slippage, Uniswap v3 allows liquidity providers to provide liquidity within a custom range, and each position is then pooled into the pool, so that large transactions will be spread across multiple positions, thereby achieving the goal of reducing slippage Effect. But the new problem is that liquidity providers have no losses only in the initial stage (the price has not deviated), which is very unfriendly to them, making vAMM v2 unattractive to LPs. At present, the Perpetual Protocol team is providing liquidity for the market to guide depth and activity.

Drift also initially focused on the vAMM model - the same as Perpetual. Based on the Perpetual Protocol v 1 model, Drift introduces a dynamic k value and realizesDynamic AMM(Dymatic AMM). In this way, liquidity rebalances and provides deeper liquidity at the current price, and the depth of liquidity will not get out of control as the price moves further and further away from the initial price level of the perpetual contract, ensuring liquidity under any market conditions Sex is strong. At the same time, Drift is also integrated with the order book, allowing users to submit limit orders.

But is the problem with static k completely solved?

not at all. Although the position on Drift can be closed directly without reaching the final price, its funding rate has seriously deviated from the funding rate of the perpetual contract on CEX, because the problem of market inclination has not been really resolved. For example, whenLUNAWhen prices plummet, Drift requires a large number of short positions to keep prices accurate, meaning longs pay extremely high funding rates to do so. Overall, the vAMM model makes it difficult for such DEXs to reflect real market prices. This failure led Drift to decide to discontinue the v1 and focus on the second generation.

Drift v2 adds two liquidity mechanisms based on the original decentralized order book - instant liquidity auction and AMM liquidity. When a trader submits a market order, an auction is generated for that order pitting market makers against each other to achieve a better price to satisfy customers. If the market maker does not step in within the first 5 seconds, the customer will be satisfied through the DAMM. This has improved pricing and liquidity depth, enabling orders to be filled with minimal slippage, and at the same time reducing the risk of AMM long/short imbalance, but the specific effect remains to be tested by the market.

Overall, from a mechanism point of view, although the order book model has brought dYdX a high trading volume, the degree of decentralization is far lower than that of GMX, Perpetual and Drift. It is not difficult to find through analysis that the vAMM model has certain disadvantages and is not suitable for the current market for the time being. Perpetual and Drift need to further explore this model.

Fee Structure and Allocation

Due to the order book approach, dYdX usesMaker-TakerPrice model to determine transaction fees. Makers are charged 0-2bps, while Takers are charged 2-5 bps, based on transaction volume over the past 30 days. It is worth noting that no transaction fee will be charged when the transaction volume in the past 30 days is less than 100,000 US dollars. This is to encourage retail investors to participate in transactions, and fees will only be charged for orders that have been satisfied. In addition, depending on the amount of $DYDX and $stkDYDX tokens held by the user, there is also a discount of up to 50% on transaction fees. Unlike other agreements, all fees charged go to thedYdX Foundation, and will not be distributed to token holders.

Compared with dYdX, GMX has more sources of transaction fees. There are two main parts: one is the fees incurred when minting/destroying $GLP and swaps. As mentioned above, 0-80 bps fees are charged according to the current weight ; The other part comes from margin trading, and the transaction fee is 0.1% of the total position. At the same time, in margin trading, a borrowing fee will be charged to the GLP pool. The calculation formula is (Assets Borrowed) / (Total Assets in GLP) * 0.01%, and it will be charged every hour. 70% of the fees collected by the platform will be distributed to holders of $GLP, and the remaining 30% will be distributed to pledgers of $GMX.

As a result of the upgrade to the model, the charging mechanism for Perpetual and Drift has also changed. A transaction fee of 0.1% is charged on every transaction on Perpetual Protocol v2. Compared with v1, v2 has broadened the fee channels: v1 fee income only comes from the public market, and v2 also includes private market and remortgage on this basis (funds in insurance funds can be used for low-risk agreements to increase returns). There are two situations for fee allocation. When the insurance balance is less than the insurance threshold, 20% of the fee will be deposited into the insurance, and 80% will be allocated to the liquidity provider (market maker); if the insurance balance is greater than the insurance threshold , the cost of inflowing insurance funds will be evenly distributed between DAO Treasury and $vePREP holders.

Because part of Drifts liquidity comes from the order book, itsfee structureMore similar to dYdX, also based on past 30-day trading volume. Takers are charged 5-10 bps, and its worth noting that Makers are charged a flat -2bps - a big difference from dYdX. Additionally, the DAMM charges 90% The transaction fee will be allocated according to the liquidity ratio provided by the liquidity provider.

All in all, the fee structure of dYdX and Drift is similar to a large extent, but the overall cost of Drift will be slightly higher than that of dYdX. Compared with these two DEXs, GMX and Perpetual have richer sources of fees. In addition, dYdX does not distribute revenue to token holders or liquidity providers. Even though token holders can enjoy transaction discounts, from this perspective, it will be slightly inferior to the other three protocols in terms of user incentives.

Token economy

In addition to Drift, GMX, dYdX, and Perpetual all have their own governance tokens, and can also be rewarded by staking tokens. There are differences in the specific reward distribution:

100% of GMX revenue is distributed to $GMX and $GLP holders. Total reward for $GMX holders is 30% transaction fees (in ETH or AVAX) plus staking earned$esGMXToken andmultiplier points. $esGMX can also be pledged again like $GMX to get the same benefits, or exchanged for ordinary $GMX tokens after a one-year lock-up period. At the same time, $GMX/$esGMX stakers can also get 100% APR multiplier points per second, which can also be staked again to motivate holders to keep staked $GMX, and once the user cancels the stake of $GMX, the corresponding proportion will be destroyed multiplier points. Similarly, $GLP holders also earn a total of 70% of the transaction fee (in the form of ETH or AVAX) plus the $GMX earned by staking. It is worth noting that the $GLP currency price is positively correlated with the asset price in the GLP pool, and liquidity providers indirectly enjoy the potential appreciation of the assets in the pool.

Similar to GMX, holders of $DYDX on dYdX can stake tokens tosecurity poolto mint $stkDYDX. $stkDYDX enjoys the same proposal and voting rights as $DYDX in governance. The security module is mainly used to incentivize holders to properly govern the agreement, and at the same time act as a risk manager in the system. As an incentive reward, 2.5% of the initial supply of $DYDX will be allocated to users who pledge $DYDX, and the standard is based on the fees generated by user transactions and the proportion of open contracts. In addition, 7.5% and 25% of the initial tokens will also be used for liquidity provider rewards and trading rewards to motivate them to participate in trading activities on dYdX.

$PREP tokens are also available for governance and staking on the Perpetual Protocol. Holders of $PREP can lock it in the staking pool for a fixed period of time to obtain $vePREP. The risk is that if the insurance fund is exhausted in extreme market conditions, the pledged tokens will be sold through the agreement; and as compensation, the pledger can receive weekly rewards (fee distribution).

safety

safety

As mentioned above, users need to deposit the corresponding collateral before trading on GMX. GMX uses thepartial liquidation, the liquidation price is the price at which the value of the collateral less losses and borrowing fees is less than 1% of the position size. If the token price changes beyond this point a liquidation is triggered and the position will be automatically closed. Since traders can choose up to 50 times leverage, the higher the leverage, the higher the liquidation price. With the increase of borrowing costs, the liquidation price will gradually increase, requiring users to continue to pay attention to the liquidation price to avoid liquidation.

In addition to the liquidation mechanism, GMX has also taken corresponding security measures against platform attackers. Originated from September 2022aggressive behavior: The attacker first opened a contract on GMX, then manipulated the price of AVAX on FTX, and finally benefited by closing the position on GMX. The attack caused the liquidity provider to lose about $570,000. In response to this incident, GMX protected the exchange from further manipulation by capping short and long positions on AVAX/USD, making the cost of manipulation higher than the potential gain. In addition, GMX launched in OctoberBug bounty program, rewards are distributed based on the severity and impact of vulnerabilities to prevent smart contracts and applications from fund theft, price manipulation, and theft of governance funds.

Unlike GMX, dYdX decides whether to liquidate based on account value and margin requirements: when the total value of the account is less than the maintenance margin requirement, different formulas will be used for liquidation depending on the position. The profits and losses caused by the liquidation will enter the insurance fund, and if the insurance fund is exhausted, the deleveraging mechanism will be used as the last protection method: offset the underwater account by reducing the position of the high-profit and high-leverage account, thereby maintaining the stability of the system sex.

The liquidation mechanism of Perpetual is similar to that of dYdX. During liquidation, the margin ratio will be obtained by dividing the collateral value by the notional value of the position. Only when the ratio is greater than 6.25% to avoid liquidation. If liquidation is triggered, the maximum liquidation ratio varies depending on the margin ratio: when the margin ratio is between 6.25% and 3.125%, 50% of the traders position will be liquidated; and when the margin ratio is less than 3.125%, 100% of the traders position will be liquidated % of the position.

In addition, Perpetuals insurance funds are also used to protect the perpetual contract market. When the perpetual market is heavily tilted, the insurance funds will be used to pay high funding rates. If the insurance fund is exhausted, the smart contract will be triggered to protect the solvency of the system by minting new $PREP tokens and selling them as collateral in the vault.

Drift also calculates the margin ratio, and liquidation will be triggered when the account maintenance margin ratio is less than the minimum maintenance margin ratio. In addition, on Drift, it will be calculated by the formula of log(max( 0, margin ratio - maintenance ratio) + 1)Health. The user can judge the distance between the account and the liquidation through the Health value on the interface. When the Health is 0, the account will trigger liquidation, and the position will be liquidated at the price of the margin engine.

On the whole, dYdX, Perpetual, and Drift all use margin to judge whether to liquidate. In addition to liquidation, GMX and Perpetual also have related security measures against attacks and market conditions. Although dYdX also has similar security modules to deal with protocol bankruptcy or other issues, it has been voted by the community to be closed after November 28, 2022.no longer valid。

data performance

In this section, we compare the market performance of several decentralized exchanges over the past period of time, including indicators such as market trading volume, open interest, platform revenue, and active users, in order to analyze similar development trends, and Which exchanges have higher market recognition.

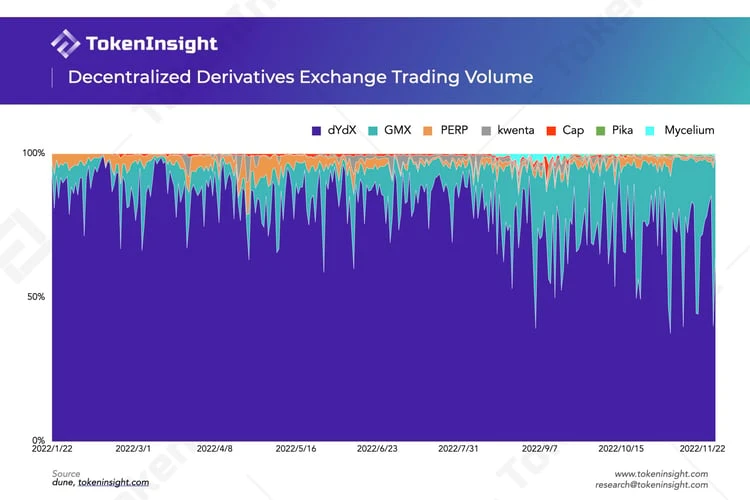

Decentralized Derivatives Exchange Trading Volume

From the perspective of trading volume, dYdX has an absolute advantage over other decentralized derivatives exchanges, continuing to control over 70% of the market as a whole. Especially since GMX has not been widely known since the beginning of the year. dYdX’s high trading volume is inseparable from its order book and having designated market makers to provide liquidity. Users can use trading strategies similar to centralized exchanges, and with low transaction costs, the blessing of API transactions can also support more frequent transactions.

As a rising star, GMXs innovative mechanism, considerable real returns (ETH rewards) and the expansion of Layer 2s own user base have all promoted the development of GMX. Since the third quarter of this year, GMXs market share has increased significantly, and in some time periods it can even gain more than half of the market share.

The remaining agreements only account for a small part of the total transaction volume, and their competitiveness is weak at this stage.

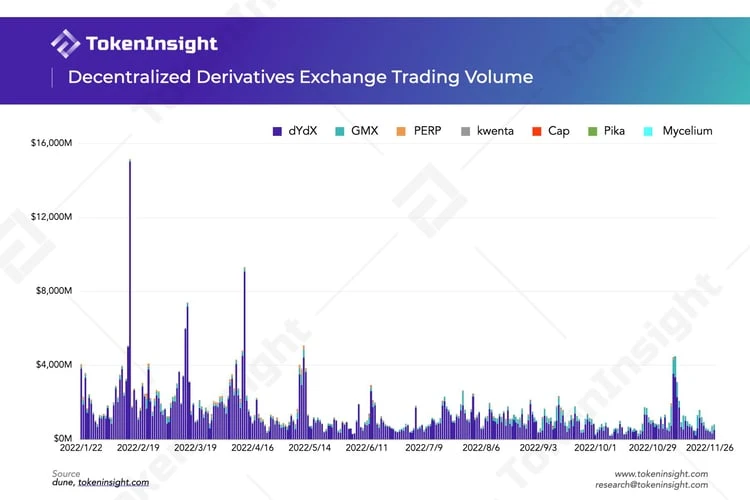

In 2022, the trading volume of various exchanges will basically remain the same. In the past 10 months or so, the total trading volume of decentralized derivatives exchanges reached $478 B. dYdX has been in a dominant position in the early stage, with a single-day trading volume even exceeding $15 B. Since Q2, affected by the bear market and events such as Terra, the overall trading volume has declined. early novemberFTX thunder eventThe occurrence of , led to a large number of traders withdrawing from centralized exchanges and turning to decentralized protocols. As a result, the trading volume had a small peak during this period, and then fell back to a lower level.

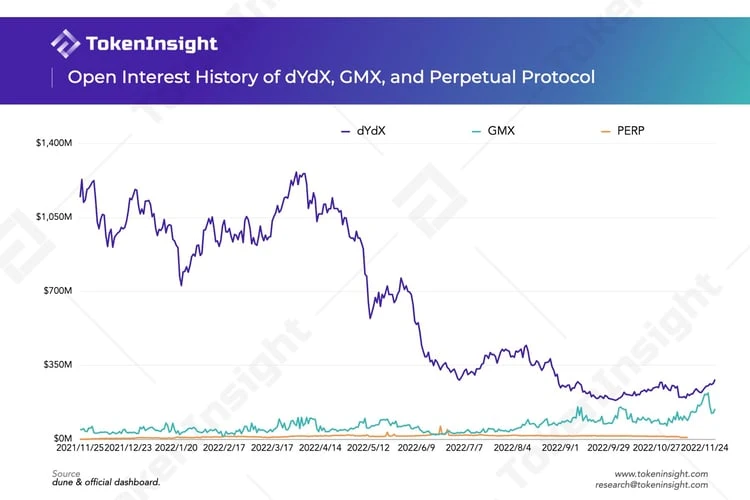

Historical open interest volume

Before Q3 in 2022,dYdXThe open interest (OI) far exceeded the other two exchanges, and then fell all the way to a minimum of about 190 million US dollars, only about 15% of the peak. Of course, this is not the reason of dYdX itself, but the influence of the market environment. Since the beginning of this year, because the market as a whole is in a bear market and mixed with various thunderstorms, the high leverage and the expansion of market credit in last years bull market have been gradually forced to rupture this year. This process is obviously cruel and bloody, so we can see that dYdX, a trading agreement that has attracted a large number of users since last year, is the same as a centralized exchange, and its open interest has also plummeted.

On the other handGMX, the exchanges OI has been growing steadily, and even once had a tendency to surpass dYdX. One of the core catalysts was of course that many users began to move to decentralized exchange protocols. The increase in the scale of GLP assets in GMX also enables its platform to support greater liquidity and provide users with more exposure. And more user influx and transaction behavior will attract more users to GMX to provide liquidity to earn income. In contrast, PREP is mediocre and relatively weak in competitiveness.

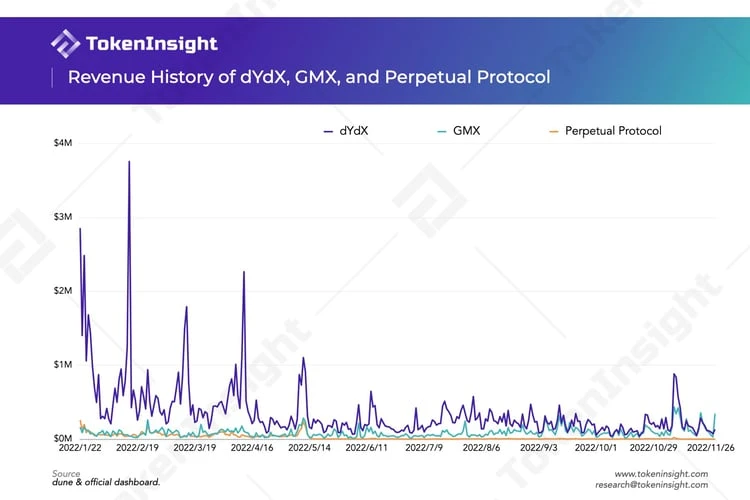

Historical revenue of dYdX, GMX and Perpetual Protocol platforms

Similar to market trading volume, dYdX’s platform revenue in the first half of this year also far exceeded that of the other two decentralized exchanges. Analyzing the reasons, on the one hand, the trading volume of the dYdX platform is much higher than these two exchanges. Even though the transaction fees are lower and there are certain discounts, the overwhelming advantage in terms of trading volume still brings considerable income to dYdX.

On the other hand, as mentioned above, dYdX does not distribute fee income to token holders, and all income belongs to the dYdX Foundation. Other exchanges will allocate all or part of the fees to token holders or liquidity providers, resulting in a large income gap. As time goes by, this gap is gradually narrowing, and it was even overtaken by GMX for a few days in November this year, and GMXs revenue is expected to continue to grow.

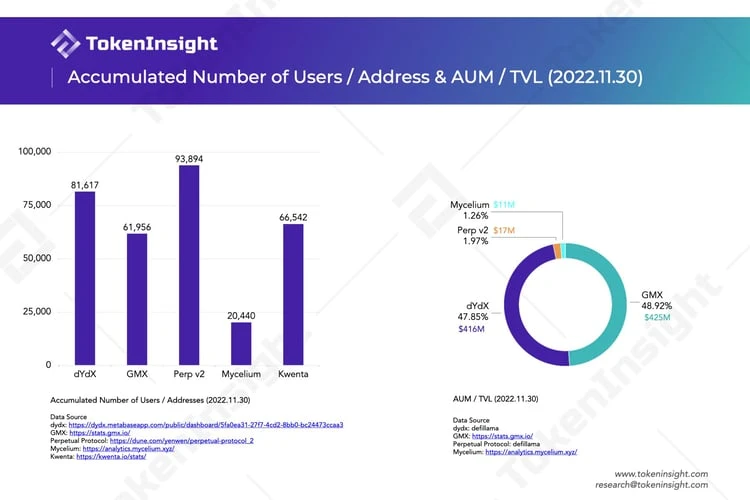

Comparison of cumulative user volume and total lock-up value

Comparing the accumulated users of each exchange on November 30, 2022, it can be seen that Perp v2 has the highest number of users, reaching 93,894. This data comes from the founder of PerpDune Dashboard by Yenwen. The highest user volume and low transaction volume and TVL are somewhat anomalous.

Apart from Perp v2, among other protocols, dYdX has the largest cumulative user base. Mycelium is currently at the lower end of the spectrum in terms of users after rebranding from Tracer DAO. In terms of TVL, GMX has the highest GLP asset scale and has slightly surpassed dYdX. But the two agreements basically each occupy half of the market share.

Token situation

The above table summarizes the Token performance of some decentralized derivatives trading protocols.

In terms of circulating market capitalization, $GMX is the highest followed by $DYDX. It is worth noting that the market capitalization of $GMX is even twice that of $DYDX. and$KWENTAThe market value of $KWENTA is also as high as $37 M, but $KWENTA has just been released, and the current circulation is only the initial issuance and a small amount of release in the first few weeks. As a new Token, $KWENTA has the smallest number of holders, less than two hundred.

In terms of fully diluted market cap (price * total tokens), $DYDX is the highest, mainly because there is a large amount of $DYDX that has not yet been unlocked. The initial allocation of $DYDX to the team, investors, employees, etc. will start to be unlocked in February next year, and the circulation of $DYDX will increase significantly by then. TokenInsight has been updated$DYDXs unlocking plan, click the link to view it.

Future direction

This section aims to make a simple comparison of the development paths of various exchanges based on their roadmaps and related disclosure documents. Through this comparison, we hope to provide readers with a further understanding of the future development trend of the decentralized derivatives exchange.

according to

according toGMX DAO In the discussion on the 2022 annual development plan in the forum, GMX will continue to develop the platform mainly in three dimensions: improving platform security and ease of use, developing the synthetic asset market, X4 and new chain deployment.

Starting from the level of development priority, although the team said that the deployment of the new chain itself will only take more than a month, specific issues such as liquidity and on-chain monitoring are the real problems facing the new chain. At the same time, the team is also worried about fully developing the new Chaining would cause GMX to be left behind by competitors who are constantly improving their products. Therefore, the development of a synthetic asset trading market with relatively low difficulty will be prioritized over X 4 and the launch of the new chain. This decision also means that striving for more market share is still the top development goal of GMX at present.

X 4 aims to attract more derivatives traders by providing a more flexible trading mechanism. This version will launch a custom AMM that gives pool creators great freedom, and creators can set and change transaction fees arbitrarily to adjust liquidity and buy and sell transactions. At the same time, the X4 will also launchPvP AMMLet traders one-to-one match long or short, and allow LP to participate, which means that the white list no longer exists, and various assets can participate in the transaction. In theory, this trading model supports unlimited trading liquidity.

In addition, according to the GMX teams speech in the forum in May this year, the deployment of PvP AMM and X 4 originally required about three months of development time, and the current development progress of the project is obviously behind expectations.

Deploy a new chain to realize the concept of complete decentralization

The dYdX team is currently concentrating on developing the v4 version, and recently completed the second phase of v4, namelyDeployment of internal testnet. According to the news at the beginning of this year, dYdXs v4 was originally scheduled to land at the end of 2022, and in the latest development progress disclosed, after completing the third phase of advanced function development, the fourth phase of the public test network launch and the fifth phase of the main The complete dYdX v 4 will be deployed in 2023 Q2 after the network launch.

Focusing on the construction of DAO and the improvement of platform performance, dYdX aims to realize the construction through v4Fully decentralized trading platformidea. The current v3 version still relies on a centralized system for the order book and matching engine, while the v4 version will launch a fully decentralized off-chain order book and matching engine, hoping to achieve throughput that can scale several orders of magnitude. In addition, trading products such as spot trading that were canceled with the deprecation of the Ethereum Layer 1 version are expected to return to the trading platform with the v4 version.

In the v4 version, dYdX Trading Inc., the development team of the platform, will also hand over the operation rights to the community, and will no longer extract income from transaction fees. At present, the community plans to create an operations sub-DAO, Operations subDAO, to assist the platform to smoothly complete the transformation of the operating structure.

In addition, dYdX also plans to develop in the Cosmos ecosystemindependent blockchain, and extend its v4 version to the chain. The new chain will be built using the Cosmos SDK and the Tendermint Proof-of-Stake consensus protocol.

When asked by TokenInsight about the future competitive landscape of decentralized derivatives exchanges and whether there will be giants like Binance,Nathan Cha, head of marketing at dYdX told us:

“We believe that in the long run, there will be a situation in which the market share will be concentrated in the hands of a few players in the future. It’s like we have Uniswap, MakerDAO and AAVE in decentralized spot trading and lending. These are all exciting Respectable agreement. Therefore (for us) building an excellent DeFi tool, providing a good user experience, and returning the ownership of the agreement to the hands of users is the key issue. In this way, even if the market is concentrated, Its a small problem, too.

Derivatives Exchange Alliance

In terms of development plans, Perpetual Protocol and Drift Protocol did not show particularly clear development ambitions. Perpetual Protocol is currently focusing on increasing the types of collateral supported by the platform and completing the distribution of USDC fees. However, referring to the expected completion time on its roadmap, the project also has a slow development progress. Drift Protocol launched the v2 version not long ago, aiming to achieve more sufficient liquidity and improve the platform mortgage situation.

It is worth mentioning that Perpetual Protocol, Drift Protocol and GMX recently announced that they have cooperated with blockchain data analysis platform Nansenreached a cooperation, and jointly build a Dashboard that allows traders to monitor various data on the trading platform in real time. Through this cooperation, the derivatives exchange alliance hopes to revive the confidence of traders in the market winter brought about by the FTX incident, and at the same time re-emphasize the core concepts of the DeFi industry, namely transparency, immutability and decentralization, And called on other decentralized exchanges to join this cooperation.

When asked what needs to be solved first regarding the outbreak of decentralized derivatives,Burt Rock,Kwentas Marketing Director replied to TokenInsight:

“First, let’s realize how new a concept we’re dealing with when we talk about decentralized derivatives trading. Back in 2016-2017 we had some basic proof-of-concept synthetic assets, but The layer 2 scaling solution were using to build a fully decentralized perps AMM on ethereum is less than two years old. I think were already talking about performance, fees, and really trying to deliver a competitive product thats is very good, but were still talking about some fairly rudimentary stuff that will require a lot of development from all sides.

Having said that, I think we actually have a pretty good grasp of what needs to be addressed. First, we need a low-latency decentralized Fable Machine, and faster L2 execution. Some exchanges sacrifice decentralization or security for performance, but for a real DEX to shine, we need to get prices and submit orders within seconds, or even milliseconds, without detours.

From a user experience perspective, we also need to start simplifying the transaction experience without compromising security too much. If youve ever tried to trade perps with a hardware wallet, its a nightmare to sign every transaction. Ideally, users should only need to sign a transaction once per session, just like you only need to log in to CEX once, and then trade at will in the window.

summary

summary

It is not difficult to see that the biggest development shackles currently facing the decentralized derivatives trading platform is the problem of insufficient liquidity. The leading projects all chose some similar problem-solving ideas, such as improving user-friendliness by improving product experience and expanding product matrix, so as to reach a wider market audience and occupy more market share. GMX and dYdX even chose to build their own chains to further develop the platform ecology.

Having an independent blockchain seems to be a big trend in the development of decentralized derivatives exchanges. However, it is difficult to fully deploy a new chain, the development cycle is long, and the market is changing rapidly. As the GMX team said, the most important thing is to be recognized by more traders in the shortest time. The trust of traders is based on the transparency, non-tamperability and decentralization of transactions on the platform. The exchange alliance cooperation mentioned above can also prove the importance of the implementation of the core concept for market confidence. From this perspective, dYdX, which is committed to complete decentralization, seems to have a better answer.

Waves

In addition to the four leading projects mentioned above, there are also some rising stars in the decentralized derivatives trading track. This section will briefly introduce several derivatives trading agreements that include perpetual contract transactions, and try to explore the development potential of these new entrants, providing readers with a new perspective on this track.

Mycelium

MyceliumIt is a decentralized derivatives agreement, its predecessor is Tracer DAO. Currently deployed on the Arbitrum and Rinkeby networks. Mycelium mainly supports perpetual contract transactions, providing contract transactions with up to 50 times leverage.

Myceliums initial launch product isperpetual pool(Perpetual Pool). Its core mechanism is to use two fund pools (multi-pool and empty pool) and rebalancing rate to realize the perpetual contract trading function of never liquidate.

In the perpetual pool, opening a position means casting assets. Users can stake $USDC to mint 1 L-ETH/USD (long) or 1 S-ETH/USD (short) in a multi-pool or an empty pool. In contrast, closing a position means destroying assets. The asset price difference between minting and burning is equal to the users loss or gain. The ratio of long pools to empty pools reflects the users choice of future price direction changes. For example, when there are more assets in the multi-pool, it means that there are more people who are bullish, and more assets are opened (cast) in the multi-pool, and vice versa. The rebalance rate is similar to the funding rate in the Perpetual Protocol vAMM mechanism. It is used to balance the ratio of the two pools (pull the long-short ratio back to 1: 1). Generally speaking, the mechanism of the perpetual pool is actually similar to the vAMM mechanism of the Perpetual Protocol, which has a certain price discovery function, and at the same time, a rebalancing rate similar to the funding rate is added to balance the long-short ratio. The difference is that the perpetual pool has real liquidity.

After changing its name to Mycelium, M