Original source: Mint Ventures

Author: Colin Lee

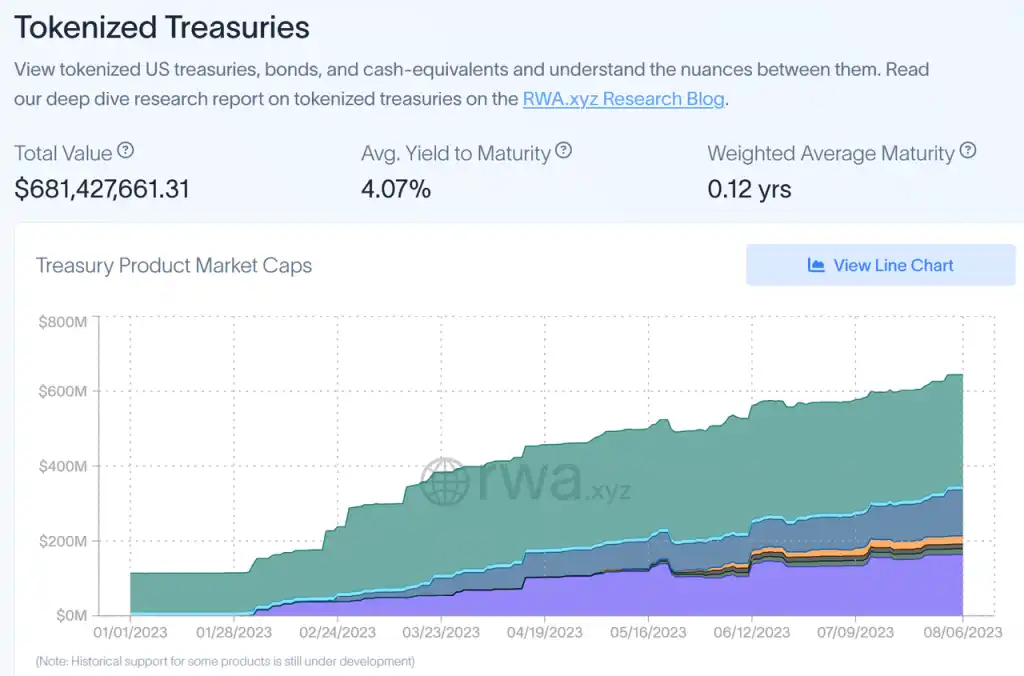

existPreviousIn the article, we mentioned that the subcategory of RWA that is most likely to explode in scale and user level in the short and medium term is government bond RWA. According to data from rwa.xyz, the current treasury bond-type RWA project (excluding U.S. bonds in MakerDAO) has tokenized treasury bond assets approaching US$700 million, which has increased by about 240% from the beginning of the year. In addition, the treasury bond RWA in MakerDAO has also grown rapidly to the level of billions of dollars. The overall growth rate of national debt RWA is relatively fast.

source:https://app.rwa.xyz/treasuries

Based on the above industry background, let us analyze the mainstream treasury bond RWA in the market.

Significance of Treasury RWA

In the previous How to define the native benchmark interest rate in the crypto world?andOutlook for the “Native Bond Market” in the Crypto World”, we discuss the crypto world’s native benchmark interest rates and possible bond markets. We can roughly think that the PoS yield of the public chain is the risk-free interest rate of the public chain, and a bond market may gradually develop around the interest rate.

But even if a crypto-native bond market similar to the scale of the current traditional bond market does not quickly develop on the chain in the future, the emergence of the “on-chain risk-free interest rate” LSD will still be of great significance to investors: using the public chain as a proxy Investors who use currency (such as ETH) as the bookkeeping standard can obtain currency-based low-risk returns even in a bear market. From this perspective, part of the investment strategies in the traditional market can be more smoothly migrated to the encryption-native industry: such as the stock-debt balance strategy.

Treasury bond RWA, like LSD, can allow U-based investors to use traditional allocation strategies once the risk-free interest rate of the traditional financial market can be introduced into the on-chain world. There are several benefits to this:

(1) U-based investors still have a relatively safe and stable place to earn interest after the market goes bearish. Taking the stablecoin market as an example, after the market began to gradually turn bearish in mid-2021, the overall stablecoin market dropped from US$188 billion to less than US$130 billion today. The reduction in the scale of stablecoins is also affecting the overall liquidity of the market;

(2) Stock-bond hybrid financial products are easier to launch and accepted by the market. In traditional markets, hybrid financial products are also familiar to most investors. This will also promote innovation in the field of DeFi asset management.

source:https://defillama.com/stablecoins

The most typical example at present is MakerDAO. After the market was bearish and U.S. bond yields increased significantly, MakerDAO included U.S. bonds in its investment scope. After entering 2023, MakerDAOs profitability improved significantly.

source:https://dune.com/SebVentures/maker—accounting_1

Therefore, there is reason to believe that other DeFi projects, after seeing MakerDAO’s “demonstration”, will also hope to improve project profitability through more diversified strategies such as RWA. Especially in a bear market, RWA can provide a stable and sufficient source of income for the stable operation of the project.

The business model of treasury bond RWA

At present, there are mainly 5 business models for national debt RWA, namely: consignment model, platform model, infrastructure model, self-operated model and hybrid model.

The consignment model neither directly participates in the packaging of underlying assets nor provides user KYC services. It mainly acquires customers through crypto-native methods, focusing on business marketing, acquisition of funds, and expansion of ecology and application scenarios. Representative projects are TProtocol and so on. This type of project is no different from the daily-used infrastructure such as Aave and Compound. It often obtains liquidity by establishing a fund pool, then pools users funds together, and then lends the funds to a single borrower. Buy underlying assets such as U.S. bonds.

Platform model, that is, the project party only provides a series of service solutions such as chaining, sales, and KYC, but does not personally encapsulate the assets. Representative projects are Desmo Labs et al. This type of project generally provides three types of services: (1) asset/equity tokenization services; (2) on-chain verifiable information services; (3) user KYC services, etc. This type of project can theoretically help encapsulate any type of assets/equities from the traditional market, not limited to treasury bonds RWA, and is commercially closer to the Internet platform model. If you want to stand out in this track, you need to consider the ease of use of the projects own one-stop solution, as well as the projects ability to acquire customers.

The infrastructure model, which provides services such as RWA on-chain, asset purchase, asset management, etc., but does not directly contact users who purchase treasury bonds at the C-end/B-end. Representative projects include Centrifuge, Monetalis Group, etc.

The self-operated model means that the project party finds the corresponding assets by itself, establishes a business structure with external partners, isolates the risks of assets, and tokenizes assets/equities. At present, there are many projects of this type of model, such as MakerDAO, Franklin OnChain US Government Money Fund, Frax Finance, etc. Compared with the first two models, this type of model has a higher level of off-chain business complexity and requires investment in legal affairs, the establishment of the companys business structure, and the selection of assets and partners. However, an important advantage of this type of project also comes from this: the underlying assets are relatively controllable, and the project party has the ability to actively manage risks.

Mixed mode can be a combination of the above four modes. This type of project can provide corresponding services such as on-chain, KYC and other services by itself. At the same time, it will also look for assets by itself and directly provide users with corresponding investment opportunities. A representative of this type of project is Fortunafi. Taking Fortunafi as an example, it provides 4 types of services: (1) Access Capital, which provides financiers with access to funds; (2) Earn Yield, which is packaged assets that users can invest directly after completing KYC; (3) Protocol Services, which provide governance, treasury management and other services to other protocols; (4) whitelabeled products, which provide RWA full-process on-chain services. Of course, the RWA services for this type of project are not limited to treasury bonds, but can also provide on-chain packaging services for other assets.

Of course, in addition to the above 5 models, there are purer trading infrastructures such as DEX serving RWA, such asDigiFTwait. However, this type of project does not participate in the screening, on-chain, sales and other links of the underlying assets, so I will not go into details here.

Asset side: underlying assets and asset-side architecture

underlying assets

The following types currently exist in the market:

(1) U.S. bond ETF. Projects using this type of underlying asset include Backed Finance, Swarm, MakerDAO, and ARKS Labs. The advantage of using this type of solution is simplicity: the management of the underlying assets is left to the issuer and manager of the ETF, including liquidity and bond rollover issues, without the project side of this type of project having to personally manage it. U.S. Bond ETFs have not yet experienced major risk problems, so for this type of project owners, there is no need to worry particularly about operational risks in asset management and other aspects. They only need to include the largest and most liquid assets on the market. Can.

(2) U.S. Treasury bonds. Projects using this type of underlying assets include OpenEden, TrueFi, Matrixdock, etc. This type of project often chooses shorter-term U.S. debt, and its liquidity is no different from cash. However, since the project directly seeks the client for cooperation, this type of project itself needs to bear the risks related to asset management, so it is very important to select the right partner.

(3) A combination of three types of assets: US Treasury Debt, US Government Agency Debt, and cash/Repurchase Agreements. Projects using this type of underlying assets include Franklin OnChain US Government Money Fund, Superstate Trust, TProtocol, Arca Labs, Maple Finance, etc. Similarly, this type of project will entrust the management of the underlying assets to professional managers. The continuation and liquidity issues of the underlying assets will be directly related to the project party. At the operational level, once the project party fails to select a manager of sufficient quality, problems may arise.

fee structure

The three underlying assets discussed above have different fee structures. Without considering the gas fees caused by on-chain transactions, the main rate structure is as follows:

Since the management of U.S. bond ETFs is handed over to ETF managers, the main cost issue comes from the casting and redemption links. The rates in this link are often around 0.05% -0.5%; the latter two involve the underlying assets. In terms of management, etc., management and transaction fees have been added. The cost of management fees is about 0.3% -0.5%. Transaction fees include bank transfer fees and other aspects, and the rate is also around 0.2%.

Asset business structure

Differences in underlying assets will also affect the entire business logic architecture. The following categories exist in the current market:

(1) Trust structure: Projects currently adopting this solution include MakerDAO, etc.

source:https://forum.makerdao.com/t/mip65-clydesdale-governance-framework-setup/16565

The trust operation mechanism is that the initiator transfers assets to the SPV to establish a trust relationship. The initiator obtains the trust income rights, and then transfers the trust beneficiary rights to ordinary investors. Taking MakerDAOs US debt RWA structure as an example, it includes various roles such as managers and auditors, but part of the off-chain business structure is built by Monetalis Group. The corresponding asset purchases, regular reports, and on-chain are all completed by Monetalis Group. In this architecture, MakerDAO uses governance to influence details such as scale and the purchase of underlying assets.

(2) Limited partnership SPV business structure: Currently, projects such as Maple Finance and Matrixdock adopt this type of business structure. The project will participate in the process of asset search and liquidity acquisition.

SPV stands for Special Purpose Vehicle - a special purpose vehicle. The main function of SPV is to raise funds from investors in the process of asset securitization/asset purchase. The original design purpose was to isolate bankruptcy risks. Strictly speaking, the first trust structure mentioned above can also be regarded as an SPV structure. Todays SPV development has become more mature. In addition to bankruptcy risk isolation, it also has several advantages:

· Simplify the financial management process and get rid of the problems in the traditional company business structure that the financial process involves too many departments and the business flow is unclear;

· Facilitate penetration management. In general, a single SPV corresponds to a single project/asset, which may avoid management problems. For example, in a commercial bank, it is difficult for investors to gain a penetrating understanding of the status of underlying assets because the bank will not disclose too many details. This type of information may only be disclosed at the management accounting level used within the bank. For personal housing loans, the characteristics of this type of loan will not be disclosed in the financial statements and annual reports disclosed to the outside world, let alone specific information about individual debtors. However, if a personal housing loan is packaged in an SPV, the loan information must be disclosed in more detail, such as the term, interest rate, collateral, loan amount, and sometimes the specific information of a single loan. In this case, the information that SPV can provide is much richer;

· Lower taxes. For certain underlying assets, SPVs have lower tax standards.

There are two layers in this business architecture:

The first level, users and SPV: What the user directly gets is the SPV’s creditor’s rights. The prerequisite for the user’s income to be guaranteed is that the SPV can perform the contract on time;

The second layer, SPV and commercial banks: SPV will participate in the national bond market, and will also participate in the inter-bank market for reverse repurchase and other operations. In this process, if the reverse repurchase between banks defaults, there may be greater risks than directly holding US treasury bonds.

In addition, in this architecture, users face an additional level of risk: SPV itself may have some risks.

ARKS Labs has expanded the above business architecture: nesting small SPVs in a large business architecture, which can achieve scalability of business scale and make it easy to operate when adding new underlying assets in the future. This is similar to the previous one in RWA talk: underlying assets, business structure and development pathThe structure of MakerDAO mentioned in is very similar.

Source: ARKS Labs

(3) Lending platform + SPV architecture: TProtocol currently adopts this type of business architecture. Compared with the second SPV business structure mentioned above, the difference is that in the second SPV business structure, one of the relevant parties of the SPV is the project party, and the project party will participate in the search and packaging of assets. In TProtocol, SPV is not related to TProtocol, but the initiator of RWA assets.

Take the following figure as an example, the initiator of SPV can be different institutions, and the subsequent on-chain service providers and asset brokers can also be different. TProtocol’s business organization is more flexible, but this is not without cost: as the number of partners increases, the SPV’s subsequent management and control, including the inspection and management capabilities of service providers, may also be reduced to a certain extent.

(4) On-chain fund share: Similar to the traditional fund purchase strategy, it is necessary to know the detailed buyer information and the one-to-one correspondence with the address. Franklin OnChain US Government Money Fund currently adopts such a business structure. This type of project is more like what was often called chain reform in the past, that is, the project party uploads off-chain assets and buyer information to the chain, and future transfer information will also be recorded in bookkeeping and then re-recorded on the blockchain. Record.

Although the RWA track is currently in its early stages, and users and capital scale do not have high requirements for business architecture, as the value of treasury bond RWA is gradually recognized by investors, the scalability of the architecture has become very important. Can it Encapsulating new assets in a timely manner and accessing more off-chain service providers may be the winner in the rapid development stage of the track.

Client side: KYC and other requirements

Due to the differences in the underlying assets and business architecture, the requirements of the project party for the user end also differ. Currently, there are 3 main differences:

(1) Initial investment threshold: Projects such as MakerDAO, ARKS Labs, and TProtocol do not set a user’s initial investment amount limit, but Maple Finance, TrueFi, Arca Labs, Backed Finance and other projects have set clear thresholds Minimum investment amount limit. No limit on the initial investment amount is more in line with the habits of current DeFi users. Some projects with an initial investment amount of more than 100,000 US dollars are mainly aimed at users with higher net worth.

(2) KYC requirements: According to the difficulty of KYC, it can be divided into 3 categories: no KYC projects, such as Flux Finance, ARKS Labs and TProtocol; lightweight KYC, such as Desmo Labs, which only requires uploading passport and other information; heavy KYC, such as OpenEden, Ondo Finance, Maple Finance, Matrixdock, etc. need to submit KYC information comparable to the traditional financial industry. High KYC threshold not only means threshold in the traditional financial industry, but also unacceptable to DeFi users at this stage.

(3) Other requirements: Some projects also limit their investors to certain regions, such as only serving non-U.S. users, or only serving non-U.S., non-Singapore, and non-Hong Kong users. This type of restriction is generally implemented by restricting IP addresses.

Some projects requirements for users, such as KYC and regional restrictions, are often checked through third-party KYC service providers. The project party does not directly participate in the KYC review process.

Revenue distribution strategy and composability

income distribution strategy

At present, there are two main income distribution strategies in the market:

The first strategy is the most common, that is, to distribute directly through the creditors rights relationship. Regardless of whether users hold SPV claims or obtain treasury bond ETFs, treasury bonds, etc. through other structures, end users can get most of the income generated by treasury bonds. Excluding the minting and burning, and the earnings earned by intermediaries, users can get a net income of about 4 percentage points.

This income distribution method is very similar to LSD: most of the pledged income is returned to the user, and only a part of the handling fee is deducted.

The second strategy currently only appears in the MakerDAO project, that is, through deposit interest rates. Since the users funds do not directly correspond to the underlying assets, MakerDAO uses a spread model similar to commercial banks: on the asset side, assets are invested in relatively high-yielding assets such as RWA; on the liability side, DSR is used to adjust the users income. Up to now, DSR has been adjusted 4 times, namely: (1) from 1% to 3.49%; (2) from 3.49% to 3.19%; (3) from 3.19% to 8%; (4) Decreased from 8% to 5%.

This strategy gives the project team more flexibility, but the disadvantages may also be obvious: users lack a clearer analysis framework for future profitability. It was originally a national bond RWA, and the user directly understood that it should have obtained a return level similar to the national bond yield. However, through monetary policy, such as MakerDAO’s recent excess returns to depositors, it has soared to 8%. Later, if depositors increase enough If there is a large amount, the yield will fall to the vicinity of the U.S. bond yield. This kind of fluctuation is not friendly to investors who want a stable yield level.

For the yield of government bond RWA, clear and clear predictability is very important, so the first income distribution strategy may be better than the second strategy. However, once the project adopting the second strategy clearly anchors the yield of government bonds, there is no difference between the two from the perspective of yield.

composability

Due to KYC requirements, the tokens of national debt RWA have also differentiated in terms of composability:

Some projects with strict KYC qualifications, such as Ondo Finance, Matrixdock, Franklin OnChain US Government Money Fund, etc., have whitelist restrictions on addresses, so even if there is a corresponding token transaction pool on the chain, it is impossible to do without access Let users trade as they please. For this type of project, unless the scale of the underlying assets is large enough, it will be difficult to obtain the support of many DeFi projects and obtain richer composability.

Projects that do not require KYC currently have no difficulty in composability. The only thing that limits the composability of this type of project is the business resources of the project itself, BD capabilities, and the scale of the project itself.

Summarize

By sorting out the above national debt RWA projects, we can vaguely see the business models that such projects may win in the short to medium term:

Underlying assets: Using treasury bond ETFs may be a relatively clever way to leave issues such as liquidity management to giants in the traditional financial field. If it is to directly purchase U.S. bonds or mixed assets, it will test the project partys ability to select partners;

Business structure: There are already relatively mature models that can be applied. It is best to have strong scalability to facilitate faster scale expansion and the inclusion of new asset categories in the future;

User side: In the short to medium term, projects that do not require KYC and have no capital threshold requirements have a wider user base. In the future, if regulatory requirements require KYC, the lightweight KYC project may become a more mainstream solution;

Income distribution: In order to make treasury bond RWA investors’ expectations of yield more stable and secure, the best solution is for the yield rate provided by the project to users to be consistent with the treasury bond yield rate;

Composability: Before regulation imposes restrictions on access permissions to RWA assets on the chain, expanding the usage scenarios of users’ treasury bond RWA tokens as much as possible is an important factor for each project to gain greater business volume in the medium to long term.

In the medium and long-term competition, perhaps due to the deepening of regulatory intervention, some lightweight KYC projects may have greater opportunities.