Detailed explanation of EigenLayer, the leader in “re-pledge”: business logic and valuation deduction

Original author: Alex Xu

Original source:Mint Ventures

introduction

With the completion of the upgrade of Ethereum Shanghai, the business of many LSD projects has ushered in rapid growth, and the number of users and net worth of LSD assets have also increased significantly. On the other hand, with the approach of the Cancun upgrade at the end of the year and the opening of the OP stack, today is also a big year for Rollup, and various services around the Rollup module, such as DA layer, shared sequencer, RaaS service, etc. are also in the ascendant. EigenLayer, which proposes the Restaking concept based on LSD assets and aims to provide services for many Rollups and middleware (Middleware), has also continued to gain attention this year. Large-scale financing, the OTC price of its tokens has recently been rumored to have reached an astonishing $2 billion, comparable to the valuation level of public chain-level projects.

In this article, the author will sort out the business logic of EigenLayer, and conduct a trial calculation of the project valuation of EigenLayer, and try to answer the following questions:

What is the restaking service, who is the customer base, and what problem is it trying to solve?

What are the obstacles to the promotion of the Restaking model?

Is EigenLayers valuation of 500 million or even 2 billion US dollars expensive?

The content of the following article is the authors staged opinion as of the time of publication. It is more evaluated and interpreted from a business perspective, and the technical details of the project are less inked. There may be errors and prejudices in facts and opinions in this article, which are only for discussion, and we also look forward to corrections from other investment and research peers.

Business logic of EigenLayer

Before officially starting to sort out EigenLayers business, let me introduce a few high-frequency words that will appear below:

Middleware: Middleware refers to the service between the underlying service of the blockchain and the Dapp. In the Web3 field, typical middleware includes oracles, cross-chain bridges, indexers, DIDs, DA layers, etc.

LSD: Liquid Staking Derivatives, such as Lidos stETH

AVS: Actively Validated Services, a distributed node system that provides security and decentralization guarantees for projects, the most typical is the PoS system of the public chain

DA: Abbreviation for Data availability. Data availability mainly means that other projects (such as Rollups) can back up their transaction data on the DA layer to ensure that all historical transaction records can be accessed and restored from the DA layer when necessary in the future.

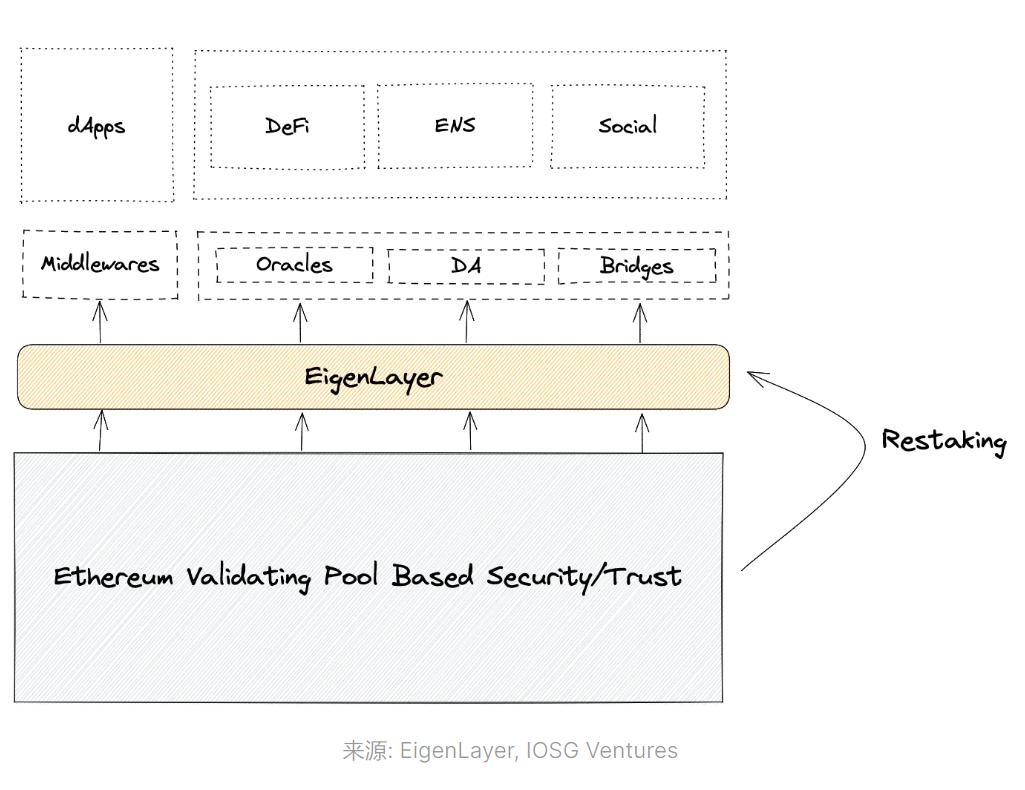

Business Scope

EigenLayer provides a rental market for cryptoeconomic security.

The so-called cryptoeconomic security (cryptoeconomic security) refers to the fact that in order to ensure the stable operation of the project, all kinds of Web3 projects have permissionless and decentralized attributes, and require the main service providers (verifiers) of the network to pledge tokens Participate in the project in a way, if the validator fails to perform the contract, the pledged tokens will be confiscated.

As a platform party, EigenLayer raises assets from LSD asset holders on the one hand, and on the other hand, uses the raised LSD assets as collateral to provide convenient and low-cost AVS middleware or side chains and Rollups. The AVS service itself provides demand matching services between LSD providers and AVS demanders, and a dedicated pledge service provider is responsible for specific pledge security services.

In addition, the parent company behind EigenLayer has also created a DA layer to provide data availability services for Rollup or application chains that need DA layer services. The product is called EigenDA, and EigenDA will generate business synergy with EigenLayer.

The pain points EigenLayer hopes to solve are:

1. For various project parties: reduce the high cost of independently building their own trust network, directly pay for the pledged assets + node operators on the EigenLayer platform, without self-build.

Source: EigenLayer White Paper

2. For Ethereum: Expand the usage scenarios of Ethereum LSD, make ETH a network security collateral for more projects, and increase the demand for ETH.

3. For LSD users: further improve the capital efficiency and income of LSD assets.

business user

The users of EigenLayer service involve three parties, and the corresponding requirements are:

1. LSD asset provider: The main demand of this type of user is to obtain the benefits of Ethereum LSD assets beyond the basic PoS rewards, and at the same time, they are willing to bear the possible confiscation of their own LSD assets as pledged assets to node operators risk.

2. Node operators: Obtain LSD assets through EigenLayer, provide node services for project parties that need AVS services, and extract income from node rewards and handling fees provided by project parties.

3. AVS demand side: Refers to those project parties who need AVS to provide security for themselves, but want to reduce costs (such as a Rollup or cross-chain bridge that uses LSD assets as the pledge of the node operator), they can pass EigenLayer To purchase this type of service, there is no need to build your own AVS.

The demand side of EigenDA is mainly various Rollups or application chains.

EigenLayer business details

Users can pledge the tokens pledged on the Ethereum network, including stETH, rETH, and cbETH tokens, to the EigenLayer market for a second time. The pledge service provider is responsible for matching the users tokens with the corresponding security network demanders and providing these project parties with AVS service, and the underlying assets of AVS are the tokens pledged by users on EigenLayer, and the project party needs to distribute a certain security fee to users.

Product progress

At present, EigenLayer has only launched the restake function of LSD, and has not yet developed node operation pledge and AVS services based on LSD assets. In the deposit activities of LSD assets that have been opened twice, the deposits quickly reached the limit (depositors are mainly seeking EigenLayer’s potential airdrop rewards). Users can also directly deposit 32 integer units of ETH to participate in Restake. In the case of limited deposits, EigenLayer has accumulated about 150,000 staking ETH at present.

Image source: https://app.eigenlayer.xyz/

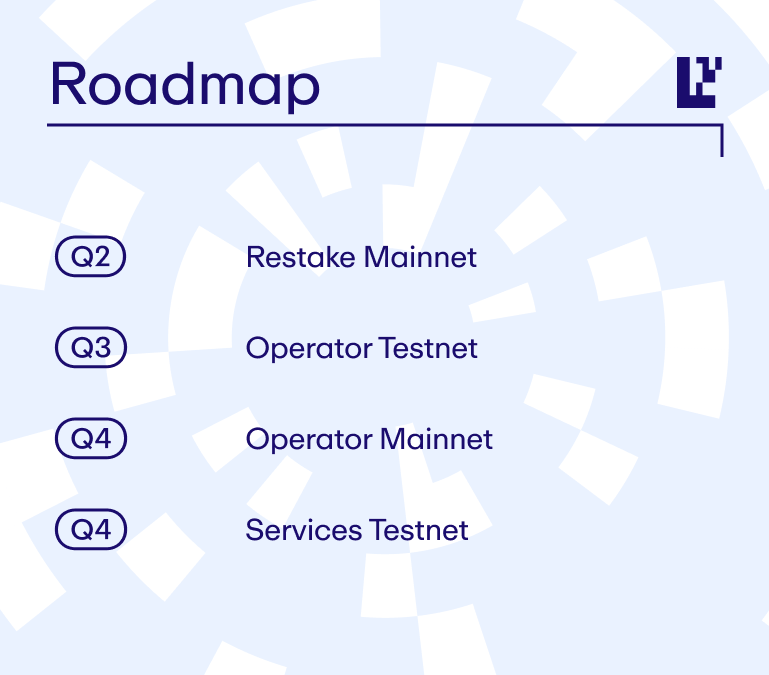

According to the roadmap officially announced by EigenLayer, the main task of the current Q3 quarter is the development of the Operator testnet (node operator testnet), and the development of the AVS service testnet will officially start in the 4th quarter.

https://docs.EigenLayer.xyz/overview/readme/protocol-features/roadmap

The first clear user of EigenDA is Mantle, a rollup project based on the fork of the OP virtual machine. Mantle is currently using the beta version of EigenDA as its DA.

Token Economic Model

EigenLayer is a tokenized project, but its token information and token model have not yet been determined and disclosed.

EigenLayer’s team and financing background

core team

Founder&CEO:Sreeram Kannan

Associate Professor of Computer Engineering at the University of Washington, and founder and controller of Layr Labs, the parent company behind EigenLayer. Published more than 20 papers related to blockchain. Completed undergraduate studies in telecommunications at the Indian Institute of Science, obtained a masters degree in mathematics and a doctorate in information theory and wireless communication at the University of Illinois at Urbana-Champaign, and then worked as a postdoctoral researcher at the University of California, Berkeley. -Head of Blockchain-Lab).

Founder Chief Strategy Officer: Calvin Liu

Majored in Philosophy and Economics from Cornell University in the United States. After graduation, he has been engaged in data analysis, corporate consulting and strategy work for many years. He has worked in Compound as a strategy leader for nearly 4 years and will join EigenLayer in 2022.

COO:Chris Dury

MBA from New York University Stern School of Business. Has extensive cloud service product project management experience. Before joining EigenLayer, he served as the senior vice president of products of Domino Data Lab (machine learning platform), served as the general manager and director of Amazon AWS, and led a number of cloud service projects for game developers. EigenLayer was added in early 2022.

Data source: https://www.linkedin.com/company/eigenl/

EigenLayers team is growing rapidly, and currently has more than 30 employees, most of whom are in Seattle, USA.

Layr Labs is the parent company behind EigenLayer and was also founded by Sreeram Kannan (founded in 2021). In addition to EigenLayer, it also has EigenDA and Babylon (also a project that provides encrypted economic security services, but mainly serves the Cosmos ecosystem. ) two items.

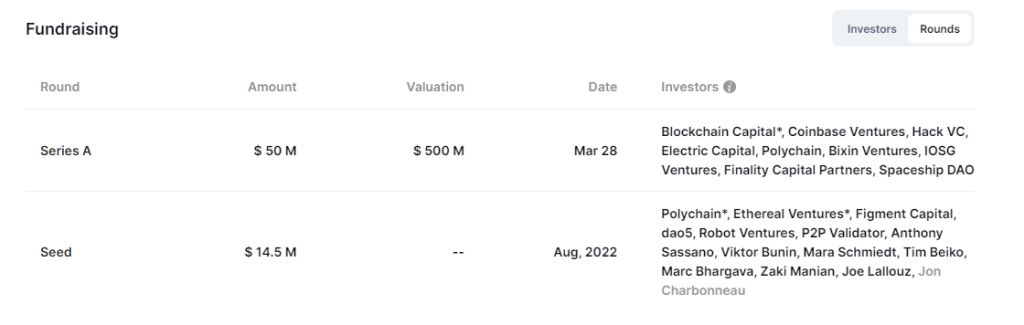

financing

EigenLayer has currently conducted two public financings, namely the 22-year seed round of 14.5 million US dollars (valuation unknown) and the A round of 50 million US dollars (valuation 500 million) completed in March 2023.

Among the well-known investment institutions are the following:

Data Sources:rootdata.com

In the same period of 2023, its parent company Layr Labs also completed nearly US$64.48 million in equity financing, see its report to the SEC for detailsReporting information。

Market Size, Driving Narratives, and Challenges of the Restaking Business

Market Size Forecast

EigenLayer proposed the novel concept of restaking and provided the service of cryptoeconomic security as a Service. Its customer base includes middleware (oracle machines, bridges, Da layers) and side chains\application chains\Rollups, hoping to solve the pain points It is to reduce the decentralized network security cost of these projects (compared to their self-built trust network).

Theoretically speaking, all projects that require token pledge as access, maintain network consensus, and maintain decentralization through game mechanisms are potential users. The current specific size of this market is difficult to accurately estimate. Optimistically speaking, it may be a market that will reach the tens of billions of dollars within three years.

Because the ETH pledge amount of Ethereum is currently 42 billion U.S. dollars, and the total market value of the project is about 200 billion (the above are all data on August 30, 2023), the total scale of funds on the Ethereum chain is 300-400 billion U.S. dollars. Considering that EigenLayers main customers in the future are relatively small and new projects, compared with the absolute leader Ethereums PoS pledge scale of about 40 billion US dollars, the pledge business scale of EigenLayer service projects should be 10-100 million in the short term. billion dollar range.

A narrative that drives project business and expected growth

Demand side:

The arrival of the Cancun upgrade and the opening of the OP Stack have enabled the rapid development of small and medium-sized Rollups and application chains, increasing the total demand for low-cost AVS

The development of the modularization trend of the public chain\Rollup\application chain increases the demand for cheaper DA layers outside of Ethereum, and the expansion of EigenDA increases the demand for EigenLayer, and there is synergy between businesses

Supply side:

The increase in the pledge rate of Ethereum and the number of pledge users have provided abundant LSD assets and holder scale, and they have a strong willingness to improve the capital efficiency and income of LSD assets. In the future, EigenLayer also hopes to introduce LSD capital in addition to ETH.

problems and challenges

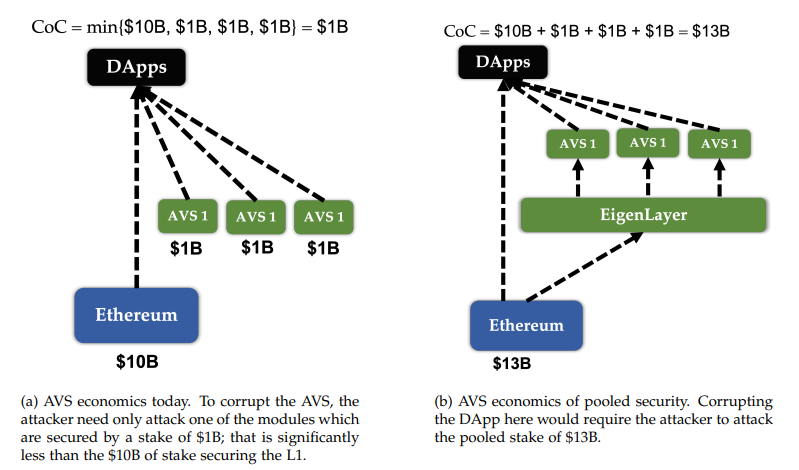

For the demand side of AVS, how much can the combined service of purchasing mortgage assets + professional verification nodes on the EigenLayer platform reduce? It’s hard to say. Using Ethereum’s LSD assets as collateral does not mean that it directly inherits the tens of billions of Ethereum’s security. In fact, the economic security of the project party comes from the leased Ethereum’s LSD assets. It may be faster and easier than building AVS from scratch, but the cost savings ratio may not be too much.

The project party uses other assets as collateral for AVS, which will weaken the scene of its own tokens. Although EigenLayer supports the project partys own token + EigenLayer mixed pledge model, it will still cause considerable obstacles to the adoption of the service.

The project party uses EigenLayer to build AVS, and will worry that due to the dependence on EigenLayer, it will be passive in long-term development and may be stuck in the future. When the project matures, the project party may switch to using its own tokens as pledge assets for network security.

The project party uses LSD collateral as security collateral, and needs to consider the credit and security risks of the LSD platform itself, adding a layer of risk.

competitors

Restaking is a newer concept, pioneered by EigenLayer, and this model currently has fewer followers. But for EigenLayer, the main comparison options among its potential customers are to build their own security network or outsource the security network to EigenLayer. At present, EigenLayer still needs more customer examples to prove the superiority and convenience of its solution.

Valuation deduction

As a new commercial project, EigenLayer lacks clear benchmark projects and benchmark market value. Therefore, we estimate the project’s valuation by predicting the project’s annualized agreement revenue and PS.

Before making a formal estimate, we still need to assume several premises:

EigenLayers business model mainly collects commissions on security service fees from AVS service users. 90% of the service fees are given to LSD depositors and 5% to node operators. EigenLayers commission rate is 5% (this standard is consistent with Lido).

AVS service users pay an average security service fee of 10% per year for the LSD capital they lease.

The reason why 10% is taken is that it is currently a mainstream POS project. The annual rewards provided to PoS pledgers are basically in the 3-8% range. Considering that most of the projects that will use EigenLayer are newer projects, the initial incentive ratio will be higher. , so the author selects 10% as the average security service fee ratio.

PoS reward ratios of major L1s, data source: https://www.stakingrewards.com/

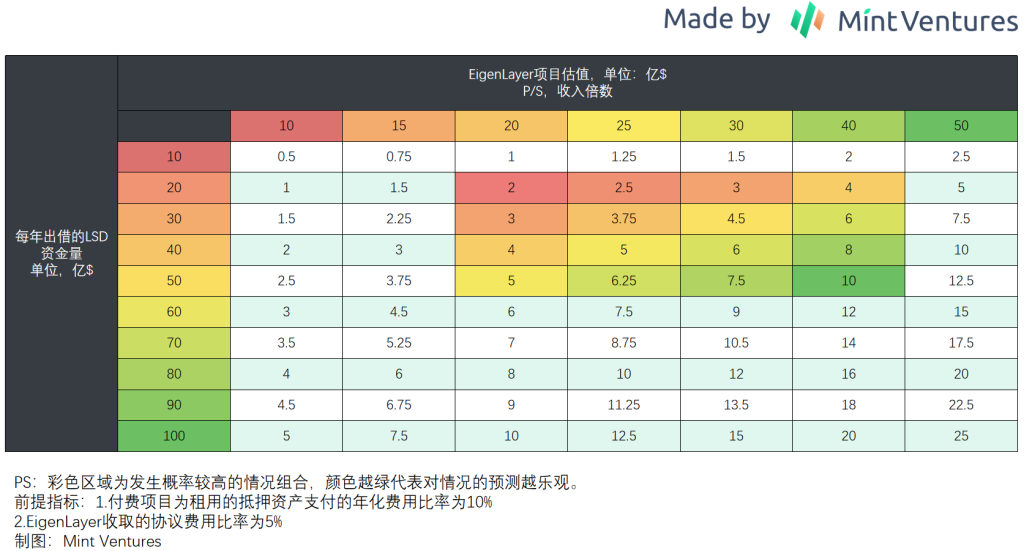

Based on the above assumptions, the author obtained the following project valuation range based on the amount of LSD assets lent by EigenLayer and the corresponding PS. The colored part of the valuation area is the valuation range that the author believes has a higher probability. The greener the color, the higher the prediction. optimism.

The reason why the author determines the area of LSD asset annual lending volume is 2 billion to 5 billion and PS is 20 to 40 times as a range with a higher probability of valuation is because:

Today, the market value of the PoS pledged tokens of the top ten public chains alone is about 73 billion US dollars. If Aptos and Sui are included, the market value is nearly 82 billion. However, the pledges of these two projects mostly come from unreleased team and institutional tokens. During the cautious period I eliminated these two outliers. The author assumes that EigenLayers LSD share can account for about 2.5% -6.5% of the total PoS staking market (note, slap your head), corresponding to a market amount of 2-5 billion. As for whether a 2.5% -6.5% share is reasonable? Readers have different opinions.

The PS value of 20-40 times is based on Lido’s current PS of 25 times (data on 23.8.30, using the full circulation market capitalization as the market capitalization base). Newer narratives may enjoy higher returns when they first debut. premium.

Based on the above calculations, US$200 million to US$1 billion may be a reasonable valuation range for EigenLayer. First-tier investors who participated in the project with a valuation of US$500 million may not have left too much space for themselves, considering the various restrictions on token unlocking. Much safety margin. If, as rumored, there are investors who want to buy EigenLayer tokens OTC at a valuation of US$2 billion, they should be even more cautious.

Of course, it should be noted that the above valuation is a valuation deduction for the entire EigenLayer project. What the specific market value of the token should be depends on the specific capture ability of the token in the business, such as:

What percentage of the protocol’s revenue will be attributed to token holders?

In addition to repurchase\dividends, does the token have a relatively rigid application scenario in the business to increase the demand for it?

Will EigenDA share the same token with EigenLayer to provide more scenarios and needs for the token?

If the empowerment of points 1 and 2 is insufficient, it will further weaken the intrinsic value of EigenLayer tokens. If there are unexpected surprises in point 3, it will increase the value of the tokens.

In addition, the market value of EigenLayer when it debuts also depends on the market bull and bear environment at that time.

Lets wait for the markets answer.