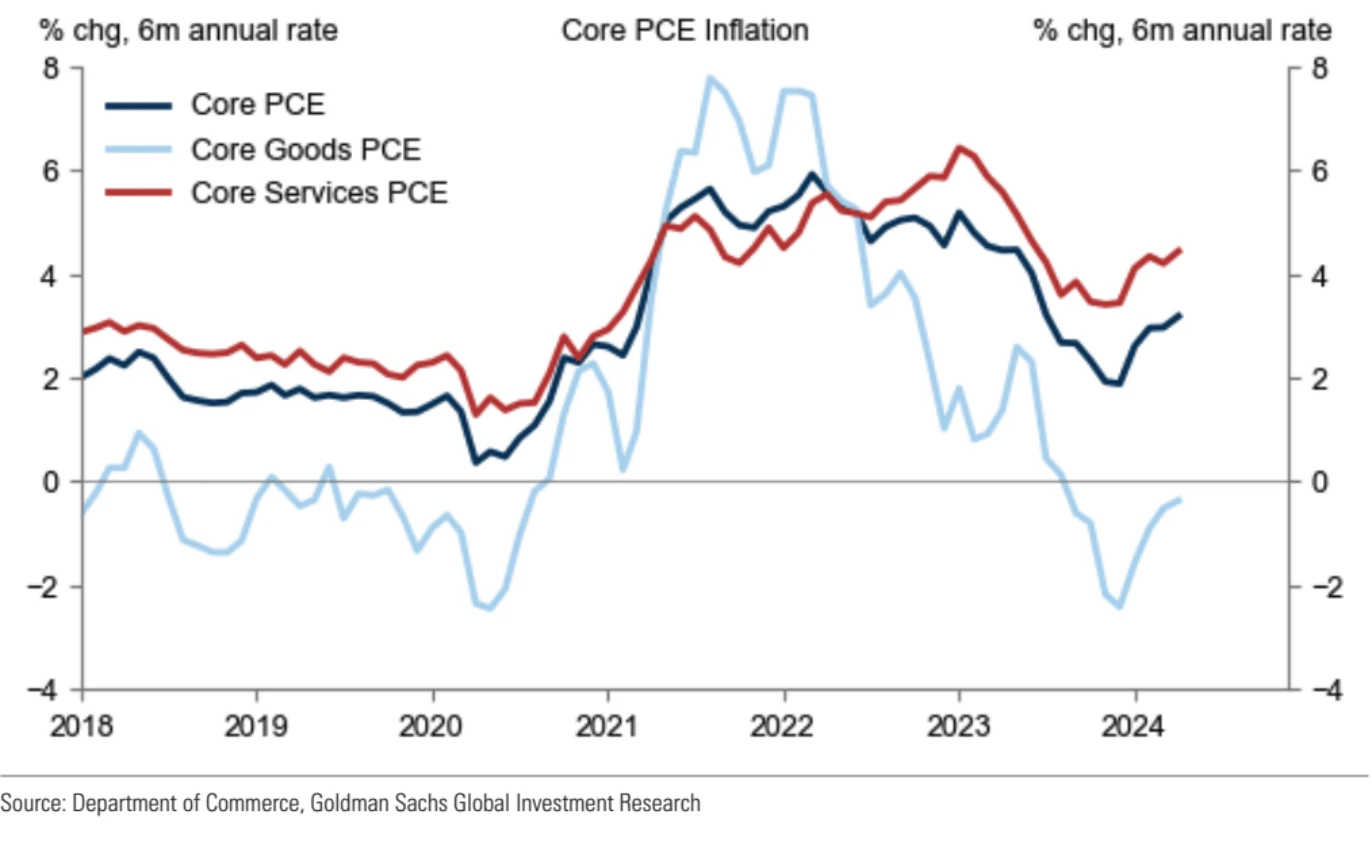

This weeks data before the release of GDP on Thursday and PCE on Friday were relatively mixed. The relatively heavy first-quarter GDP revisions and April PCE data were generally dovish. The core PCE, an inflation indicator that the Federal Reserve attaches importance to, grew by 0.2% month-on-month, lower than the expected 0.3%. The unrounded value was 0.249%, so it was only rounded down to 0.2%. Although it was still lower than the previous value of 0.317%, such a coincidental number made people doubt the possibility of data manipulation, and the actual decline was less than 0.1 percentage point. Such data basically would not change the Feds views on inflation, so the market fell after a brief rise.

The core PCE 6-month annualized rate fell below 2% at the end of last year, which was also the time when the market was most optimistic. The past four months have been the first major setback in this round of inflation:

The US economy grew 1.3% in the first quarter, which was released a day earlier, slowing down significantly from 3.4% at the end of last year and the initial value of 1.6%. The growth of personal consumption expenditure (PCE), the main economic growth engine, slowed down to 2.0% in the first quarter, which was 2.5% in the initial value. Personal spending grew by only 0.2% month-on-month, actual spending fell by 0.1%, and commodity spending fell by 0.4%, which was consistent with the weak retail sales in April.

Most of the economic data in the past month are negative, which is theoretically a good environment for current risk assets:

Recently, more and more data point to a slowdown in US consumer momentum. The current moderate growth in overall spending is supported by travel and entertainment projects, while all aspects except insurance spending have slowed down, and the growth of rent payments has also slowed down across the board. Bank of Americas CEO said in a speech last week that US consumer spending through credit card payments, checks and ATM withdrawals has increased by about 3.5% this year, a significant slowdown from the growth rate of nearly 10% in the same period in May 2023. Whether it is households or small and medium-sized businesses, these important customers of US banks are slowing down their purchases of everything from hard goods to software. (But spending growth in the eurozone, the UK and Canada is beginning to improve)

Secondary market yields continued to fall on Thursday and Friday, but the cryptocurrency market lacked momentum and failed to form an inverse linkage. The correlation between Bitcoin and secondary interest rates has declined recently:

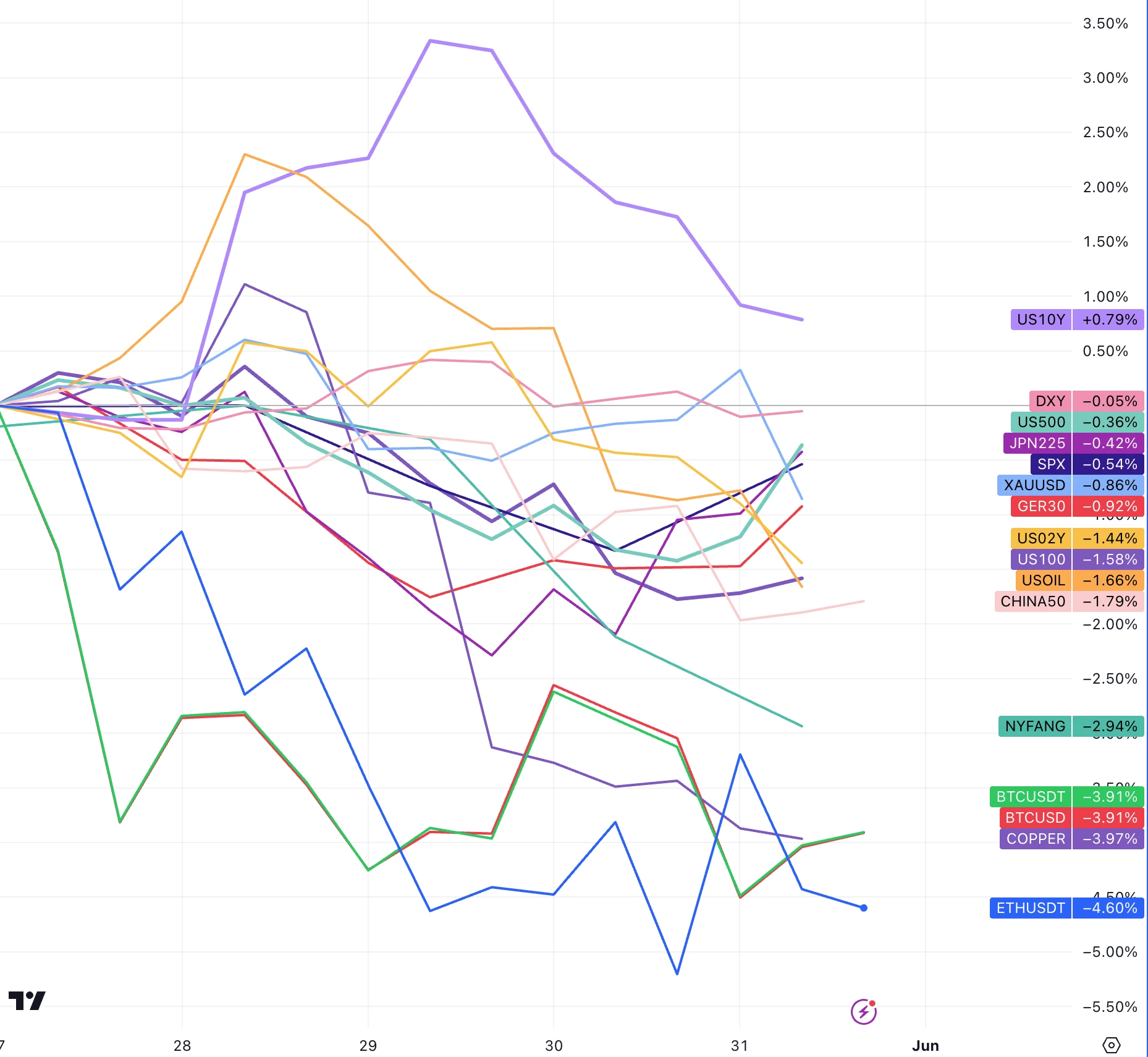

Stocks fell briefly after the PCE data on Friday, but quickly pulled back, showing that the stock market remains strong. However, among technology stocks, performance was differentiated, with Amazon, Microsoft, and Google performing poorly, and only NV showing a significant increase. As shown in the figure below, after the rebound on Thursday and Friday, the SP 500 fell only 0.36% for the whole week, while the Nasdaq 100 fell 1.58%, and the FANG+ index fell 2.94%. The software industry ushered in the worst earnings season in history, causing the overall decline in the technology stock index. The most eye-catching thing was that the cloud software giant Saleforces quarterly revenue was lower than expected for the first time in 18 years, and its guidance for this fiscal year was also inferior. The stock price plummeted by 20%, the largest daily decline in nearly 20 years, leading the drag on the stock index. Some analysts pointed out that the market style may switch in the future, and technology stock investment may become a painful transaction.

Bloomberg analysis believes that currently few software companies revenues are boosted by AI. Although the software industry will eventually benefit from AI, it may take years to build it up, and there is no hope of improving performance in the second half of this year. Some analysts also believe that the current sharp correction in software stocks provides investors with a good opportunity. Bernstein analysts believe that leading companies with higher profit certainty such as ServiceNow are more valuable for investment after valuation repair.

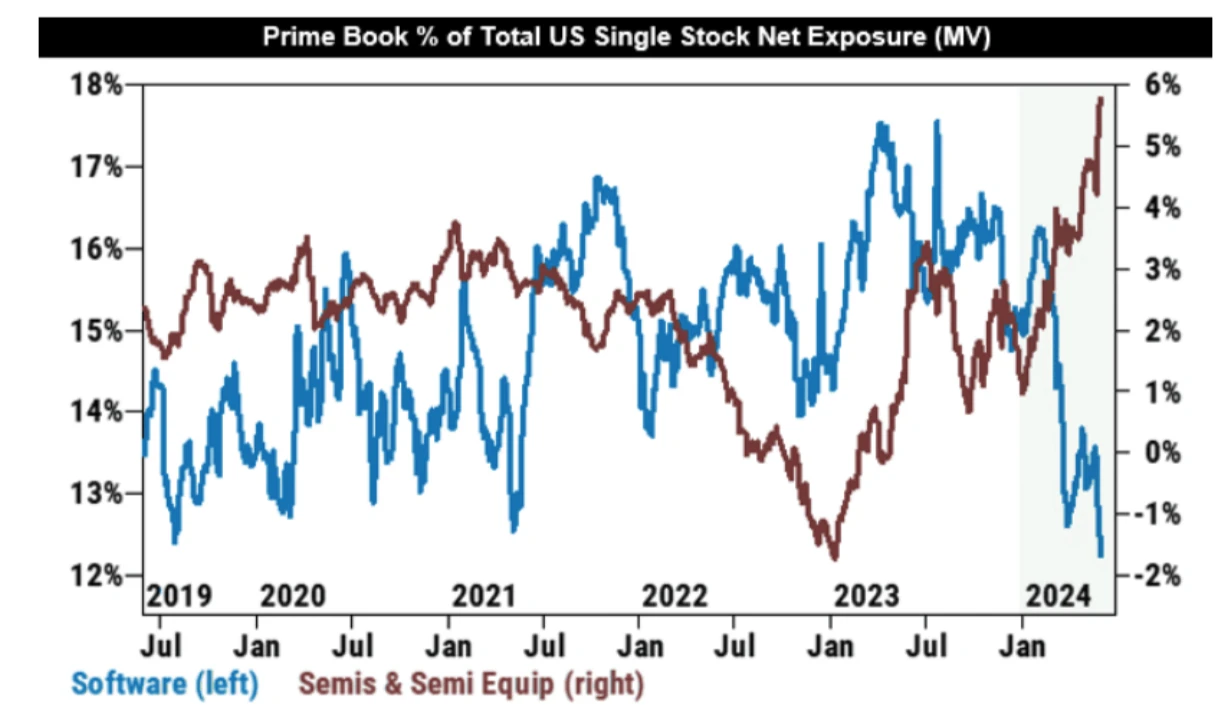

As funds exposure to semiconductor stocks increased, net software exposure reached its lowest level in 5 years:

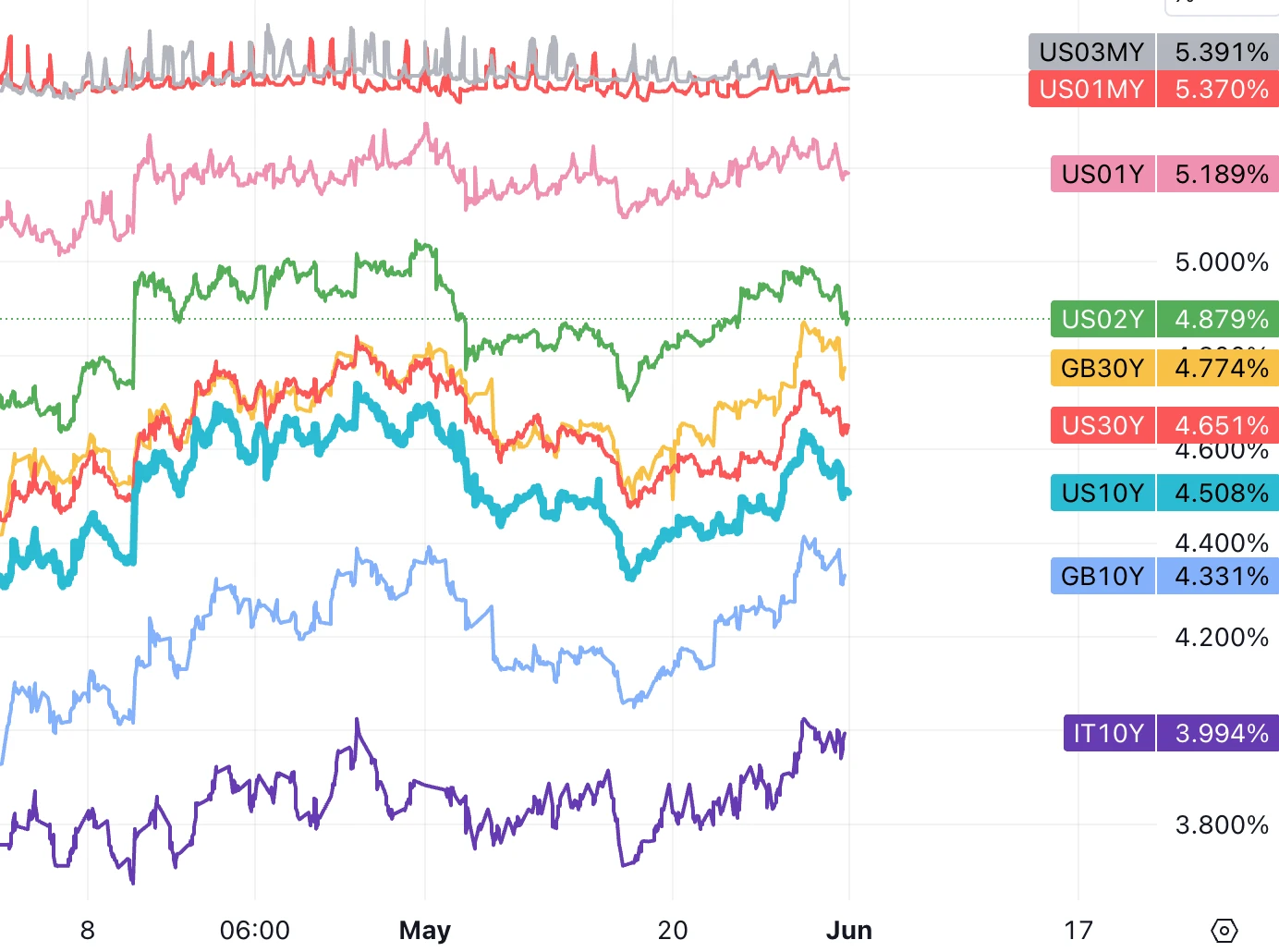

US 2-year yields fell from a high of 5% to 4.88%, and US 10 Y fell from 4.64% to 4.5%. The Fed minutes a week earlier pushed secondary market interest rates to a one-month high. Fed Chairman Powell vowed at a press conference after the meeting that the Feds next move was unlikely to be a rate hike. However, the details of the meeting minutes revealed that Powells dovish statement at the time may have largely overshadowed the voices of hawkish officials.

ECB and European stocks

Due to the stubborn inflation in the eurozone service sector, the CPI rebounded from 2.4% in April to 2.6% in May, exceeding the market expectation of 2.5%, causing Germanys 10-year government bonds to hit a new high since November last week. Although the higher-than-expected inflation increase is unlikely to prevent the ECB from cutting interest rates this week, it may give the ECB more reasons to suspend interest rate cuts in July and slow down the pace of interest rate cuts in the coming months. (In addition to the ECB, the Bank of Canada will also cut interest rates this week, and the Bank of England is expected to cut interest rates in August)

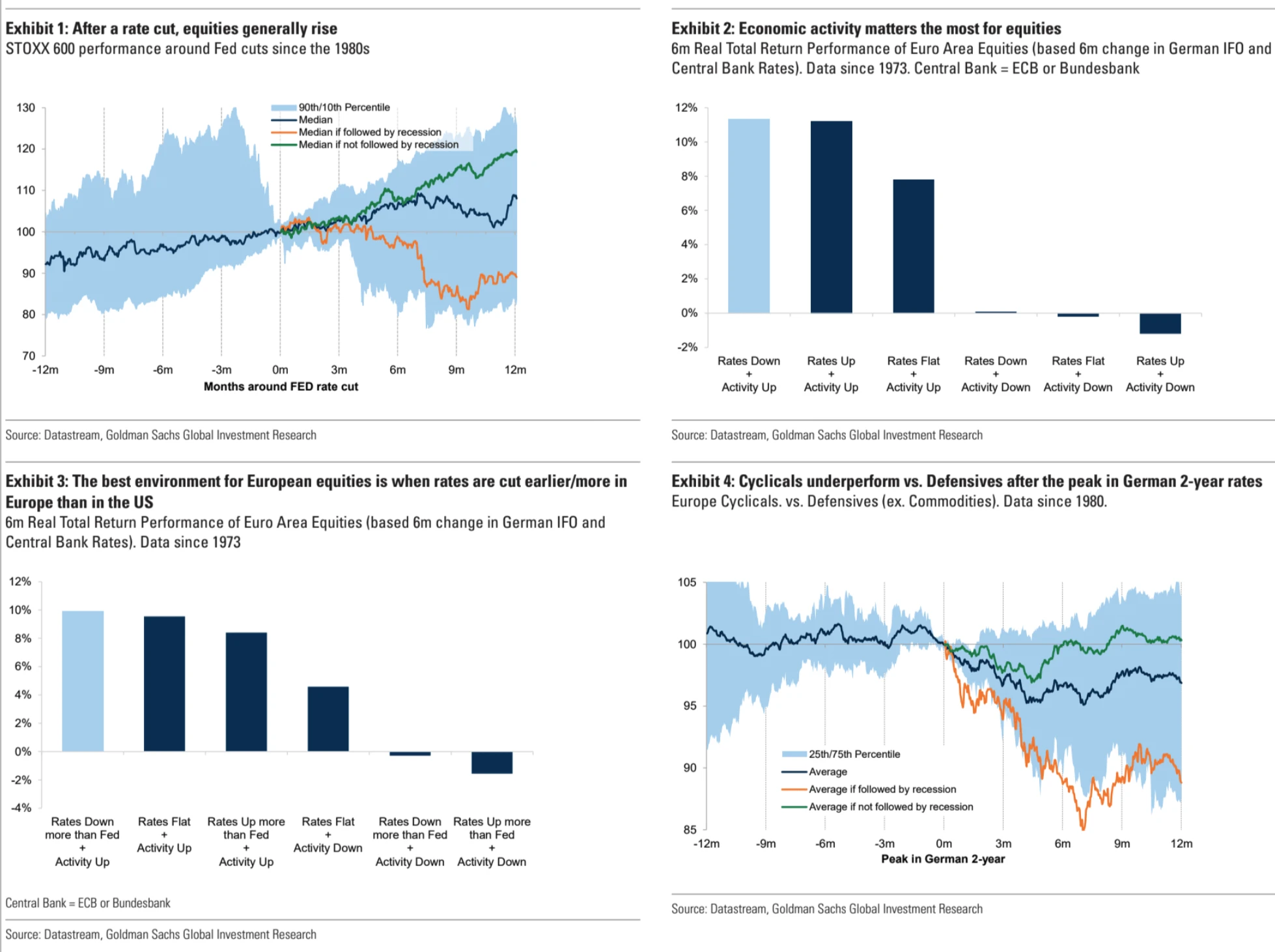

Falling interest rates and rising economic activity are the best environment for stock markets to perform. The Eurozone economy has escaped five consecutive quarters of stagnation. Economists expect Europes GDP to grow positively this year and next (+0.8%, +1.4%). If the momentum can be maintained, the outlook for European stocks is optimistic, especially when European interest rates are cut earlier/more than in the United States (Figure 3 below):

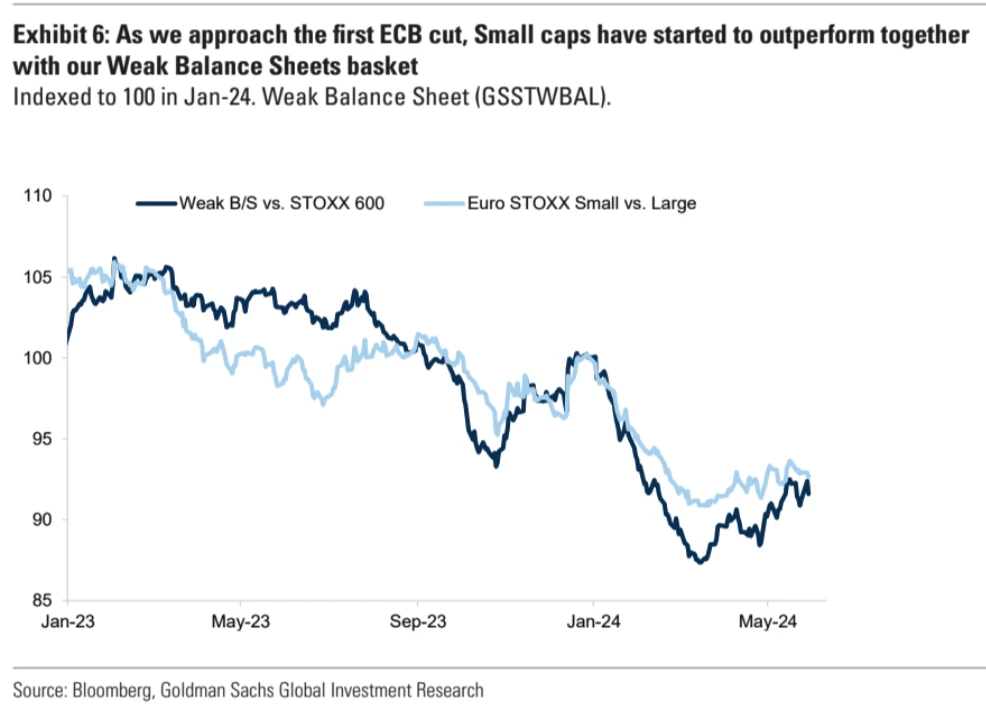

Goldman Sachs believes that when interest rates are cut in the context of improved activity, the utilities and real estate sectors, which are usually sensitive to interest rates, will not benefit that much from the rate cuts. Instead, small-cap stocks and companies with weaker balance sheets will benefit more:

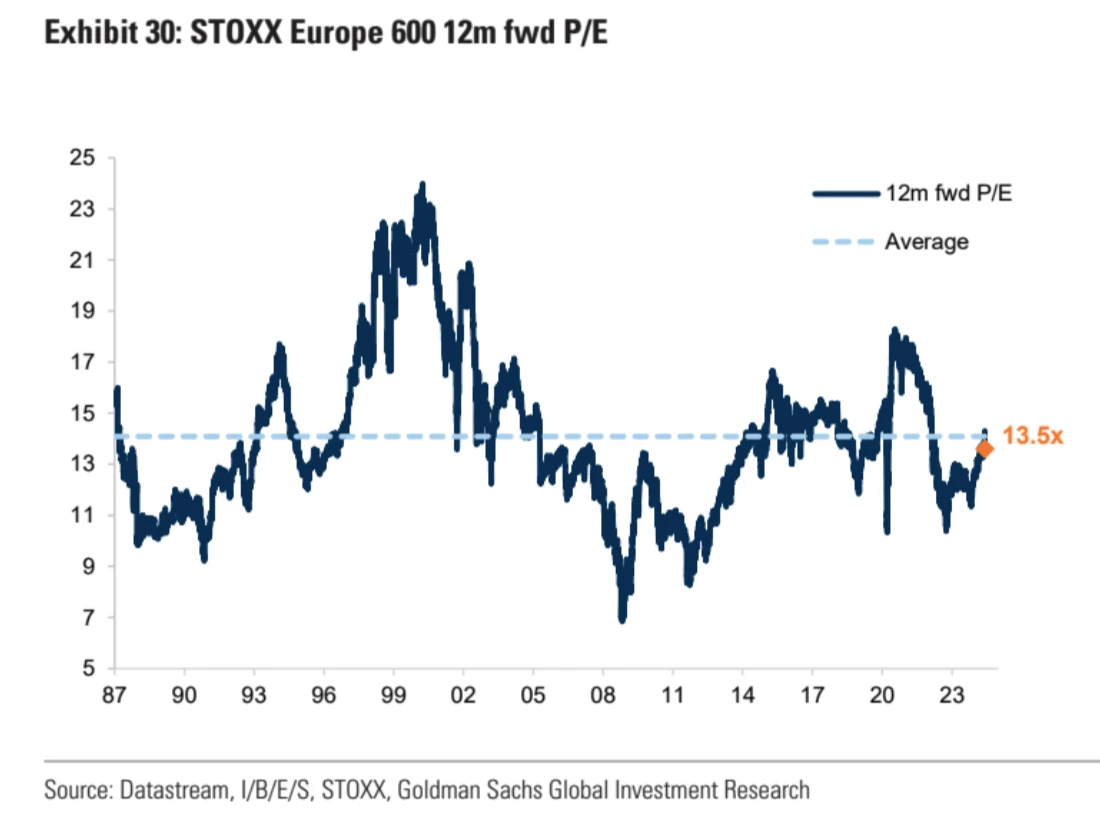

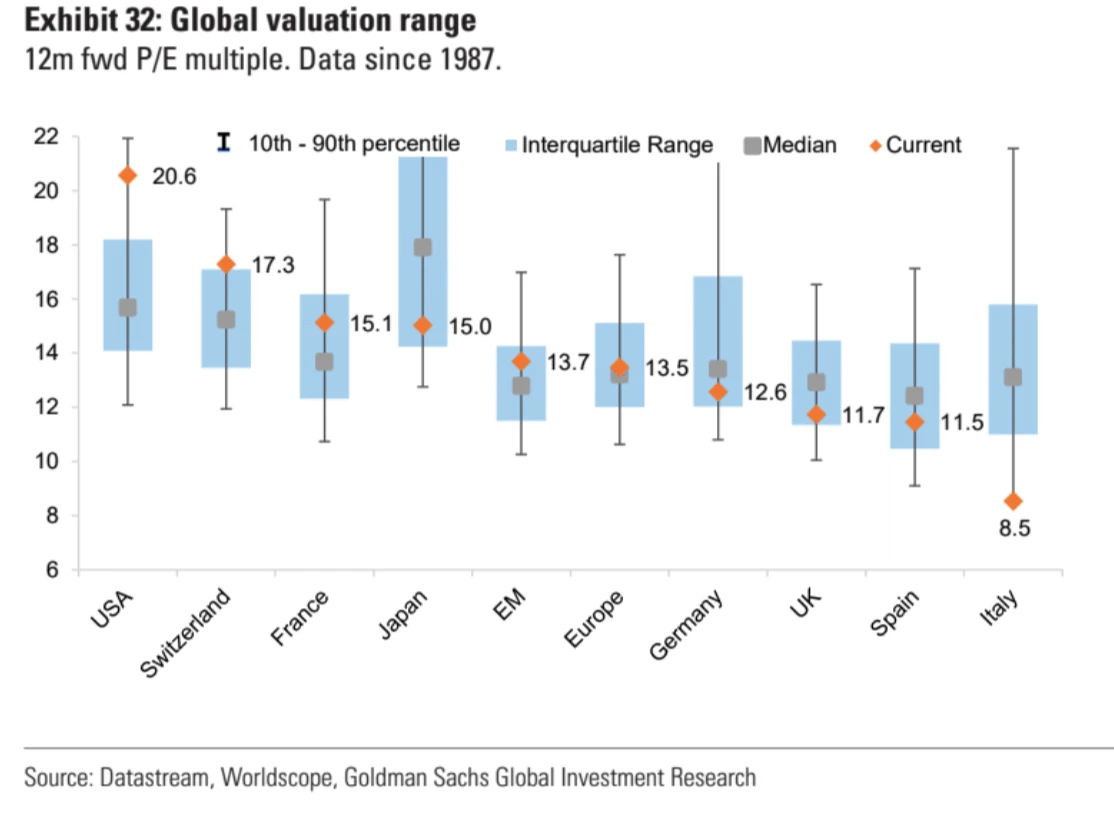

The valuations of European stocks in major global markets are relatively low compared to history:

On the swing of interest rate cuts

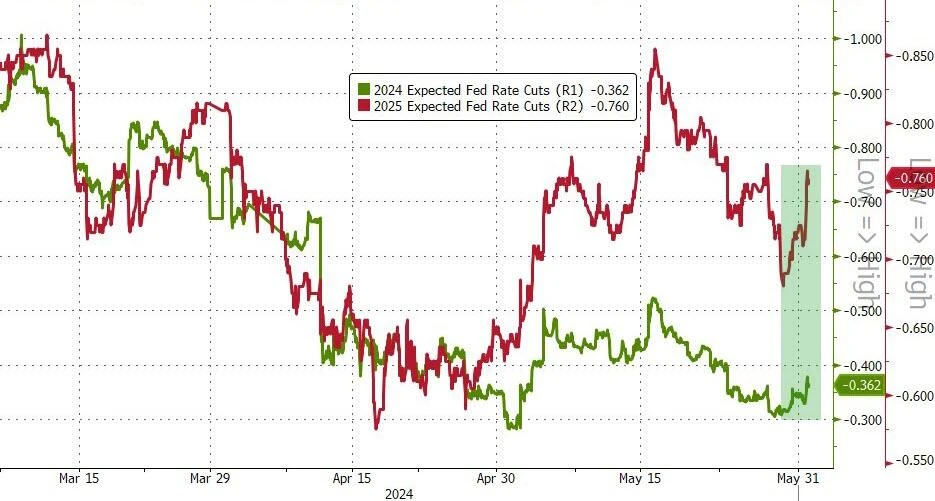

The decline in yields in the United States is accompanied by an increase in expectations for rate cuts, which are expected to rise to 36 bp this year, just under 1.5 times, and 76 bp next year, about 3 times. Comments from Fed officials indicate that a July rate cut may require a significant improvement in inflation figures over the next two months and a significant weakening in labor market data.

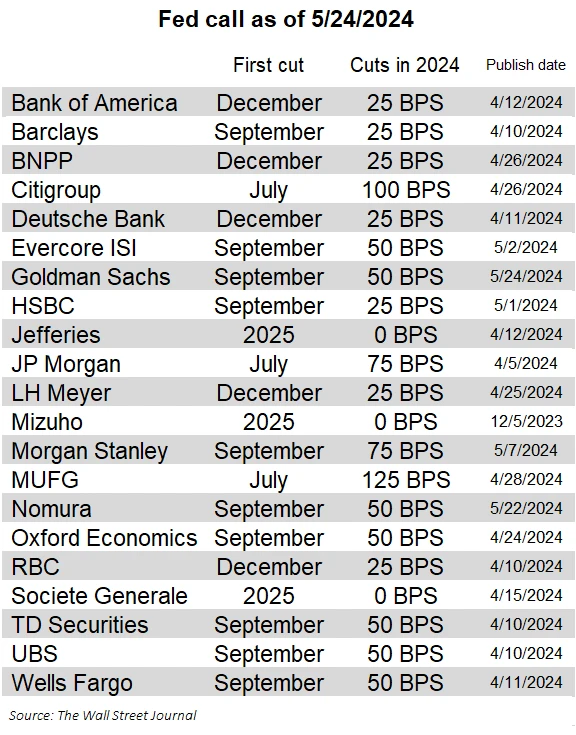

At present, the market is divided and no unified view has been formed, so the amplitude of the price fluctuation will still be large, ranging from 0 to 4 times, and the overall rightward deviation will be larger. For example, Bank of America expects to cut interest rates only once in December this year, while Goldman Sachs expects to cut interest rates twice starting in September.

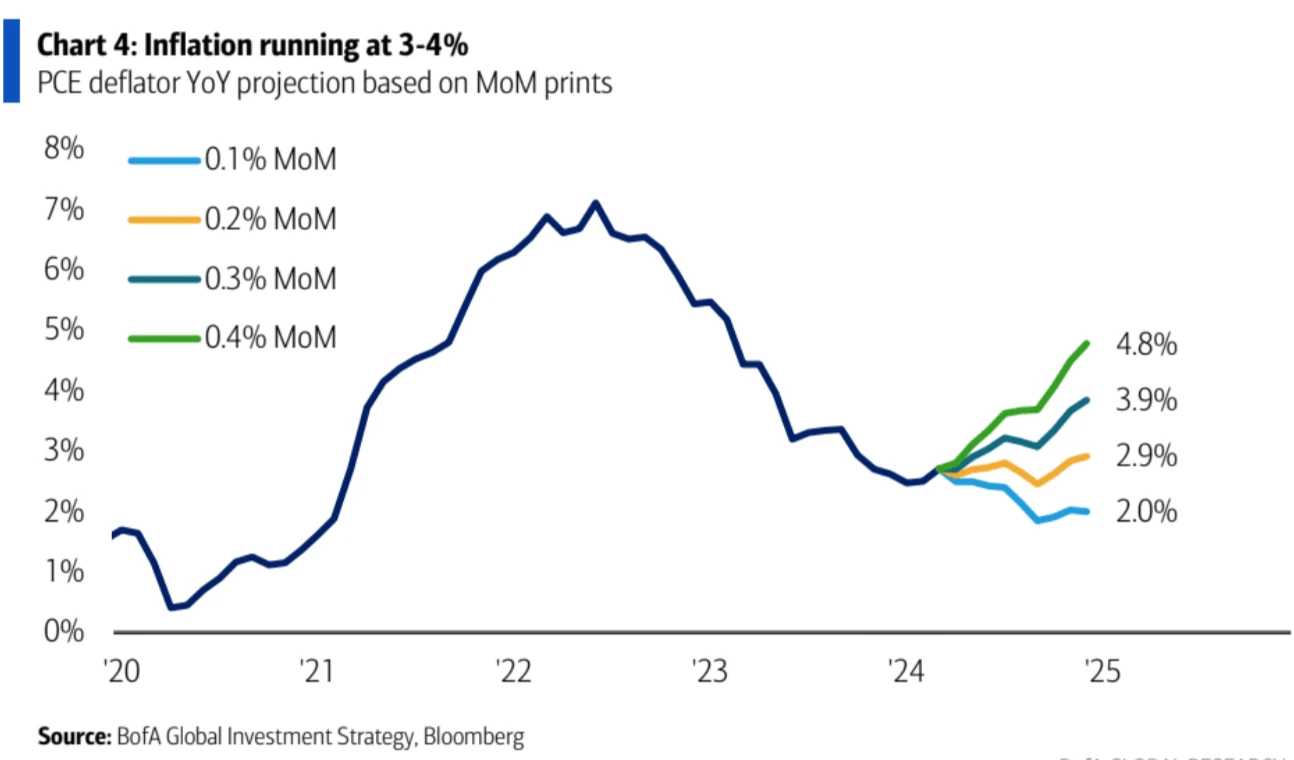

PCE needs to maintain a month-on-month growth rate of 0.2 or lower, and the year-on-year figure is expected to decline in the fall:

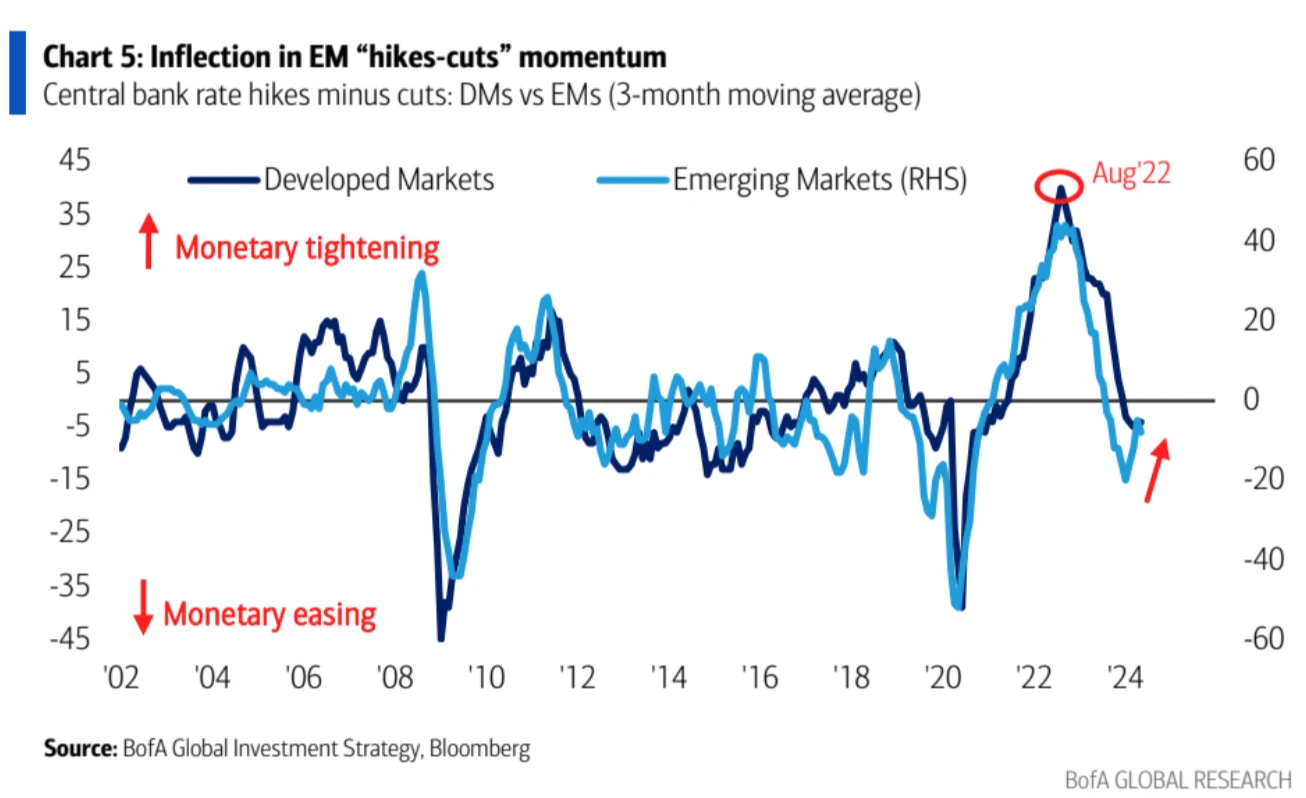

Monetary policy in emerging market countries, which usually serve as a leading indicator, has become less dovish in the face of the recent rebound in prices:

NV received a little challenge

Chip stocks such as NV and AMD fell at one point due to the news that the United States was conducting a national security review of the development of artificial intelligence in the Middle East and might slow down the issuance of export licenses for chips to the Middle East, but NV and AMD still closed up 4.9% and 3.6% respectively for the week. It is not clear how long this review will last, nor what counts as large-scale exports.

In addition, UBS pointed out in its latest report that Nvidia may have a VVVVIP customer, and this mysterious customer contributed 19% of Nvidias total revenue in fiscal 2024. UBS speculated that this customer might be Microsoft. Such highly concentrated revenue has caused market concerns and poured some cold water on NVs rise (but not much). So far this year, NVs stock price has risen 130%, with a market value of more than $2.7 trillion, just one step away from Apple (although this years expected revenue is only one-third of Apples). However, NVs biggest recent positive is the stock split and inclusion in the Dow Jones, both of which usually bring considerable buying, and it is difficult to see NV falling significantly before it happens.

China

The Hang Seng Index fell 2.8% and the CSI 300 fell 0.7%. TH Junyan, the PMI unexpectedly fell into the contraction range, and the general decline in domestic and foreign demand was the main negative news.

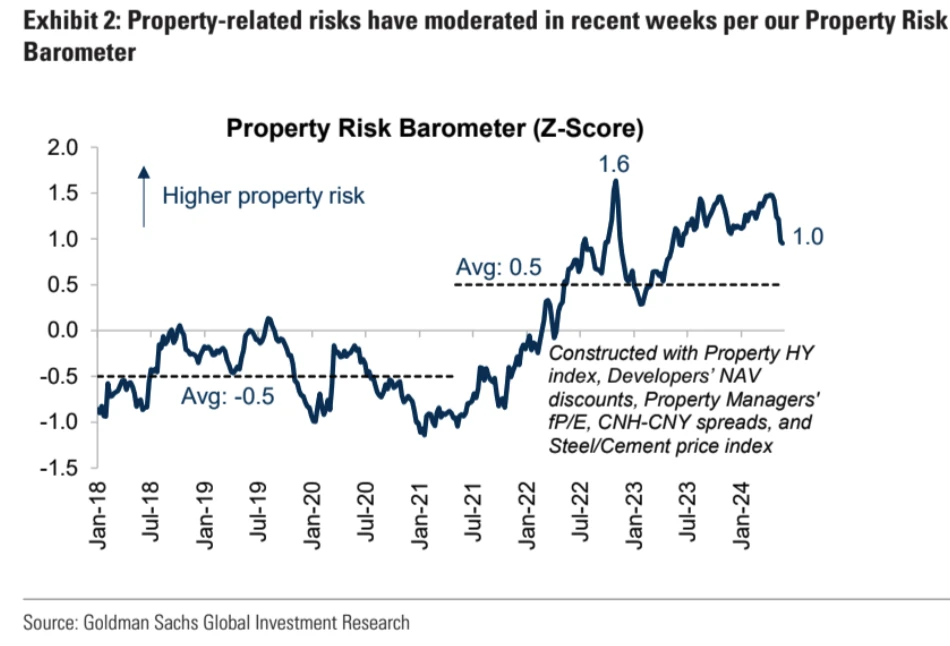

But risks related to real estate have eased in recent weeks due to more policy easing and support:

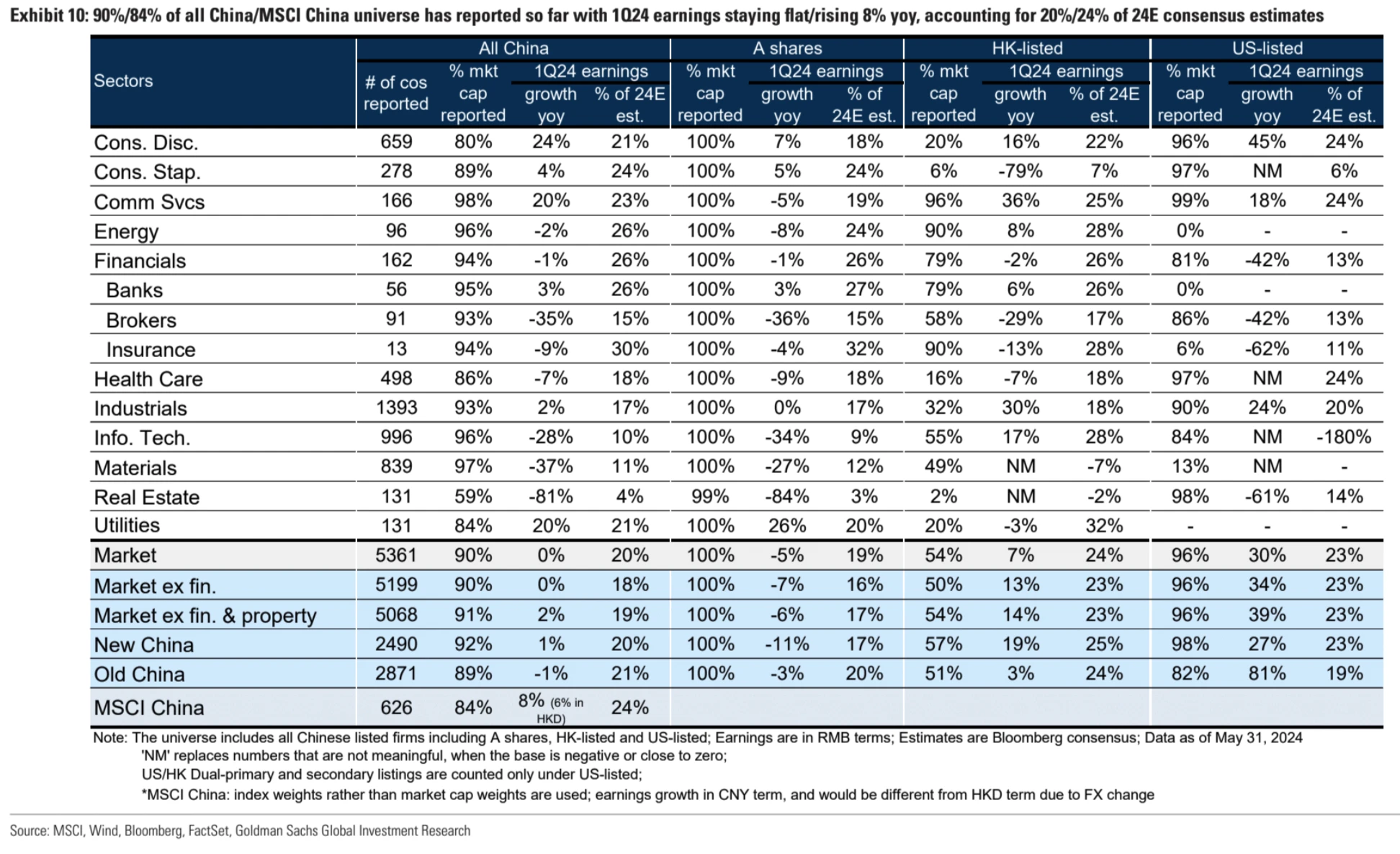

About 90% of Chinese companies have reported Q2 4 earnings, with overall earnings up 0% year-on-year, but the market expected a 20% increase for the full year. There seems to be a huge gap between the actual data and expectations.

Fund Flow and Positions

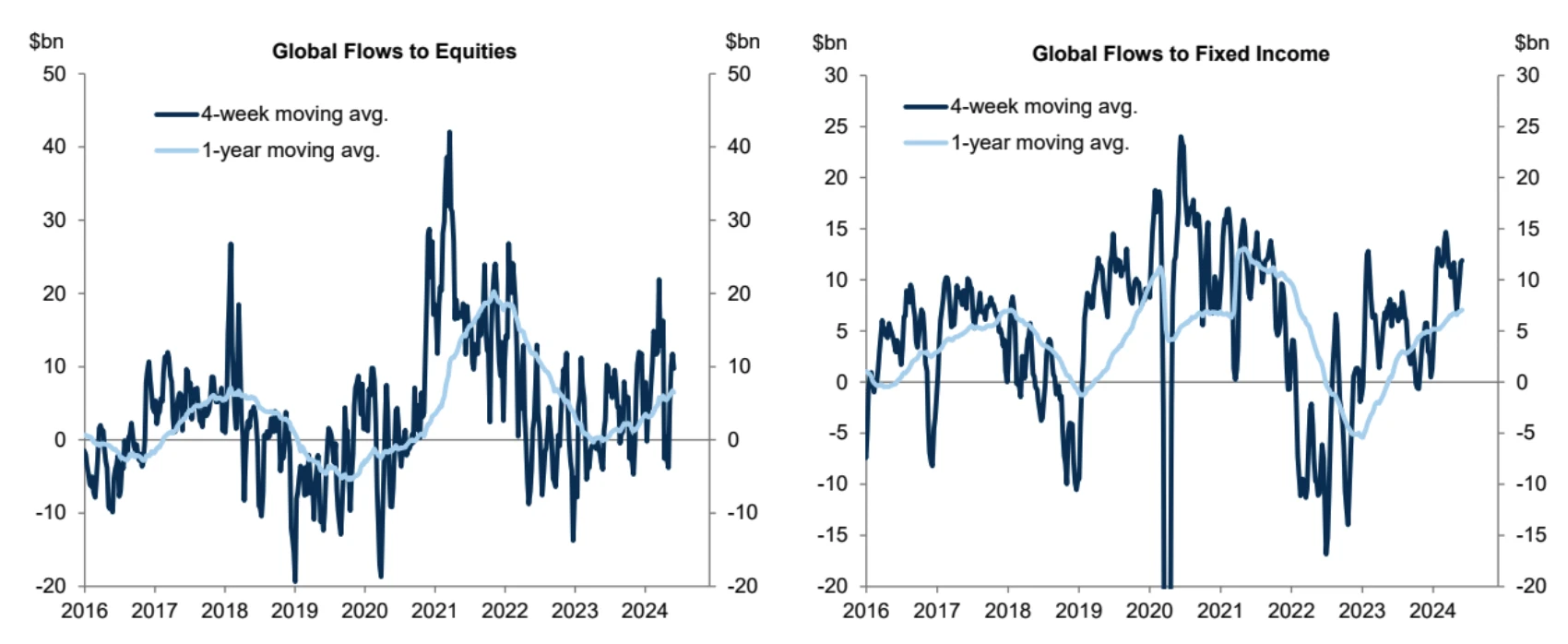

Inflows into global equity and bond funds were modest in the week ended May 29.

Equity Funds: Global equity funds saw positive net inflows (+$2 billion), down from the previous week (+$10 billion). The US saw small inflows, while the rest of the G10 was mostly negative.

Bond Funds: Global fixed income fund inflows slowed, with lower inflows into government, IG credit and high yield bond funds.

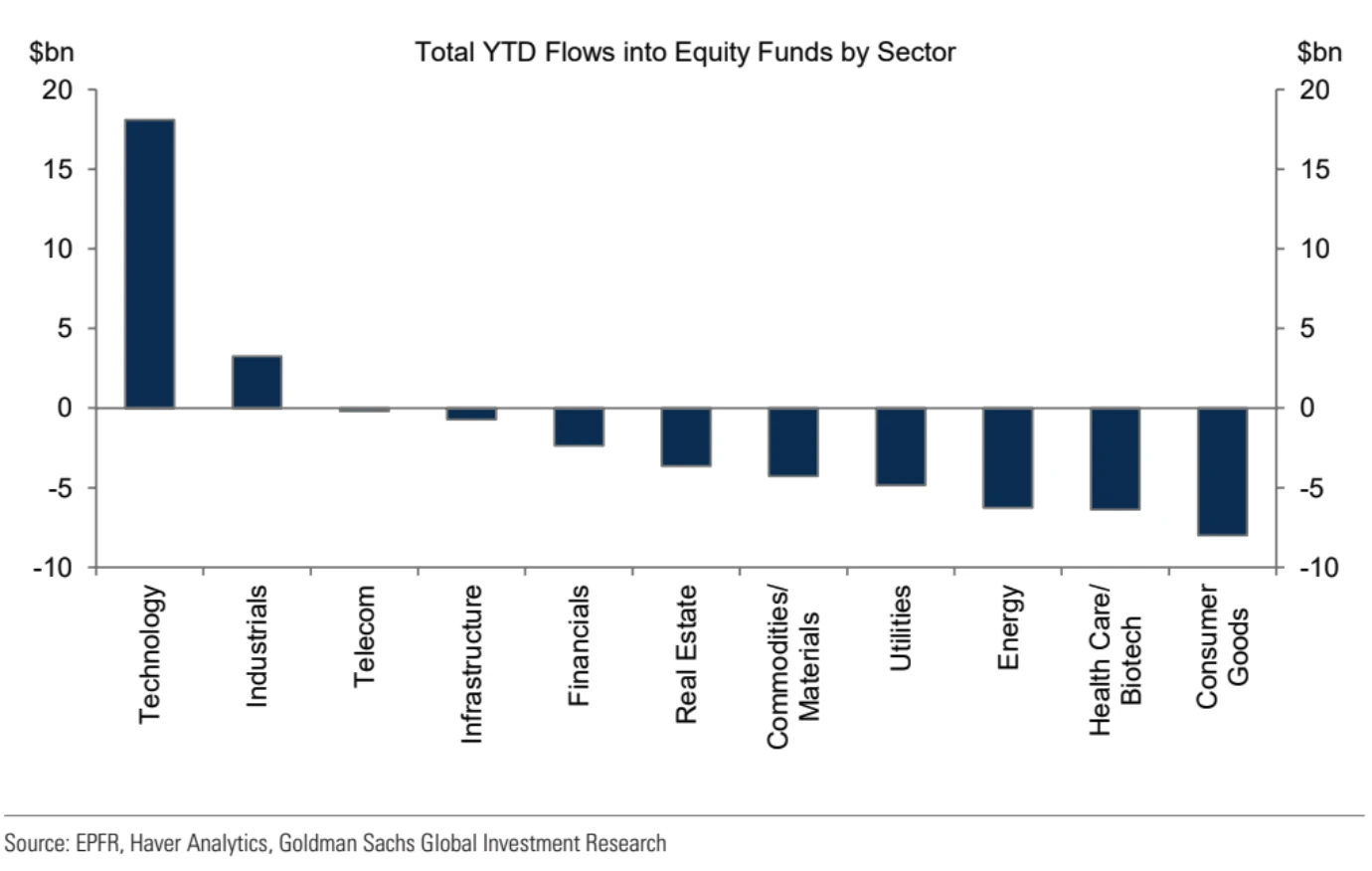

Sector Flows: Technology funds attracted the largest inflows. Most sector funds, except for technology funds and industrial funds, have seen net outflows year-to-date.

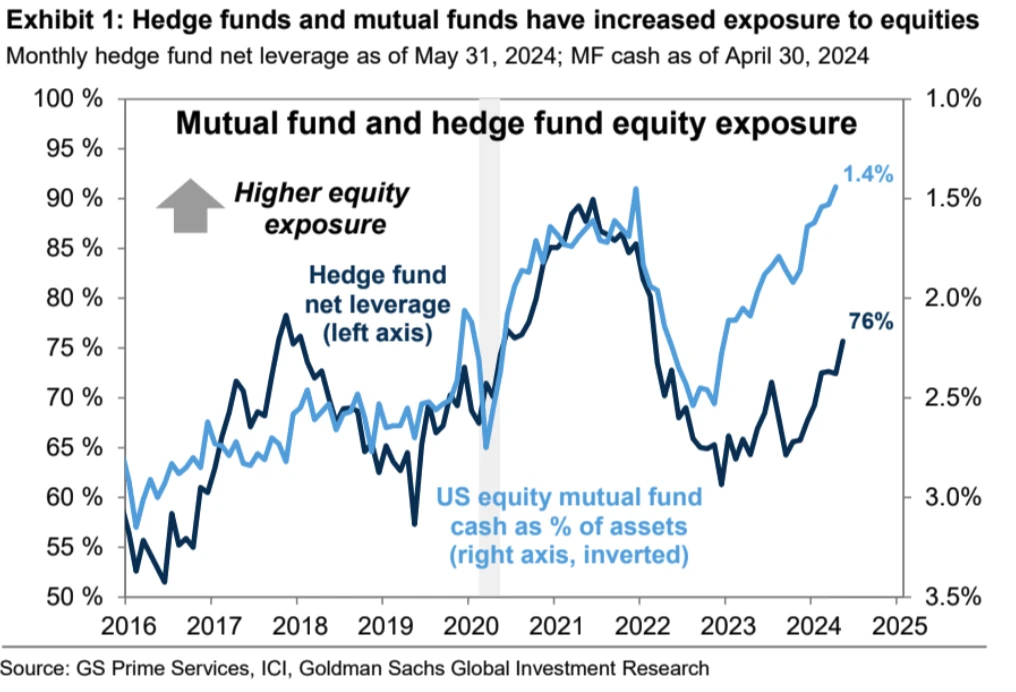

Hedge funds and mutual funds have continued to increase their exposure to stocks this year, with hedge fund net leverage close to its highest level in the past year and mutual fund cash balances falling to a record low of just 1.4%:

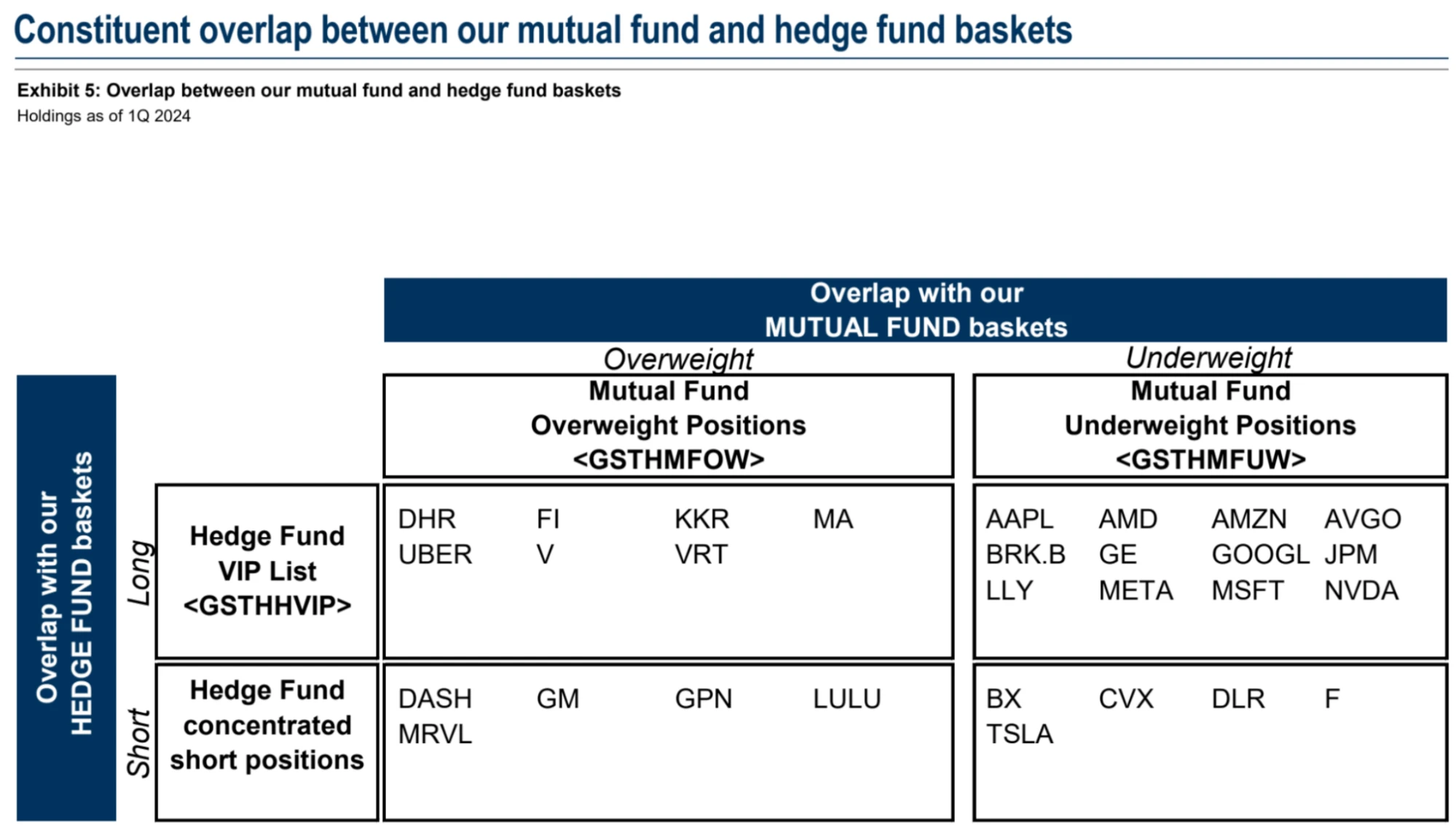

Goldman Sachs analyzed the first quarter holdings of 707 hedge funds (with a total stock holding of $2.7 trillion) and 482 mutual funds (with stock assets of $3.3 trillion). The conclusions are as follows:

Hedge funds and mutual funds generally reduced their positions in Mag 7, with only AAPL being added

Mutual and Hedge Fund Favorites: DHR Education Services, FI Real Estate Investment Trust, KKR Private Equity, MA Payment Processing, UBER Ride Services, V Payment Processing, VRT Data Management

Stocks that are underweight by mutual funds and shorted by hedge funds: BX Banks CVX Energy DLR Air Transport F Automotive TSLA Electric Vehicles

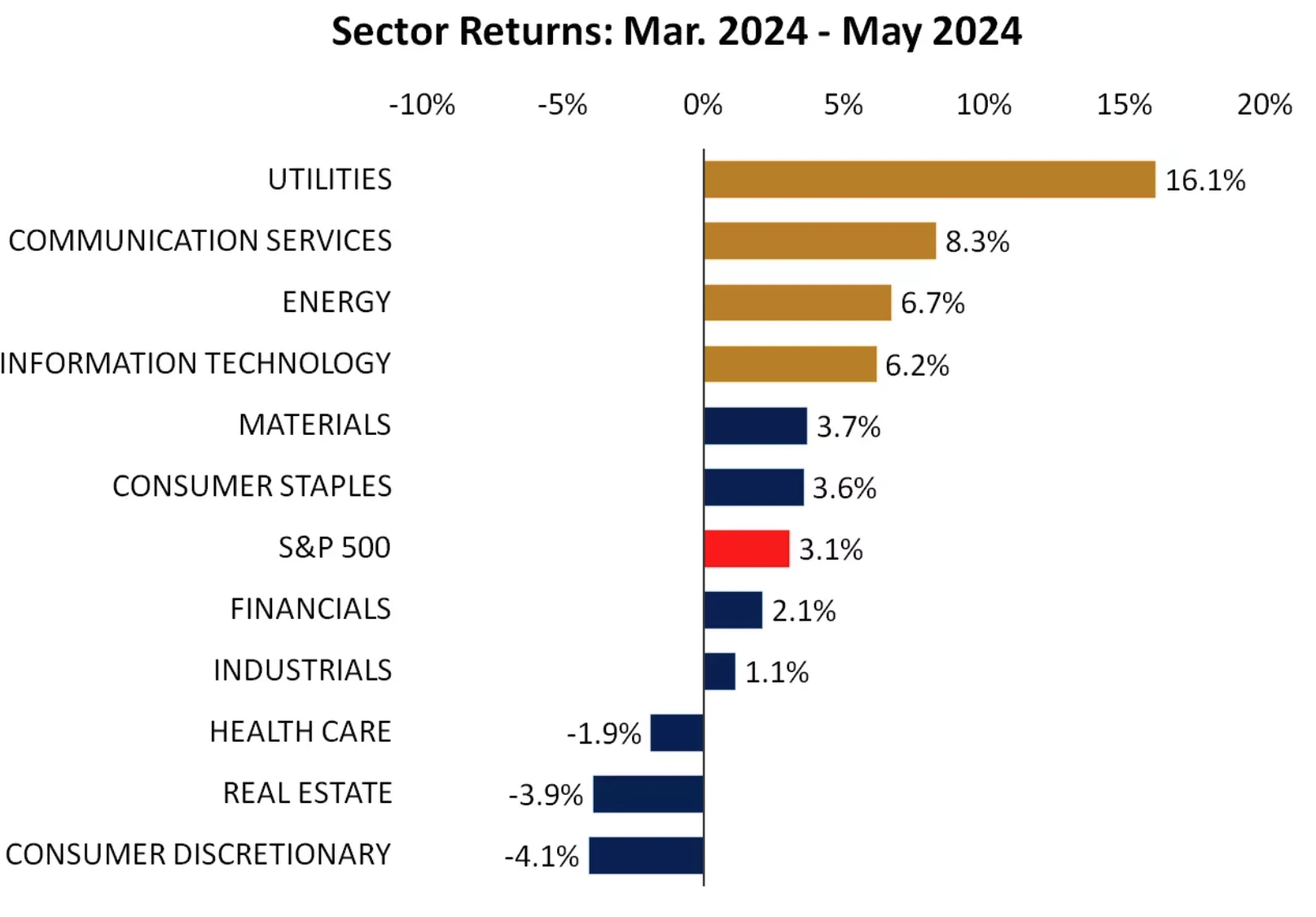

Investor enthusiasm for the expanding AI sector is reflected in increased exposure to the utility sector, as running and training AI models requires large amounts of electricity.

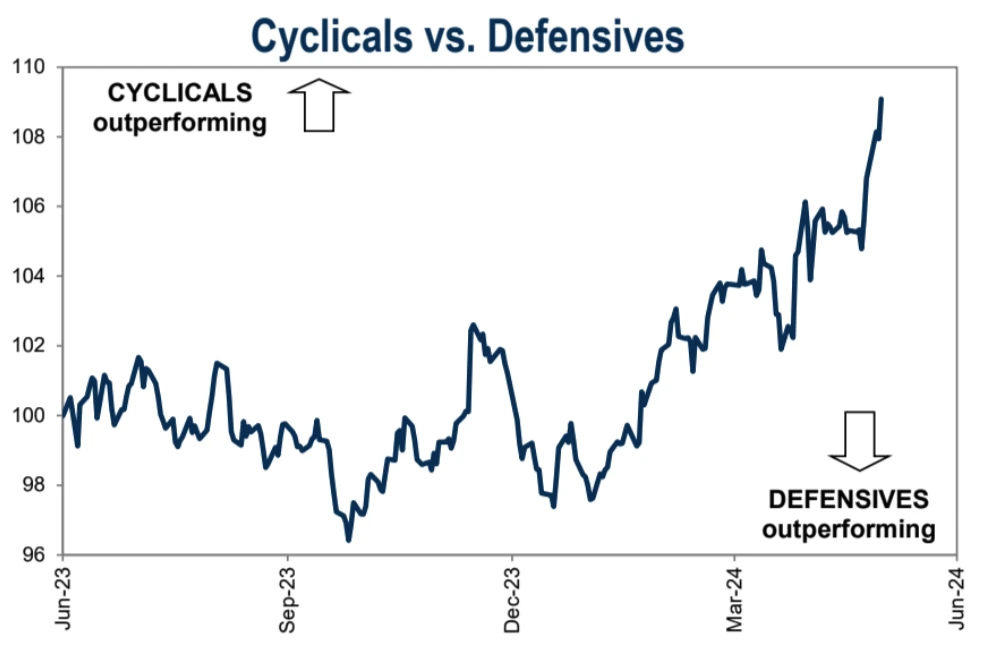

The fund has maintained its pro-cyclical tilt, and in fact cyclical stocks have outperformed defensives year-to-date.

Some analysts believe that while technology stocks still occupy most of the headlines and attention, we have quietly seen the expansion of this leadership reflected in areas such as utilities and energy, as well as occasional rebounds in other areas such as finance, industry and healthcare. Style switching may become the next theme. In fact, technology stocks have lagged behind utility stocks since April, which may reflect a larger trend: the expansion of the bull market.

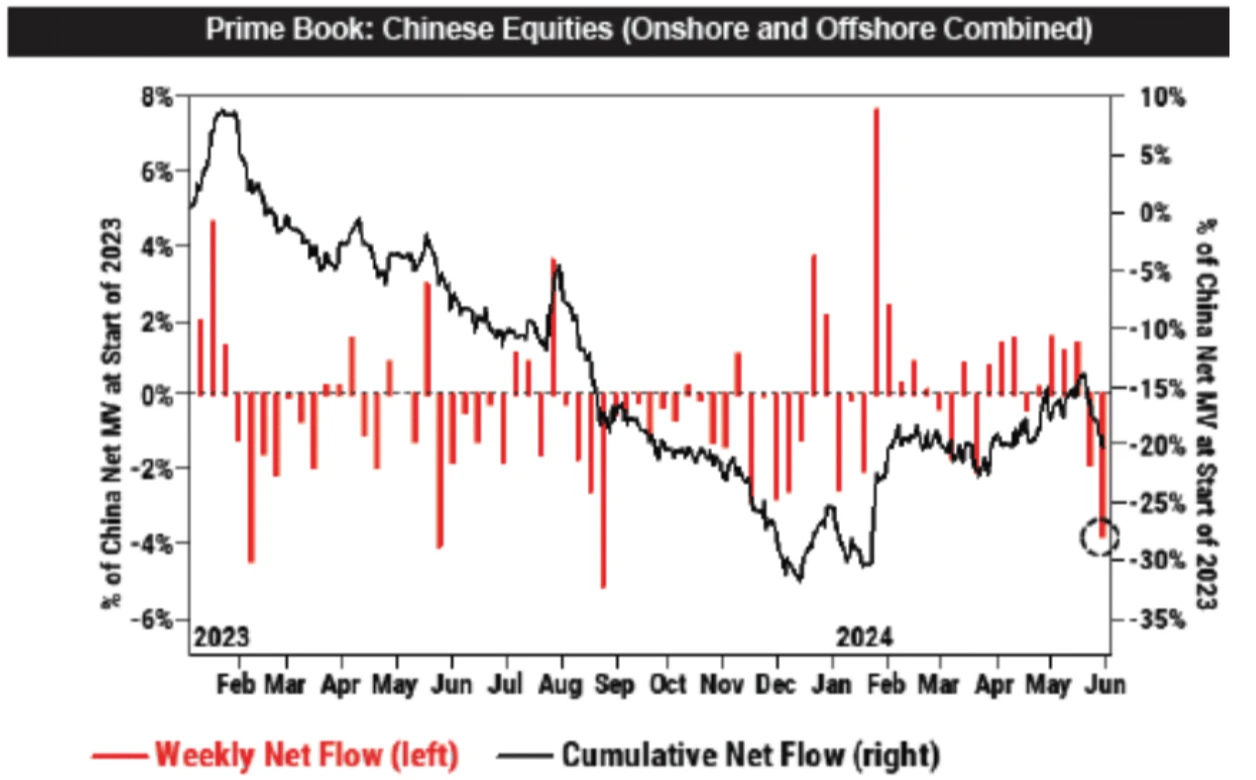

Chinese stocks: Hedge funds accelerated selling this week, at the fastest pace since August 2023.

Trump was found guilty

Trump suddenly became the first former president of the United States to be convicted, but there is no clause in the U.S. Constitution prohibiting him from continuing to run for election and serving as president of the United States. Since there are many ways to delay, including bail and pardon, if Trump is elected president, he will almost certainly be exempt from detention during his term. The main event for which Trump was prosecuted this time was that he paid hush money to two female friends on the eve of the 2016 presidential election. Trumps former personal lawyer, who was also his former confidant (now they broke up), paid $130,000 in hush money himself. It was fine, but Trump was reluctant to take it out of his own pocket, and instead used the money from the company under his name, which involved financial fraud and tax issues.

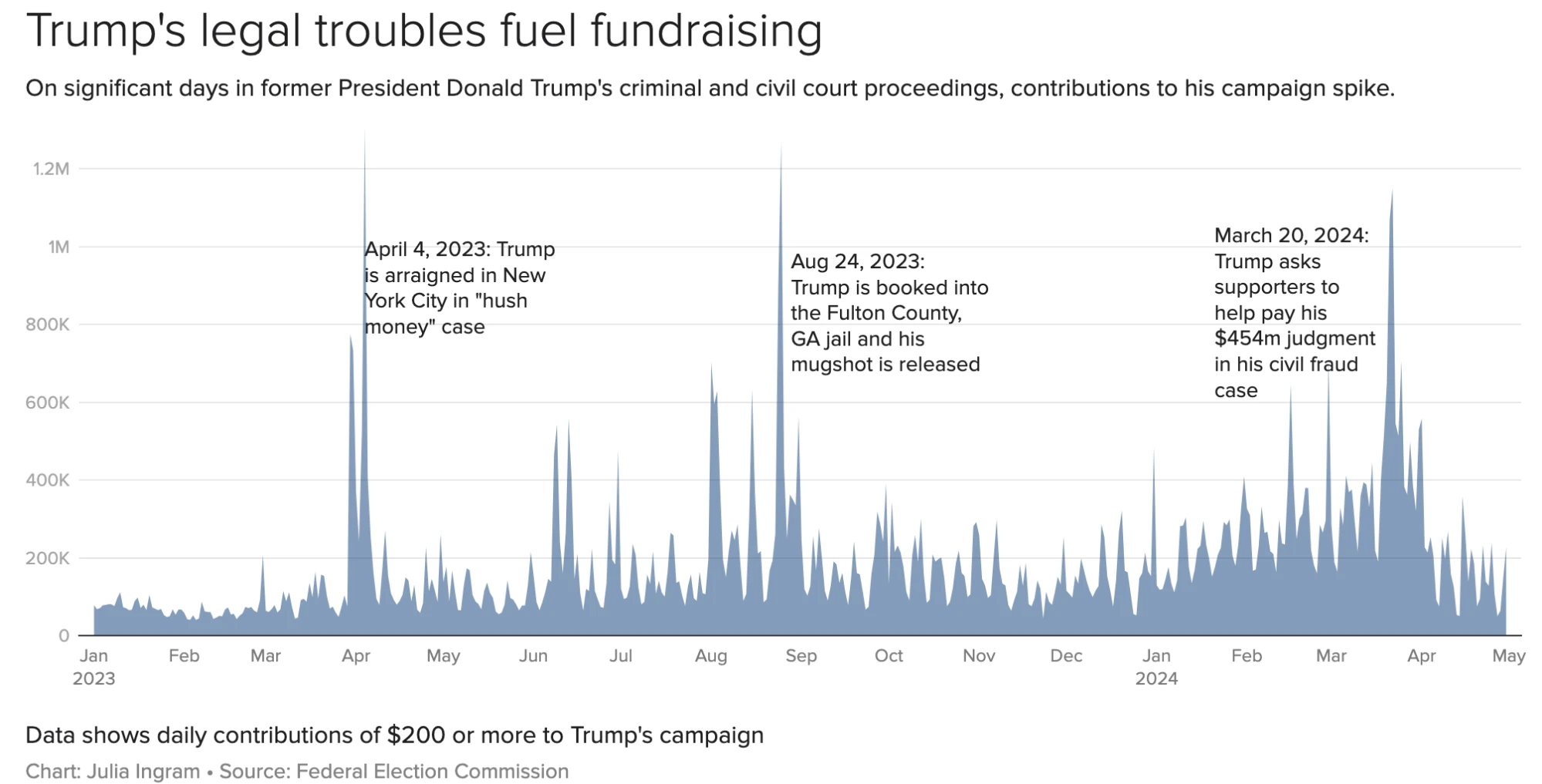

Interestingly, Trump has a campaign donation system, and every time he is suspected of committing a crime, donations will soar. Half a month ago, Trump announced that he might be arrested, and then the daily fundraising income increased significantly. After the verdict of the hush money case, he raised about 53 million US dollars through small donations on the website, and the donation website crashed due to too many visits. So the verdict may not only fail to suppress Trumps public support, but will make more people think that this is a political persecution by the Democratic Party to interfere in the election, thereby stimulating support for Trump. Since Trump has recently turned to actively win over cryptocurrency supporters, this may be a good thing for the cryptocurrency circle.

Judging from the secondary market pricing, Trumps chances of winning dropped briefly after he was found guilty, but soon reached a new high:

It should be noted that when the hush money incident that was sentenced this time occurred, Trump was not yet president and had little connection with the party. In addition, Trump is experienced in facing this kind of lawsuit. In the past 50 years, he has dealt with more than 4,000 lawsuits. The real danger is the other three. One is in the 2020 election in Georgia. Trump wanted to modify the vote count in this state. As a result, he called Secretary of State Zhou and asked him to find enough extra votes to reverse the election. As a result, the call was recorded. One is that Trump brought secret documents home, and the other is the attack on the US Congress on January 6. If these charges are proven, it is really possible that Trump will wear prison clothes.

This week’s highlights

After maintaining high interest rates for 22 consecutive months, the much-anticipated ECB rate cut cycle has finally arrived. At the monetary policy meeting on June 6, the ECB will fire the first shot of interest rate cuts among major central banks. According to the survey, economists believe that the ECB will 100% cut interest rates by 25 basis points on the day of the monetary policy meeting. This may be a positive for risky assets.

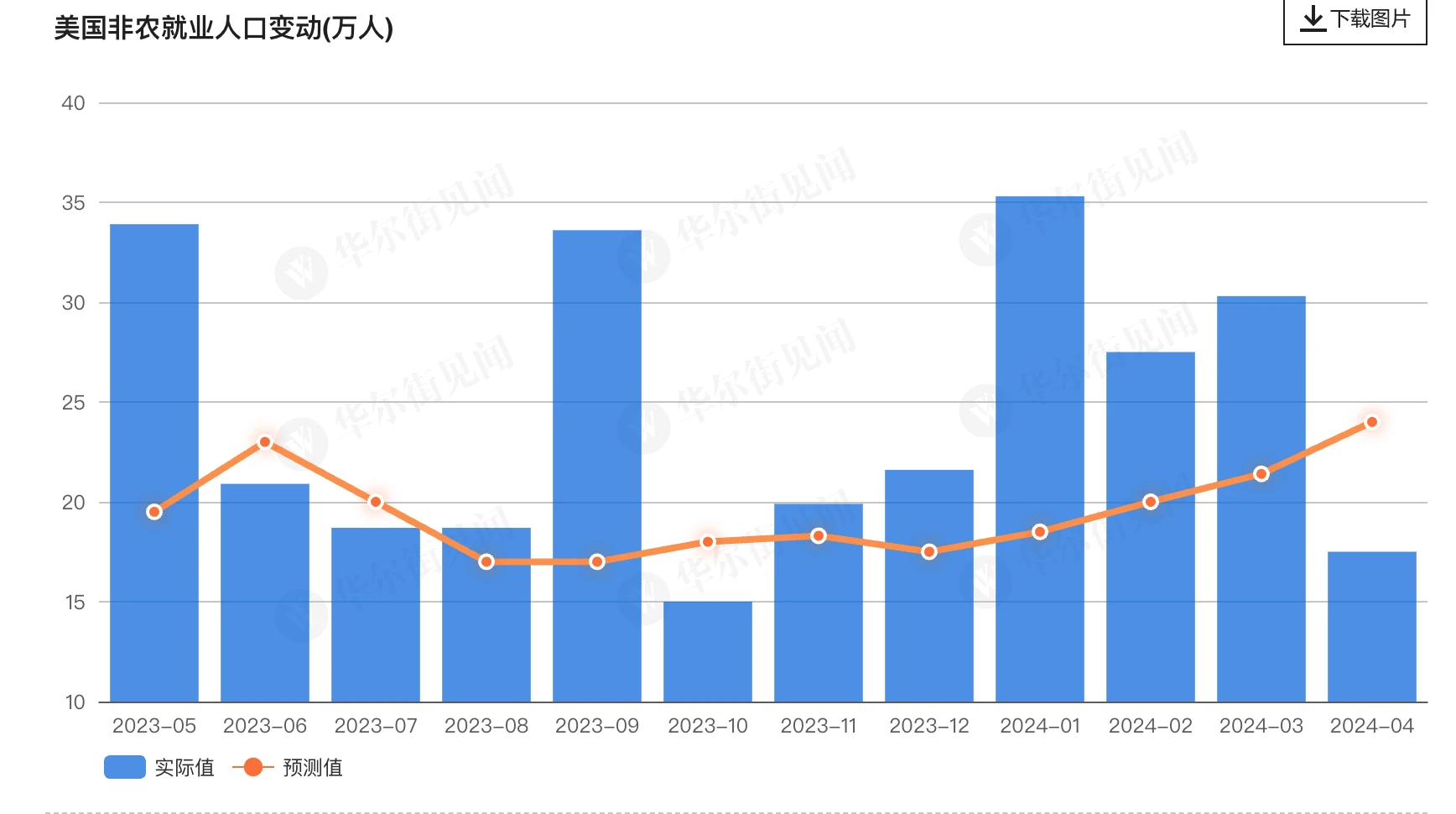

Recent forward-looking indicators point to further weakening in the labor market. For example, the number of people applying for unemployment benefits has been on an upward trend, with the four-week average of initial claims rising to 222,500, the highest level in eight months.

The history of economic cycles shows that this process will not be smooth and continuous. At some point, nonlinear phenomena will occur, and companies will save labor by directly laying off employees rather than slowing down recruitment. The market expects that the US non-farm payroll data for May, which will be released on Friday, will confirm this trend. It is expected to increase by only 180,000 (in April, the market was extremely optimistic that employment would increase by 240,000, but it only increased by 175,000, resulting in the first time in six months that the published value was lower than expected. BTC rose 6.5% on the same day), the unemployment rate stabilized at 3.9%, and the average hourly wage was expected to rise slightly from 0.2% to 0.3% month-on-month. Since expectations have been lowered, another weaker-than-expected performance may also trigger a market rally. If the unemployment rate rises, the impact will be greater than the number of employed people. As long as it rises by 0.1 percentage points, even if the number of employed people slightly exceeds expectations, it may trigger a market rally, although the current lack of momentum may make the continuation of the increase weaker.