4 Alpha Views

1. Current market trading logic: Recession expectations dominate, stagflation risks loom

Interest rate market signals: 2-year Treasury yields fell rapidly, the spread with SOFR widened, and the 10-year yield fell below the SOFR rate, reflecting that the market is pricing in an economic slowdown in advance → the Federal Reserve was forced to cut interest rates. At the same time, the inverted long-term interest rate (10-year < SOFR) strengthened the recession warning.

Liquidity contradiction: Although the consumption of TGA accounts has promoted marginal improvement in USD liquidity, the markets risk aversion has caused funds to withdraw from high-risk assets (US stocks, cryptocurrencies) and pour into the Treasury market, forming a paradox of loose liquidity but shrinking risk appetite.

2. The root cause of risk asset volatility: weak economic data + policy uncertainty

Economic cracks: The consumer confidence index plummeted, the job market cooled, and Trumps tariff threats intensified market concerns about a hard landing.

The AI narrative is shaken: the controversy over the invalidation of the Scaling Law after Nvidias financial report and OpenAIs technological iteration have caused the market to question the feasibility of AI commercialization, and technology stocks (especially the computing power sector) have been sold off.

Chain reaction in the crypto market: The backwardation structure of CME futures weakened the attractiveness of arbitrage, and coupled with the outflow of ETF funds, Bitcoin and U.S. stocks fell simultaneously, and the Greed Fear Index entered an extreme panic range.

3. Key game points next week: Non-agricultural data sets the tone for the strength of the recession trade

Data focus: If non-farm employment continues to exceed expectations in February, or the ISM manufacturing PMI continues to fall, it will strengthen recession pricing, push U.S. Treasury yields further downward, and put pressure on risky assets; conversely, data exceeding expectations may temporarily repair expectations of a soft landing.

Policy risks: Details of Trump’s tariffs and statements by Federal Reserve officials (especially revisions to the path of interest rate cuts) may trigger sharp market fluctuations.

Strategic advice: Focus on defense and wait for opportunities to counterattack. The short-term selling pressure in the crypto industry is due to the withdrawal of leveraged funds, but regulatory relaxation and technological innovation still support long-term growth space.

Stagflation or recession, what is the market trading?

1. Macroeconomic Review of This Week

1. Liquidity and interest rate changes

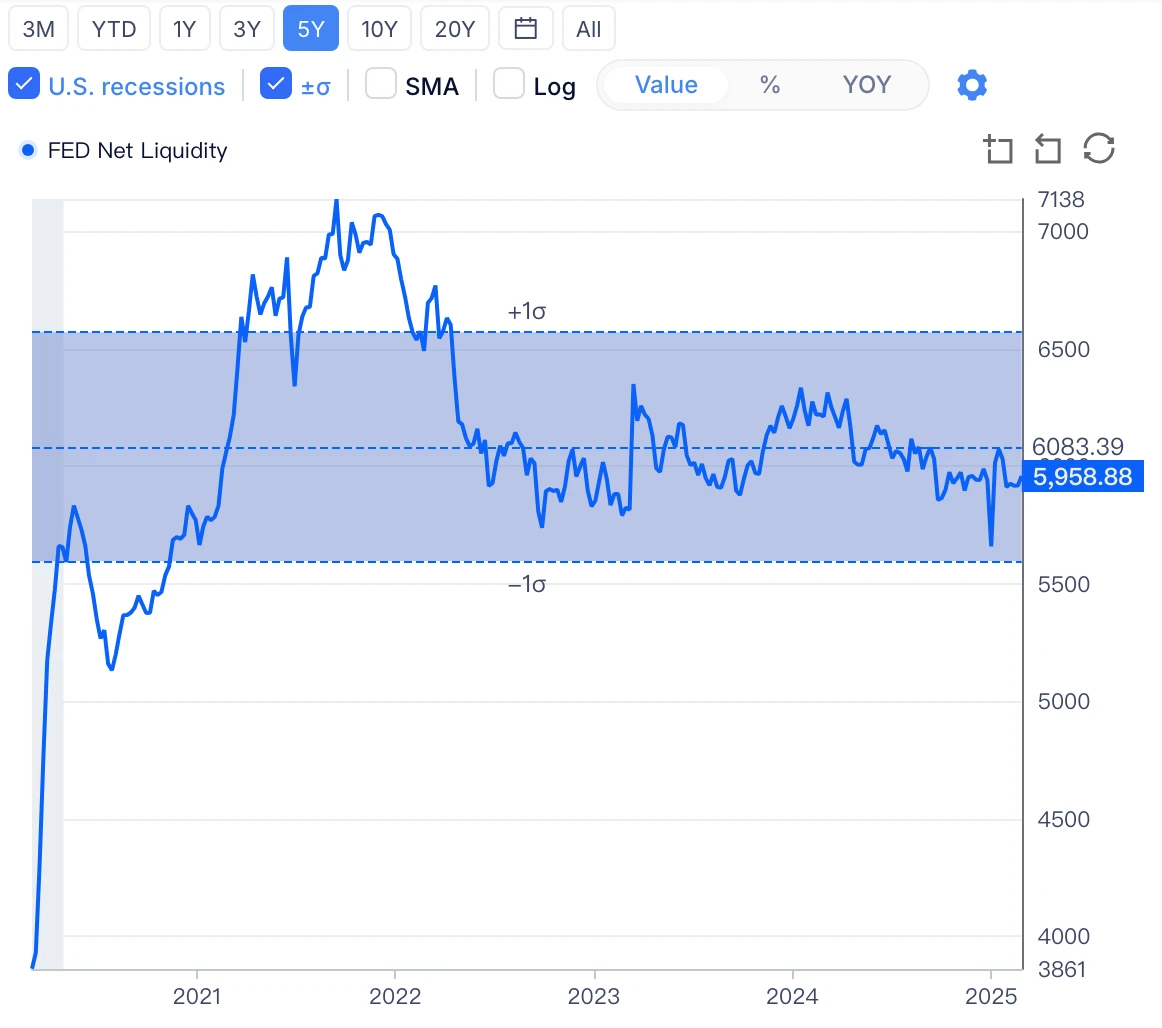

The marginal improvement in liquidity may be mainly due to the consumption of the Treasurys TGA account. While the US debt ceiling discussion has not yet been released, the marginal improvement of the US dollar basic liquidity this week is slightly increased by $39 billion compared with last week, but it is still in a tight state compared with the same period last year. Further analysis shows that the consumption of the US Treasurys TGA account has accelerated, and has dropped from $800 billion in mid-February to the current $530 billion+.

Figure 1: Changes in USD Base Liquidity Source: Gurufocus

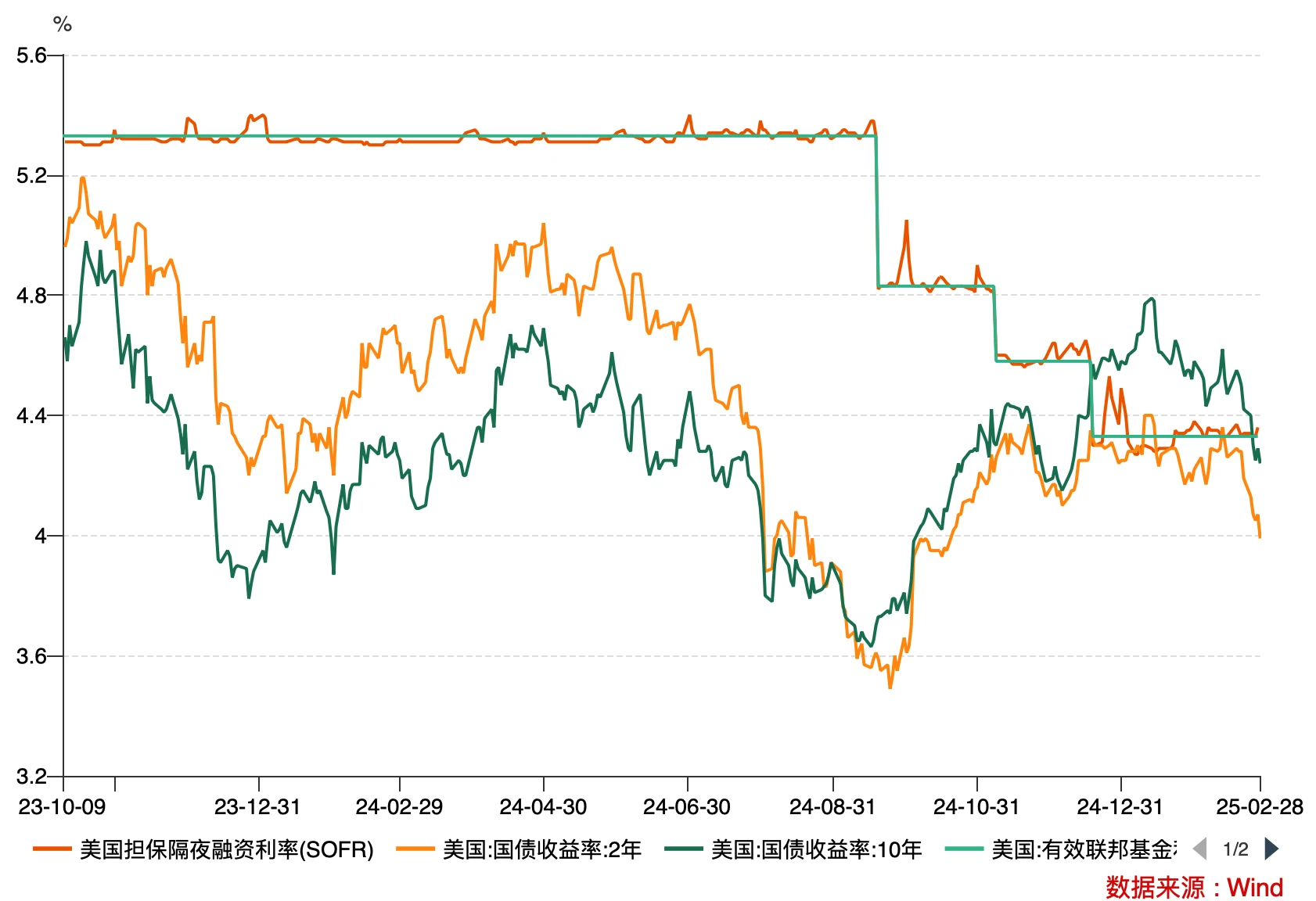

The interest rate market began to price in rate cuts, and long-term Treasury yields priced in an economic slowdown . From the data, over the past period of time, the 2-year Treasury yield, which measures the implicit interest rate path, and the SOFR, which measures the short-term financing rate, have not shown significant changes. However, since this week, due to the impact of economic data and Trumps tariffs, the 2-year Treasury yield has fallen rapidly and widened the spread with the short-term financing rate; at the same time, the 10-year Treasury yield has begun to be significantly lower than the SOFR rate.

Figure 2: Changes in short-term financing rates and government bond yields Source: Wind

The above trend is the result of global investors trading, which reflects several facts:

As economic data deteriorated, the Treasury markets expectations for the Feds rate cuts this year rose rapidly. Historically, when short-term financing costs are significantly higher than long-term interest rates, it basically means the end of the Feds tightening policy.

Short-term financing rates have not priced in a rate cut, indicating that the Federal Reserve is still managing liquidity through open market operations to ensure that short-term financing costs remain tight and to prevent the market from rushing to cut interest rates, thereby affecting inflation control.

The downward slope of the treasury bond yield is large, and the market is full of risk aversion. As shown in the chart, the downward slope of the 10-year treasury bond yield is significantly steeper this week, which shows that market funds are rapidly pouring into the treasury bond market and risk aversion is strong.

In general, although the Federal Reserve ensures the tightness of financing costs through liquidity management at the short-term interest rate level, the trading results of the Treasury market show that due to the influence of economic data, Trumps tariffs, inflation and other factors, the market is pricing in the Federal Reserve is forced to cut interest rates due to the economic slowdown.

2. Risk Market Review

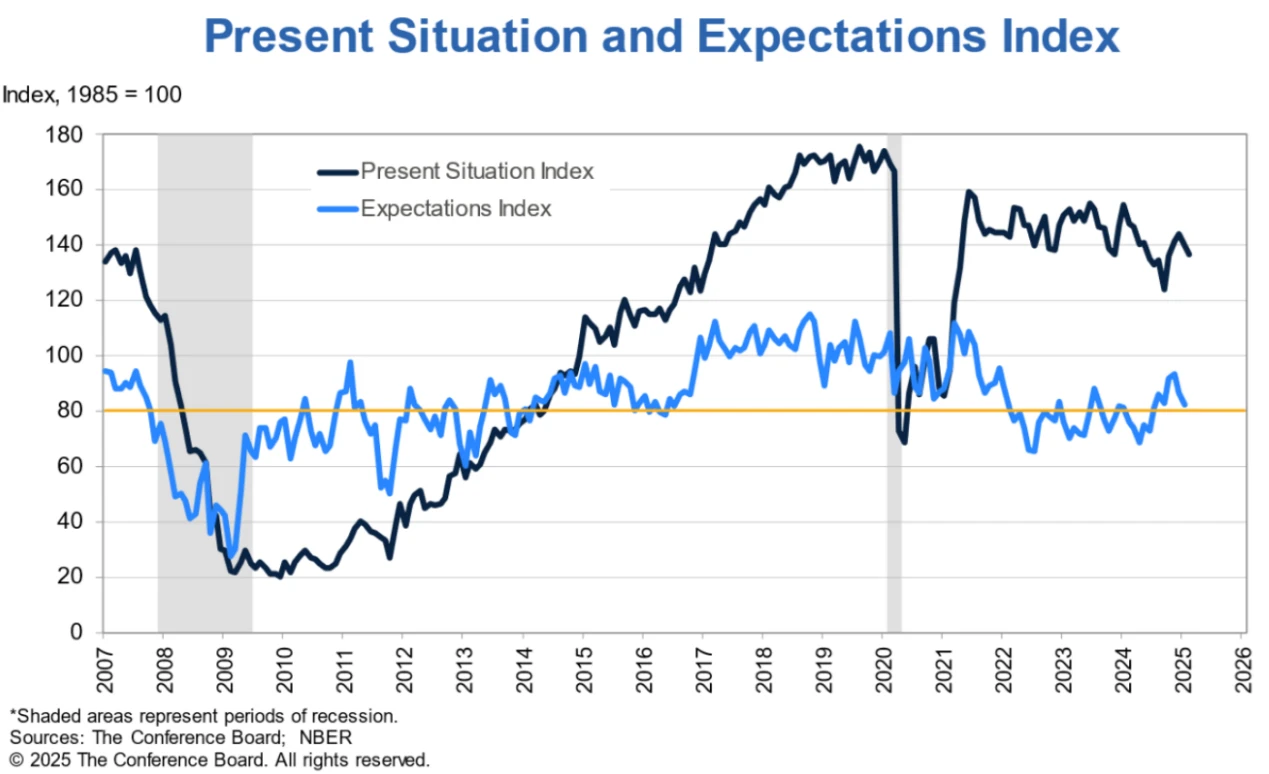

Looking at the U.S. stock market, the market fluctuated greatly this week. Driven by the poor data last week, the market sell-off continued this week, and the VIX index continued to fluctuate above 19. The market pricing of uncertainty became more pessimistic, and the markets attention began to gradually shift from inflation to economic data. In particular, the consumer confidence index released on Tuesday fell sharply, the largest drop in three years. Recession concerns once again shrouded the market, prompting more intense selling and short-selling activities until the release of PCE data on Friday, which eased market concerns and U.S. stocks closed on Friday with a rebound.

Figure 3: Business Council Consumer Confidence Index Source: NBER

Judging from the fluctuations in the U.S. stock market, in addition to the worsening signals given by economic data, the most important data last week was Nvidias financial report. Although the financial reports performance was impressive, the failure of the Scaling Law was once again magnified by the market, and the AI narrative faced a great test, especially after OpenAI launched ChatGpt 4.5. This concern seems to be becoming a reality. With the main line of AI in the market being questioned and economic data giving expectations of a slowdown, U.S. stocks are facing a comprehensive adjustment of expectations and market pricing.

From the perspective of the crypto market, this week can be described as a cloudy week. After the Bybit incident last week, as the risk appetite of the entire U.S. stock market deteriorated, market funds flowed to the treasury market for risk aversion. The entire crypto industry suffered a huge pullback, and the Greed Fear Index once fell below 15, entering an extreme panic zone.

As analyzed above, although the basic liquidity of the US dollar has eased marginally, when the market is pricing in interest rate cuts due to economic slowdown or even recession concerns, it does not have a significant boost to high-risk assets. Funds are more inclined to withdraw from high-risk assets and turn to the Treasury market with positive carry returns.

At the same time, if we further observe BTC, the price gap between the CME futures market and the spot market has narrowed rapidly, and even entered a backwardation structure. This structural change has basically lost its appeal to hedge funds that use spot ETFs + CME futures for basis arbitrage, compared with the 4% or more Treasury yield. This also explains to a certain extent why Bitcoin ETF funds have experienced a large outflow this week.

The entire transmission logic is: the market worries about economic recession - risk appetite declines - funds withdraw from high-risk markets - hedge funds begin to withdraw from Bitcoin basis trading - ETF funds outflow - exacerbate concerns in the crypto market - sell-offs accelerate. With the easing of PCE data on Friday, the market rebounded thanks to the recovery of risk appetite.

2. Outlook for next week

As analyzed in the previous article, the market is at a turning point where trading expectations are undergoing drastic adjustments. The gaming factors are too complex, which increases the difficulty for subjective trading investors. They need to closely track the latest data and adjust expectations in a timely manner.

The key macro data for next week are as follows:

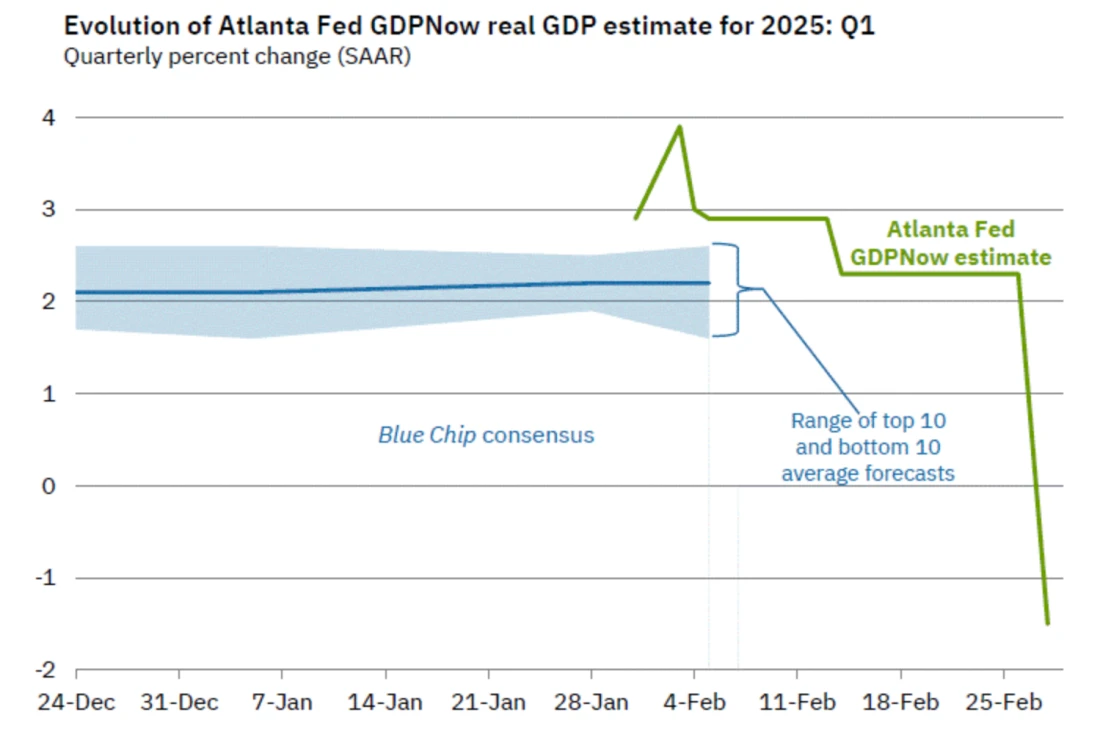

As the Atlanta Federal Reserve released its latest GDP NOW forecast data last Friday, the data rarely forecast the US GDP (seasonally adjusted) for the first quarter of 2025 to be -1.5%.

Although the deterioration of this forecast data is partly due to seasonal factors in US consumer spending, it does reflect that the risk of economic slowdown is increasing under the threat of Trumps tariff policy. The current market is in a critical period of adjustment of the dual expectations of recession expectations strengthened and Trump policy impact, and asset prices may still maintain high volatility. In particular, next weeks non-agricultural data is about to be released, which will determine whether the market will further strengthen the recession trade during the critical period of the game.

Based on the above factors, we recommend:

Out of a risk-prudent stance, we advise investors not to chase high prices unless market expectations are clear; but assuming that risk appetite stabilizes and recovers, the market may see short-term corrective movements, but volatility risks still need to be monitored.

The current market is highly uncertain. For defensive purposes, we recommend diversifying your portfolio as much as possible and adding defensive assets/quantitative arbitrage products to ensure a balance between risk and return.

Pay close attention to the market expectation adjustments brought about by economic data, macro interest rates, liquidity and policies

Although the decline last week dealt a heavy blow to market sentiment, investors need to pay attention to the fact that the relaxation of US policies and regulations has not stopped, which has brought long-term growth momentum and broad growth space to the crypto industry. The short-term decline in the market is a risk-averse action when the main trading line is unclear. Especially for leveraged funds/short-term funds mainly composed of hedge funds, the withdrawal of funds and liquidation of positions do not mean a pessimistic view on Bitcoin, but simply because market signals trigger their risk management measures.

In the long run, we always believe that Bitcoin and the crypto industry still have ample room for upside, and we remain confident in this.

Disclaimer

The content of this article is for information sharing only. It does not promote or endorse any business or investment behavior, nor is it financial advice. Readers are requested to strictly abide by the laws and regulations of their region and not participate in any illegal financial activities.

It does not provide trading portals, guidance, or distribution channel guidance for any virtual currency or digital collection-related issuance, trading, or financing. The above content is original to 4 Alpha. Any content is prohibited from being reproduced or copied without permission. Violators will be held accountable.