The information, opinions and judgments on markets, projects, currencies, etc. mentioned in this report are for reference only and do not constitute any investment advice.

The confusion and concerns caused by Trumps tariff war, coupled with the rebound in US inflation expectations, have reinforced the markets expectations that the US economy may be in stagflation or even recession. This is extremely bearish for high-risk assets.

This expectation hit the valuation of U.S. stocks, which had been at a high level for two consecutive years, and was then transmitted to the crypto market through the BTC ETF.

BTC short-term investors sold to lock in the maximum loss in this cycle, and preliminarily completed the latest pricing of BTC. Long-term investors once again changed from reducing holdings to increasing holdings and took over some of the selling orders, bringing the price to a new balance around US$82,000. However, the market is still fragile, and the floating losses of short-term investors are still at a high level. If the US stock market is in chaos and BTC ETF funds are sold, short-term investors will inevitably participate in the selling, and the price will inevitably be adjusted downward.

At present, the moderate adjustment of the US stock market has been basically completed, but the further trend still depends on the extent of the explosion of the tariff war trigger point on April 2, and whether the employment data in March will show a sharp decline. If both deteriorate beyond expectations, it will still be priced downward.

As the chaos fell out, both the US stock market and BTC saw a sharp decline, and the sell-off and panic were also released to a considerable extent.

We believe that as the negative effects of the tariff war are gradually exhausted and the Federal Reserve gradually restarts its interest rate cuts, it is highly likely that BTC will reverse in the second quarter.

Macro-finance: Economic and employment data boost expectations of stagflation and even recession, and US stocks break down

After the Trump 2.0 Trade was extinguished, the U.S. stock market basically returned to the starting point of November 6, 2024, the day Trump won the election. The new trading judgment framework was initially established at the end of February, and the entire month of March was based on the output of the judgment framework after the various economic, employment and interest rate data that were continuously released were input into it.

This judgment framework is the game between the possibility of economic stagflation or even economic recession that may be caused by Trumps tariff policy and the choice of whether the Federal Reserves monetary policy should prioritize employment or reduce inflation.

On Friday, March 7, the U.S. Bureau of Labor Statistics first released the February employment data: Non-farm employment increased by 151,000 in February, lower than the market expectation of 170,000, indicating that employment growth slowed down, but remained relatively solid. The unemployment rate rose to 4.1% from 4.0% in January, indicating that the labor market was slightly loose. Average hourly wages increased by 0.3% month-on-month and 4.0% year-on-year, which was higher than the inflation rate, indicating that real wages have improved, but it may put pressure on inflation.

This acceptable employment data partially dispelled concerns that the economy had already begun to decline, and the US stock market fell first and then rose. However, concerns still exist, as the employment data is lower than expected and the unemployment rate is also rebounding.

On March 12, the U.S. Department of Labor released CPI data: The overall consumer price index in February increased by 0.2% month-on-month and 2.8% year-on-year, a slight decrease from 3.0% in January. The core CPI (excluding food and energy) increased by 0.2% month-on-month and 3.1% year-on-year, indicating that inflation has eased, but core inflation is still higher than the Feds 2% target.

The PCE data, which the Federal Reserve pays more attention to, was released on the 28th and showed that the overall personal consumption expenditure price index increased by 0.3% month-on-month and 2.5% year-on-year in February; the core PCE increased by 0.4% month-on-month and 2.8% year-on-year, reflecting that the downward path of inflation has been blocked and the core indicators have strong stickiness.

PCE data showed that the overall personal consumption expenditure price index increased by 0.3% month-on-month and 2.5% year-on-year in February, higher than 2.5% in January; the core PCE increased by 0.4% month-on-month and 2.79% year-on-year, higher than 2.66% in January.

Although the magnitude is small, both CPI and PCE show that price growth has begun to rebound, which means that the Federal Reserves goal of lowering inflation is facing severe challenges.

On the 18th and 19th, after a two-day interest rate meeting, the Federal Reserve announced that it would maintain the federal funds rate at 4.25-4.50%, pausing the interest rate cut for the second time in a row. The statement pointed out that economic activity has expanded steadily and the labor market is solid, but inflation is still slightly high, especially under the influence of Trumps policies, the uncertainty of the economic outlook has increased. This is the first time that the Federal Reserve has clearly stated that tariff policies may affect the economic downturn, but the risk of recession has increased, but it is not high.

Powell, chairman of the Federal Reserve, said that inflation may be delayed in returning to the 2% target due to policies such as tariffs, and hinted that interest rates will be cut if the job market deteriorates. As a preemptive measure to deal with the impact of tariffs, the Federal Reserve slowed down the reduction of U.S. Treasury holdings from $25 billion per month to $5 billion per month.

The Feds relatively dovish statement boosted the market, driving a sharp rebound in the three major stock indexes. By the end of the month, the CME Fed Watch dashboard showed that the market had raised its expectations for interest rate cuts in 2025 to three for the first time. Goldman Sachs also expects three interest rate cuts this year.

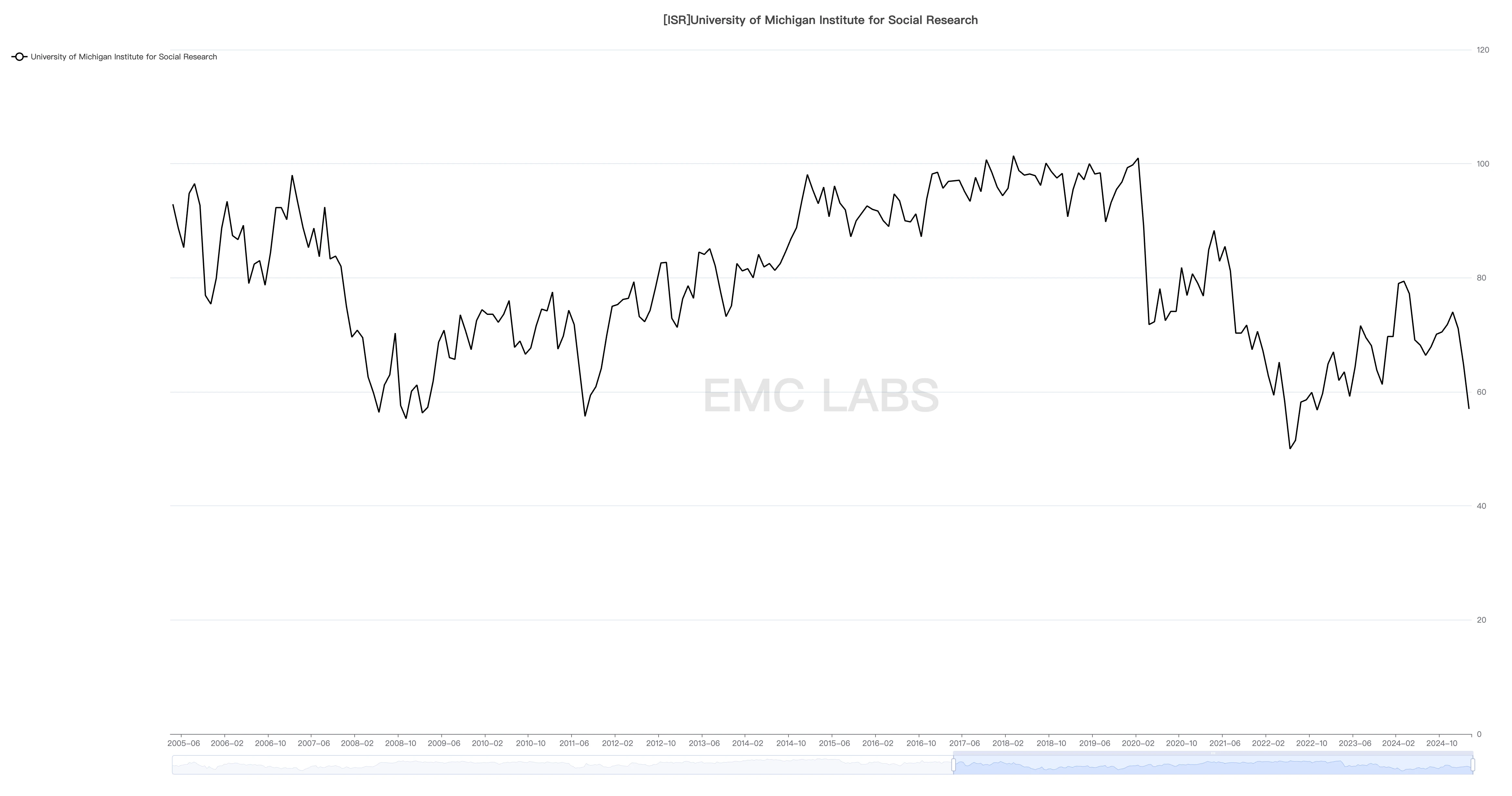

On Friday, the 28th, the University of Michigan released the final value of the Consumer Confidence Index for March, which fell from 64.7 in February to 57, a drop from the initial value of 57.9 and lower than the median estimate of economists surveyed. Consumers expect the annual inflation rate to be 4.1% in the next 5 to 10 years, the highest since February 1993, up from the initial value of 3.9%. The expectation for inflation in the next year is 5%, the highest level since 2022.

The University of Michigan Consumer Confidence Index is a subjective data, but it fully reflects the decline in the confidence of end consumers. On the same day, the GDPNow model of the Federal Reserve Bank of Atlanta showed that the forecast value of the real GDP growth rate in the first quarter of the United States as of the 28th was -2.8%. This value resonates with the University of Michigan Consumer Confidence Index. As in February, the three major stock indexes responded with a sharp decline, and the VIX index rose by 11.9% in a single day.

University of Michigan Consumer Sentiment Index

Trumps tariff policy has also been going back and forth many times this month. As of the end of March, tariffs on Canada, Mexico, China and steel and aluminum products have been implemented.

The United States imposed a 25% tariff on all imported vehicles, covering vehicle types such as passenger cars and light trucks, starting April 2. A 25% tariff will also be imposed on core auto parts (such as engines, transmissions, electrical systems), effective no later than May 3.

What remains undecided is the imposition of “reciprocal tariffs” on major trade deficit countries, and the specific list will be released on April 2. April 2 is currently regarded by the market as the day of greatest concern in the tariff war.

Amid concerns about tariff uncertainty, economic stagflation and even recession, funds continued to withdraw from the equity market in March, causing the Nasdaq, SP 500 and Dow Jones to fall 8.21%, 5.75% and 4.20%, respectively, falling below or nearly falling below the 250-day moving average, achieving a moderate technical adjustment.

Safe-haven funds poured into U.S. Treasuries, pushing the 2-year Treasury yield down 1.15% in a single month. The 10-year Treasury yield fell 0.45%, but combined with inflation expectations, long-term funds expectations for long-term economic growth have fallen to a negative growth level.

Gold, another safe-haven asset of mainstream funds, has been favored. This month, London gold officially broke through the 3,000 yuan mark, with a monthly increase of 8.51% to US$3,123.97 per ounce.

Consumer confidence is low, inflation expectations are rising, and people are pessimistic about US economic growth. They are even worried that the uncontrolled and volatile tariff war will push the US economy into stagflation and recession. EMC Labs believes that the uncertainty of Trumps tariffs is the biggest variable, which is driving the deterioration of the US economy and consumer confidence, and in turn driving the market to trade in stagflation and recession. With Powells relatively dovish speech, the market began to bet on the Feds intervention in cutting interest rates in June, and as US stocks fell, the number of interest rate cuts also increased from two to three. The problem of inflation may be temporarily shelved, but it has not disappeared. Instead, it will intensify with the tariff war. The impact of the tariff war will not be seen until it is settled.

Crypto assets: Running in a downward channel, extreme market conditions may fall to $73,000

Traders worries and fears dominated the turmoil in the capital market in March. Due to the sharp drop in late February, BTC remained relatively stable in March, but the rebound was weak, and it ultimately recorded a monthly decline of 2.09%.

In February, BTC opened at $84,297.74 and closed at $82,534.32, with a high of 95,128.88 and a low of 76,555.00, an amplitude of 22.03%, and a slightly larger trading volume than the previous month.

In terms of time, after a sharp drop at the end of February, BTC rebounded in the second and third weeks of March, but the rebound was weak, with the highest increase from the low point only 16%. In the following week, with the frequent chaos of US tariff policies and the decline of inflation data, especially consumer confidence data, BTC fluctuated downward with the US stock market and finally recorded a monthly decline.

Technically, the whole month was within the downward channel since February, and below the first upward trend line of this cycle. And since the sell-off at the beginning of the month, trading enthusiasm has dropped sharply, and trading volume has declined week by week. Most of the time, it was below the 200-day line, and on March 11, it briefly touched the 365-day line.

Although there was an outflow of BTC from centralized exchanges throughout the month and a small amount of funds flowed into the BTC ETF channel, BTC, as a high-risk asset, still found it difficult to attract buying power amid the turbulent U.S. stock market.

At the policy level, there are many positive factors this month.

On March 6, US President Trump signed an executive order to formally establish the Strategic Bitcoin Reserve (SBR), which included approximately 200,000 BTC previously confiscated by the federal government into the reserve, and made it clear that these assets would not be sold in the next four years. At the same time, the order also proposed the establishment of a reserve pool composed of digital assets other than Bitcoin, aiming to enhance the United States position in the global financial system through diversified assets. This is the first time that Bitcoin has been managed as a permanent national asset by the US government, marking the establishment of its status as digital gold. Although the executive order is not legislation, it lays the foundation for subsequent policies.

On March 7, the day after Trump signed the executive order, he convened the White House Crypto Summit, inviting many industry professionals and investors to discuss crypto industry regulation, reserve policies, and future development directions. The summit further released the signal that the US government supports crypto innovation.

On March 29, the U.S. Federal Deposit Insurance Corporation (FDIC) issued guidelines to clarify the compliance procedures for banks to participate in cryptocurrency-related activities. This provides a clear path for traditional financial institutions to integrate into the crypto market and helps banks to engage in crypto asset services.

On the same day, Trump pardoned the three co-founders of the cryptocurrency exchange BitMEX.

At the state level, on March 6, Texas proposed to establish a state-level strategic reserve of Bitcoin, and has entered the notice of intent stage of the legislative process. Usually, this step indicates that the bill is likely to pass. On March 31, the California State Assembly formally submitted the Bitcoin Rights and Interests Act to clarify the legal rights and usage regulations of Bitcoin in the state.

All of the above indicate that BTC and crypto assets are being effectively implemented in the United States. These policies and regulations will take time to take effect, but they are undoubtedly clearing the way for the United States to build a crypto capital in the future.

However, concerns about stagflation and inflation dominated the market, and risk-averse and valuation-killing traders chose to ignore these long-term positives, leading to a short-term decline in BTC prices.

Perhaps due to long-term favorable support, BTC is still in a strong trend compared to the US stock market, which has returned to the level on November 6. The closing price this month is $82,378.98, which is still higher than $70,553 on November 5.

Considering the lack of liquidity, if the tariffs exceed expectations or worse employment and economic data are released, BTC may give up all the gains of the Trump deal and fall to $70,000-73,000. But this will only happen if the tariffs or employment data deteriorate far beyond expectations. If the US stock market can gradually stabilize on April 2 after the negative impact of the tariffs on Liberation Day is fully released, the previous $76,000 may become the low point of this round of sell-offs.

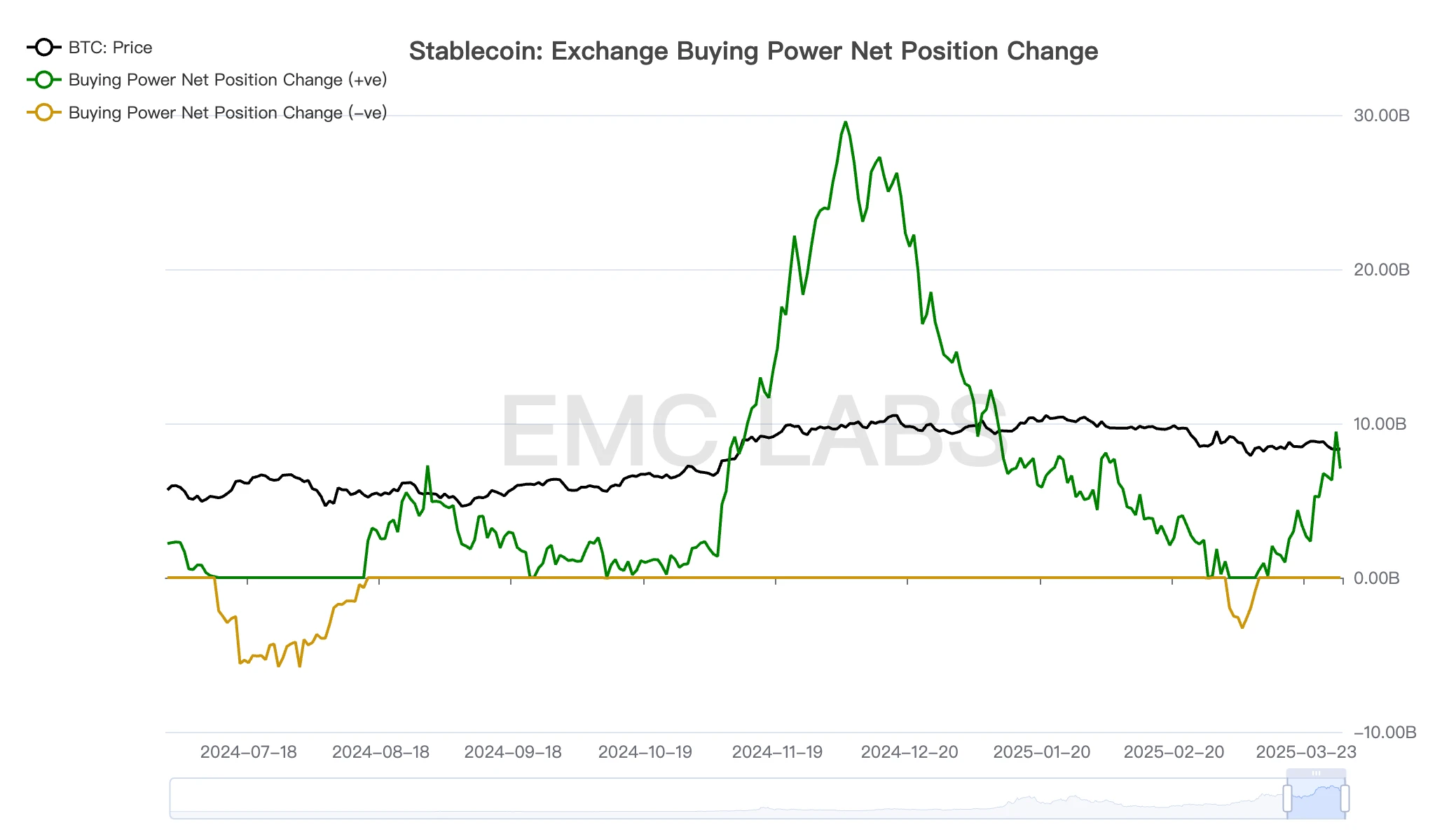

Funding: BTC Spot ETF outflows slowed, stablecoins continued to flow in

In the February report , we mentioned that the selling force of this round of adjustments came from the BTC Spot ETF. Last month, its selling reached 3.249 billion, setting a record for the largest monthly outflow since its establishment. This month, the ETF channel funds continued to outflow as a whole, but the scale was greatly reduced to 634 million US dollars. The outflow mainly came from early March, and after mid-March, it ushered in inflows for 10 consecutive trading days.

Crypto market capital inflow and outflow statistics (monthly)

Stablecoins continued to see inflows of $4.893 billion this month, slightly lower than last months $5.3 billion.

The inflow and outflow of funds in the ETF channel are completely synchronized with the rise and fall of BTC prices, which can serve as evidence that this round of adjustments comes from the chain effect of the adjustment of US stocks.

The funds in the market did not behave independently, but instead reacted following the market, both in the decline from late February to early March and in the subsequent rebound.

Changes in BTC purchasing power on centralized exchanges

BTC prices will continue to be linked to US stocks, especially the Nasdaq, so the US tariff war and the Feds decision to cut interest rates will continue to affect the medium- and long-term trend. The scale and sustainability of ETF channel funds inflows will become an observation tool for judging medium- and short-term trends.

Second sell-off paused: chips return to long hands to cool down, short hands continue to be under pressure

Before the February adjustment, the main event in the crypto market was the second wave of selling by the long-term group. This selling was both a response to the flood of liquidity and objectively suppressed the rise in BTC prices. Since then, with the change in the trading theme of US stocks, both US stocks and BTC valuations have faced downward pressure, and the short-term group has begun to sell for risk aversion.

With the sharp drop in US stocks, the internal structure of the crypto market has suffered a huge impact and made corresponding adjustments. When short-term selling increased and prices fell rapidly, the long-term group stopped selling around mid-February and turned to increasing holdings, which greatly reduced the downward pressure on the market and reduced the heat of chips, helping the market cope with the decline in liquidity and allowing prices to reach a new balance after the decline.

Statistics of long and short positions and miners group holdings

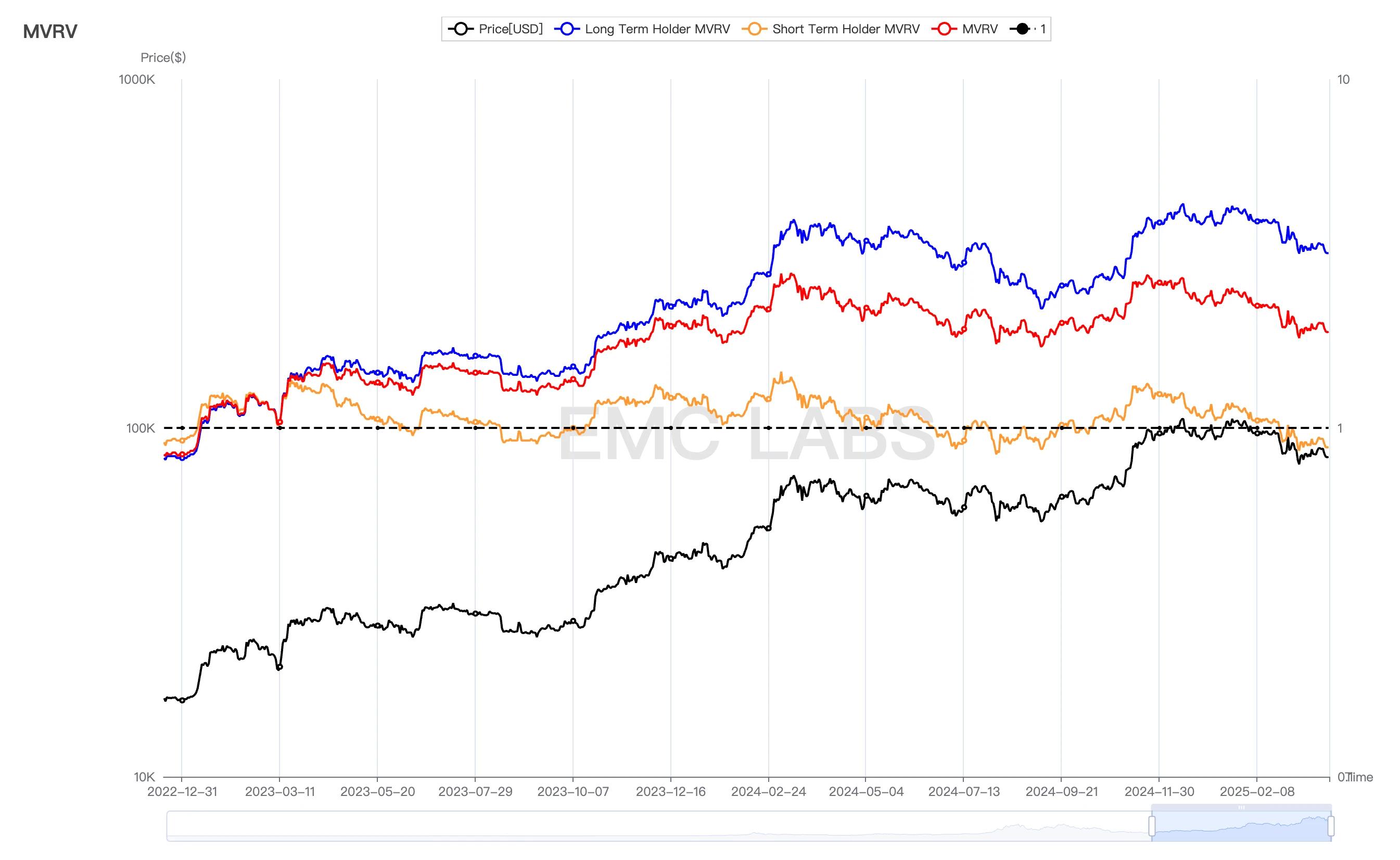

According to eMerge Engine data, the extent of the losses caused by this round of decline has exceeded the losses caused by the Carry Trade storm in 2024, becoming the largest loss range in the new cycle since January 2023. On the chain, a large number of BTC originally priced in the range of US$90,000 to US$110,000 have entered the range of US$76,000 to US$90,000, which partially solves the problem of insufficient allocation of chips from US$73,000 to US$90,000.

BTC chip distribution on the chain

In this round of rapid decline, although long-term investors also took profit-taking actions, the scale was not large. The chips that changed hands in the panic mainly came from BTC traded in the range of US$90,000 to US$110,000 after November last year.

Although the short-hand group has completed a considerable amount of selling, the current floating profit and loss of the entire chain is still not optimistic. The maximum floating loss of the short-hand group in this round of decline reached 14%, close to 16% on August 5, 2024. As of March 31, the short-hand group still had a floating loss of 12%, and the patience and tolerance of this group are still facing great challenges.

Statistics of floating profits and losses of different BTC holders

If this pressure is converted into selling pressure, it may push BTC down to $73,000, which is the upper edge of the new high consolidation zone and the price before Trump was elected.

Conclusion

From an external perspective, the current BTC price is completely subject to the game between expectations of economic stagflation or even recession caused by tariff chaos and inflation stickiness, and whether the Federal Reserve will compromise and cut interest rates.

From the perspective of internal factors, short-term investors have experienced the largest selling losses in this cycle in the past month. The selling pressure has shrunk, but the floating loss pressure is still large. It is not ruled out that they will continue to sell to alleviate the pain, but the probability is small. The turn from selling to increasing of long-term investors has played a great stabilizing role in the market.

Stablecoins continue to flow in, and there are signs of inflows into the BTC ETF channel. However, if the US stock market falls, ETF channel funds may sell off again, which will become the active force driving prices down.

On April 2, Trumps tariff war will reach a peak, and the US stock market may reach a short- to medium-term bottom. If the tariff policy does not deteriorate too much, the US economy shows signs of recession but not serious, and the Fed cuts interest rates again in June, BTC, which has already experienced a sharp drop in valuation, will likely turn around in Q2.

After the storm in the first quarter, the outlook for the second quarter is still not clear enough, but the most painful moment may have passed. When Washington and the Federal Reserve return to a rational state of game, the market should be able to return to its own operating rules.

EMC Labs

EMC Labs was founded by crypto asset investors and data scientists in April 2023. It focuses on blockchain industry research and Crypto secondary market investment, takes industry foresight, insight and data mining as its core competitiveness, and is committed to participating in the booming blockchain industry through research and investment, and promoting blockchain and crypto assets to bring benefits to mankind.

For more information, please visit: https://www.emc.fund