Original author: Paolo@Victory Securities Partner, Andy@VDX Senior Researcher

Original source: VWin Ventures

TLDR:

Stablecoin is the value mapping of its underlying fiat currency on the blockchain and is the transaction medium linking fiat currency and crypto assets.

The core scenarios of stablecoins are divided into transactions and payments, which are used for permissionless transaction settlement of financial assets and commodity trade on the global flat blockchain clearing and settlement network.

Trading scenarios: The top players are concentrated, and future growth will come from the listing of new financial assets on the chain. The competitive landscape of stablecoins has gradually evolved from competition in on-chain/exchange trading scenarios to market competition for the listing of traditional financial transactions on the chain.

Payment scenario: Payment is the largest incremental market for stablecoins, especially cross-border remittances and local acceptances, which have real and huge demand. Stablecoins are eroding the core interest chain of traditional clearing systems represented by SWIFT and card organizations. Licensed financial institutions provide customers with compliant and stable trading venues.

The leading stablecoin players USDT and USDC rose to prominence by relying on early channel and traffic binding, and later competed on liquidity and ecological network. Tether relied on the distributed network of black and gray industries to expand naturally in the early stage, and Circle relied on its compliance identity to expand mainstream financial channels.

The US dollar stablecoin essentially carries the de-geographical output of a new round of financial sovereignty of the US dollar, establishes a US dollar network that can circulate globally without going through traditional banks and central banks, and promotes the free flow of funds and the concentration of assets. The United States can remotely control the flow of US dollars on the global chain through regulatory policies and KYC reviews, forming a new digital colonial model.

The underlying logic of stablecoins – Shadow dollars on the global new clearing and settlement network

Stablecoins initially solved the problem of value stability in the digital asset world, but in essence, they meet the global demand for a de-banked dollar. This digital dollar can flow freely 24 hours a day, 7 days a week, without being restricted by the banking and central bank systems, and quickly occupy the gray area that banks cannot reach.

By tacitly allowing private institutions to issue stablecoins, the United States extends the dollar to areas that are difficult to cover with traditional supervision, forming a decentralized but essentially controllable dollar digital colonial system.

Stablecoins are a business of converting credit into liquidity. To make stablecoins means to become a private global central bank with extremely low deposit absorption costs and marginal expansion costs, and to master the two-way payment of fees, interest on capital deposits, and some underwater multiple profit models. In the entire Crypto industry, stablecoins can be called casino chips and mining shovels, serving gray needs such as speculative arbitrage and leveraged trading; stablecoins are one of the very few core businesses in the Crypto industry with real long-term value.

The core scenario of stablecoins – permissionless transaction settlement of financial assets and commodity trade

The current total issuance scale of stablecoins exceeds US$200 billion, which is mainly divided into two core scenarios: transactions vs. payments.

Scenario 1: Trading market (stock dominated, strong flywheel effect)

In terms of trading scenarios, stablecoins, as safe-haven assets and trading media, have tended to be concentrated in the top. USDT/USDC has a deep moat and obvious network effects:

Existing market: At present, there is a lack of high-quality assets on the chain to further attract liquidity, the growth of stablecoins in trading scenarios is hindered, and competition is fierce;

Incremental direction: The future growth point lies in the on-chain of RWA (real world assets), which will gradually develop from standard products (such as bonds) to non-standard equity assets, forming new opportunities similar to Nasdaq on the chain;

Opportunities for new players: Seize new assets and new scenarios - Take FDUSD binding to Binance Exchange as an example, relying on specific vertical scenarios to build network barriers; or Ethena and Usual develop on-chain fixed-income wealth management products similar to Yuebao to seize the scenario-based entrance to users financial needs.

The future development of trading scenarios will gradually shift from simple trading tools to asset financialization and securities chain-based development. Players will compete in resource integration and scenario barrier construction.

Scenario 2: Payment market (the current largest source of stablecoin growth)

Compared with transaction scenarios, stablecoins in the payment field have greater potential, which comes from the stock conversion of the traditional payment market:

Cross-border payment demand: Especially in developing countries, where the traditional financial system is weak, stablecoins have obvious cost advantages and huge demand. Stablecoins have seriously impacted the monopoly position of the traditional banking system.

Core competitive factors in payment scenarios: In the stablecoin payment scenario, credit endorsement and liquidity support are the basis, and the core of competition lies in the establishment of channel networks. Although the business model is relatively homogeneous, in the early blue ocean market, by extending upstream and downstream, it is still possible to grab asset-side or traffic-side dividends to form a bilateral network effect.

Path play:

From top to bottom: Circle has obtained a global compliance license, using its official credit and first-mover advantage to encourage traditional financial institutions to accept USDC;

Bottom-up: Represented by USDT, it has grown wildly through local non-compliant financial institutions and OTC channels, quickly occupying market share, but there are long-term compliance risks.

Compared with stablecoin issuers (Issuers), channel distributors (such as payment companies, brokers, etc.) can also obtain market expansion and customer acquisition benefits, focus on downstream channel construction, build regional distribution networks, capture incremental market dividends, and have high gross profit margins in the early stage, but their market barriers are weaker than the network effects of issuers.

The development path of the leading stablecoins – the rise depends on traffic, and the success or failure of the supply chain

The core elements of stablecoin competition are: 1. Credit endorsement; 2. Liquidity support; 3. Channels and customer acquisition capabilities. The competition landscape of leading stablecoins has evolved from competition in on-chain/exchange trading scenarios to competition in markets and channels for non-encrypted scenarios such as cross-border payment settlement.

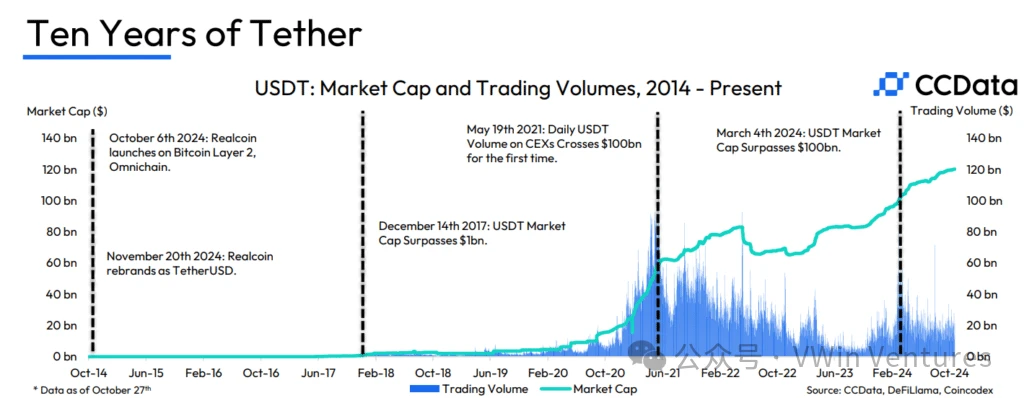

Tether (USDT issuer, with an issuance volume of over 140 billion US dollars and a market share of over 60%):

The development path is similar to the three stages of the development of the US dollar. Combined with the censorship-resistant Tron, it relies on the natural expansion of the distributed network of black and gray industries, forming a strong network effect.

Circle (USDC issuer, with an issuance volume of over 60 billion US dollars and a market share of over 25%):

Early binding exchanges and public chain cold starts (Coinbase Base, Solana, Binance Launchpool)

Obtaining compliance licenses around the world has formed a barrier, and it has survived until competitors withdraw (BUSD is sanctioned by the United States, MiCA Europe withdraws USDT), becoming the largest credible and compliant stablecoin in the capital market

Use compliance endorsements to continuously expand compliant financial channels (exchanges, payment companies, banks), and seize global incremental scenarios (payments, RWA and other new asset transactions)

Circle officially submitted its IPO application to the U.S. SEC in April 2025, and is expected to become the first stablecoin target in the U.S. stock market; the main growth scenarios for stablecoins in the future will come from cross-border trade and the global cross-border payment chain, and the compliant market will be a larger source of growth. USDC, as the compliance leader, is favored by mainstream U.S. institutions and is expected to seize major market share. Circle is expected to achieve significant fundamental growth in the long run.

Future Challenges

Can Tether be recruited in compliance with regulations? To some extent, Tether has helped the dollar expand and become one of the top 20 U.S. debt investment institutions in the world. It also has a deep relationship with Commerce Secretary Lutnicks former asset management company.

The interest rate cut cycle has begun, and issuers’ interest income is declining. How can we improve diversified profitability?

Against the backdrop of deregulation, more and more traditional financial giants (banks, payment companies, etc.) are entering the compliance race. How long will Circle’s leading position in compliance last?

Payment scenarios will become the main battlefield for future competition in stablecoins. Cross-border payment on-chain has huge room for growth

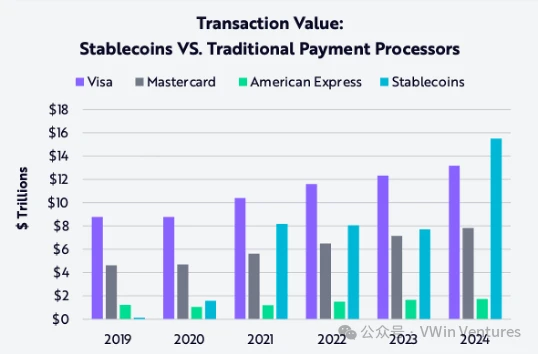

In 2024, the global stablecoin transaction volume has reached 15.6 trillion US dollars, surpassing the scale of traditional payment giants Visa and Mastercard in the same period, becoming one of the worlds most important value transmission networks. It is conservatively estimated that more than half of the volume comes from cross-border payment scenarios.

Traditional payment scenarios have long processes and involve many intermediate links. Stablecoins have obvious advantages in cross-border payment. Stablecoin payments mainly have two core business scenarios:

Scenario 1: To B business

To B is more like a web2.5 business, which adds a fiat currency-stable currency process (which is also the main source of profit) to the original payment chain. Compared with the compliance system, it reduces costs and increases efficiency, realizes regulatory arbitrage in areas with exchange difficulties or sanctions, and solves real needs.

To B customers have large business volumes, stable cash flows, and real business scenarios, including virtual service customers (eg voice chat, online gambling, etc.) and traditional cargo trade customers:

Most virtual service customers have one-way off-ramp demand for stablecoins, for example, the income side is Crypto, and the expenditure side (investment flow, salary payment, etc.) is legal currency. This scenario is highly homogeneous and gradually saturated, and it relies heavily on operations and sales capabilities.

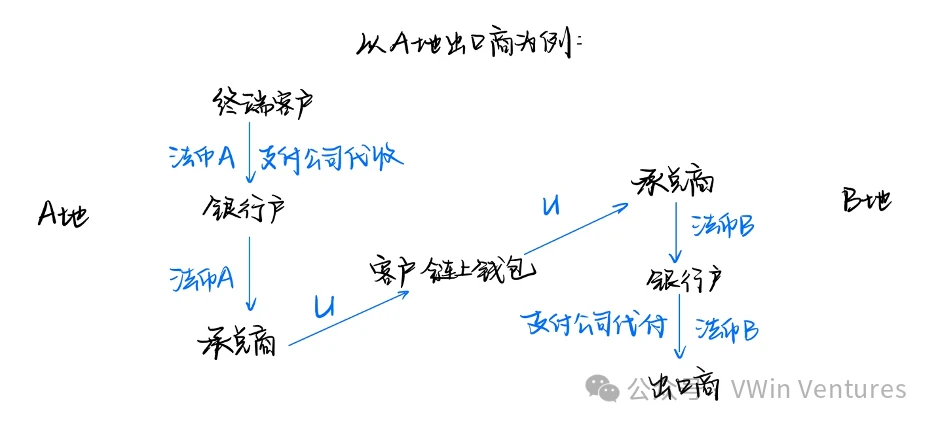

The needs of traditional goods trade customers generally involve the entire cross-border payment process: local acquisition – local acceptance – cross-border transfer – currency exchange – payment on behalf of others , and some also include settlement of foreign exchange, tax refund, etc. In long-tail small countries, there are higher gross profits, and the competition is stable in terms of capital flow channels, channel network construction, and localized operation capabilities. In comparison, the chain is longer, and more inefficient links in the traditional payment chain have been replaced and integrated, with higher value chain optimization and profit improvement space.

When To B business reaches a certain scale, there is compliance pressure, and licenses such as Hong Kong MSO/Singapore MPI become necessary compliance costs after scale-up.

Scenario 2: To C Business

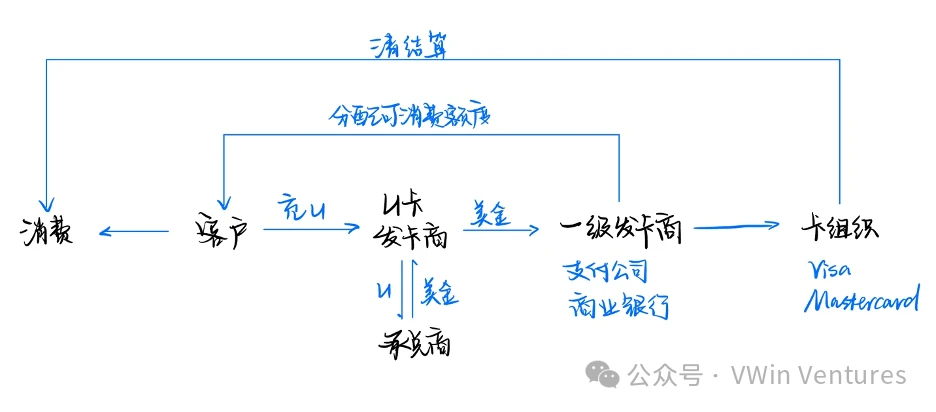

The typical form of To C business is U card issuer, which mainly serves underbank end customers who are not fully served by banks. The overall business currently has a low gross profit margin. The business chain is:

C-end customers – Second-tier card issuers [accepting third-party acceptance] – First-tier card issuers (such as commercial banks, payment companies, etc.) – Card organizations (Visa, Mastercard)

Since the threshold for expanding upstream to first-tier card issuers is relatively high, pure encryption cards are a business with higher risks than rewards. However, they can be used as a means of acquiring customers and a drainage tool for expanding asset management and other businesses by absorbing deposits. They have also become a natural choice for major exchanges to expand their business.

Whether it is B-end or C-end users conducting foreign exchange, compliance and security have always been the biggest pain points in the market. As the market moves towards institutionalization and mainstreaming, licensed financial institutions have become the most compliant and secure trading channels, such as Hong Kong compliant exchanges and listed brokerage firm Victory Securities, providing customers with safe and reliable trading options.

The future development trend of stablecoins: the battle of compliance

Stablecoin payments are currently in a relatively gray area, and compliant stablecoin settlement scenarios have huge potential for growth. As the most upstream of payment scenarios, stablecoins can significantly improve business barriers by binding core channels.

The current compliance development path of the stablecoin market is difficult because of the large conflicts of interest and high compliance thresholds in the traditional financial system. However, in the long run, the compliance route has more strategic value:

In the context of geopolitical conflicts and financial sanctions, trading companies need compliant, secure, auditable and interest-aligned solutions;

Mainstream institutions have entered the market (Fidelity, Wyoming State, World Liberty Finance, etc.) to compete for the transformation of the traditional existing payment market and the listing of high-quality assets on the blockchain;

Local protection and local head players emerge, such as the emergence of compliant stablecoins in Europe and Hong Kong. New players include local banks, payment companies, Internet companies, etc. The license is a stepping stone, and the core of competition lies in seizing the core channel resources and exchange networks;

Under the trend of de-dollarization in international trade, such as in the Belt and Road trade scenario, offshore RMB opportunities are promoted

Strategic competition: Will stablecoins help the US dollar export its financial hegemony?

From a higher dimension of global strategic competition, the US dollar stablecoin carries the de-geographical output of the new round of financial sovereignty of the US dollar. Stablecoins map the US dollar to the global permissionless clearing network of blockchain, which helps capital and liquidity to circulate more smoothly around the world on the funding side, and exacerbates the global Matthew effect and head concentration on the asset side.

Stablecoins have greatly reduced the barriers to the global flow of US dollars, bypassing the banking and central bank systems and directly facing global users. In the past, the US dollar hegemony relied on the central bank for trade settlement. Currently, in many markets, especially developing countries, people spontaneously use stablecoins as a means of pricing, payment and storage. Stablecoins have enabled the free flow of US dollars across borders, making it easier to attract global funds to US dollar assets such as US bonds and US stocks, while also facilitating the US to harvest assets through the US dollar tide.

As a result, central banks in developing countries are in a passive position. The hegemony of the US dollar continues to extend through stablecoins in both compliance and gray areas:

Gray expansion: USDT is a typical example. Backed by the demand for regulatory arbitrage, it is widely used in gray scenarios such as speculation, gambling, and circumventing financial supervision. It is widely used in foreign exchange control regions such as Southeast Asia, Latin America, and Africa, rapidly expanding its user base and market penetration.

Compliance expansion: represented by USDC, supported by US regulators and gradually incorporated by mainstream financial institutions, building a compliant on-chain US dollar clearing and settlement network has huge long-term value. However, due to certain conflicts of interest with the traditional payment system, the current growth is relatively slow, and the development path is more dependent on official supervision and institutional endorsement.

The US regulatory strategy is reflected in condoning the wild growth of the gray area (USDT) while actively supporting the development of compliant scenarios (USDC). The two together build a strategic moat for the US dollar on the chain and achieve a siphon effect on global financial liquidity.

As a strategic projection tool for the US dollar hegemony, stablecoins are essentially a weapon of programmable financial sanctions. The United States controls this seemingly decentralized network clearing network. The United States can accurately strike targets through regulatory compliance and smart contract asset freezing (such as USDC freezing Tornado Cash related addresses).

For policymakers in developing countries or elsewhere, how to avoid becoming a “digital dollar colony”:

If we fail to build a credible local on-chain financial system, we will become a passive user of the US dollar stablecoin system for a long time.

Liquidation is hegemony in the new era: Controlling the on-chain clearing flow is like controlling the global water source - seemingly free, but actually with a valve. Consider launching national or regional on-chain financial infrastructure (such as local stablecoins, CBDCs) to reduce over-reliance on the US dollar on-chain system.

Conclusion: Stablecoins, a strategic weapon for the US dollar hegemony in the new era and a historical opportunity for reshaping the global financial order

The promotion and popularization of stablecoins relies on real transaction demand and clearing efficiency to build a structural and sustainable capital flow network on a global scale.

Currently, stablecoins are relatively stable in the crypto trading scenario, with leading players monopolizing the market share and incremental growth coming from new financial assets being put on the chain; while payment scenarios, especially cross-border payments, are the current main incremental blue ocean and structural breakthrough.

The on-chain payment and clearing and settlement network built around stablecoins is eroding the cross-border payment system dominated by traditional banks and SWIFT, giving rise to a huge payment and exchange market worth trillions of dollars, providing global financial institutions, payment companies and even national financial infrastructure with a historic opportunity to redefine their roles.

The rise and widespread popularity of stablecoins essentially continues the penetration of the US dollar hegemony in the financial system, but upgrades it to a more covert, more extensive, more strategic and more precise on-chain version. Competition in the stablecoin era is no longer a game at the level of financial instruments, but a strategic contest for global monetary sovereignty and the right to speak in the global financial order.