1. Industry Trends and Status

The emergence of blockchain technology has brought many advantages such as distributed ledger and decentralization, but it has also led to a relatively isolated ecosystem for each blockchain. Different blockchains cannot interact directly, which brings many limitations and challenges to the application of blockchain technology. Therefore, how to achieve interoperability between different blockchains has become an important issue.

To solve this problem, cross-chain bridge technology has emerged. Cross-chain bridge is a technical means to establish connections between different blockchains, achieve cross-chain communication and asset transfer.

Through cross-chain bridges, users can transfer assets from one blockchain to another, and also execute cross-chain smart contracts, promoting the integration and development of blockchain ecosystems.

Therefore, cross-chain bridge is one of the key technologies to achieve interoperability between different blockchains, which is of great significance for the practical application and promotion of blockchain technology.

1. Cross-chain bridge technology is becoming more mature, and the demand and role are highlighted

In the past, users generally completed cross-chain operations through centralized exchanges, for example, transferring assets to centralized exchanges and then withdrawing to the target chain.

With the continuous improvement of the public chain ecosystem and the popularization and development of DeFi technology, the use cases of digital assets are increasing and liquidity is significantly enhanced.

For example, there is an increasing demand to transfer assets to DApps on different chains for staking, financial management, etc. This has led to the emergence of cross-chain bridge applications. People are increasingly inclined to use cross-chain bridge technology directly to complete asset transfers between different chains, instead of using centralized exchanges for cross-chain operations.

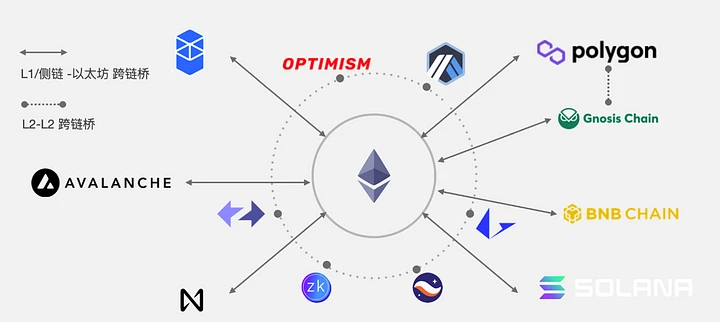

2, Rollup cross-chain bridge for different L 2 chains

In the current landscape of public blockchains, the development of the Ethereum ecosystem is still the most mature and complete. More and more DApps choose to develop on the Ethereum ecosystem.

However, Ethereum is often referred to as the "aristocratic chain". Not only are the gas fees expensive, but also the speed cannot meet the high real-time requirements of DApps. As a result, more and more Ethereum Layer 2 solutions have emerged. They improve performance while inheriting the underlying security of Ethereum.

For example, Arbitrum, Optimism, Starknet, and Zksync, known as the four major players in Ethereum Layer 2, have developed rapidly and formed their own ecosystems. Each Layer 2 ecosystem has accumulated a large number of users and assets.

The prosperity of the Ethereum Layer 2 ecosystem has also created a demand for cross-chain assets on Ethereum Layer 2, and Orbiter Finance emerges in such a background.

In the past Layer 2 framework, rollups cannot be directly transferred between each other.

If users want to transfer assets from Rollup A to Rollup B, they often need to wait for a long time.

1) Transfer assets from Rollup A to the mainnet;

2) Transfer assets from the main net to Rollup B.

The mainnet serves as an intermediary, and both transfers need to go through the Ethereum mainnet.

Not only is the speed slow, but it also requires two gas fees, resulting in high time and gas costs.However, the emergence of cross-chain bridges like Orbiter has built a bridge between different Ethereum Layer 2 solutions, greatly improving the interaction efficiency between Ethereum Layer 2 solutions and promoting the flow of digital assets. It is through this flow that value is released.

first level title

Orbiter Finance is a decentralized cross-rollup bridge that enables users to transfer assets between Ethereum mainnet, StarkNet, zkSync, Loopring, Arbitrum, Optimism, Polygon, Immutable X, and BNB Chain.

Orbiter Bridge provides users with excellent experiences such as low fees and fast speeds through its unique market maker model. At present, it only supports transfers of ETH, USDC, USDT, and DAI.

III. Financing Situation

In November 2022, Orbiter completed its first round of financing, with participation from Tiger Global, Matrixport, A&T Capital, StarkWare, Cobo, imToken, Mask Network, Zonff Partners, and others, but the financing amount was not disclosed.

Additionally, Vitalik has donated 16 ETH.

Four, Orbiter Finance Features

1. Security

Based on rollup technology, Orbiter does not have risks like Layer 1 Layer 1 cross-chain bridges.

Firstly, we need to be clear that Orbiter Finance aims to solve the problem of cross-rollup, rather than cross-chain (heterogeneous chain) issues.

Strictly speaking, Orbiter is a cross-rollup bridge, not a bridge for assets between two completely independent (heterogeneous) blockchains (e.g., from the Bitcoin network to the Ethereum network).

When it comes to asset cross-chain between two independent heterogeneous blockchains (Layer 1 Layer 1), the security of the cross-chain protocol complies with the bucket theory, which means that the upper limit of the security performance of the cross-chain protocol is determined by the chain with lower security.

Ethereum founder Vitalik wrote an article on this topic, where he introduced a concept called "shared security", which means exactly that.

For example, A and B are two heterogeneous chains, where A chain has high security while B chain has low security.

Therefore, when conducting cross-chain asset transfers between these chains, the security is determined by the security of the B chain (the chain with lower security).

The main goal of cross-chain projects is to ensure transaction security between two unique chains and prevent 51% attacks.

However, cross-rollup projects use the same Ethereum data layer, and each rollup can prevent 51% attacks. Based on this, Orbiter proposed a cross-rollup mechanism that inherits Ethereum Layer 2 security.

In simpler terms, EOA is actually our personal account, that is, our wallet address, which is different from contract accounts with interactive functions.

What are the benefits of using an EOA address in the Orbiter cross-chain protocol?

The biggest benefit is low cost and fast speed.

Because unnecessary contract interactions are eliminated, there is no need for a dedicated intermediary to mint/destroy assets, and the transfer is directly carried out between the Sender (asset exchange party) and the Maker (market maker, i.e., the party accepting cross-chain exchange demands).

Most traditional cross-chain bridges take about 10 minutes or longer to complete asset cross-chain transfers, but with Orbiter, users can complete asset cross-chain transfers in an average of 30 seconds.

3. Supports native Ethereum assets

In the Orbiter cross-chain protocol, asset minting is not required.

As we all know, Bitcoin, as the highest market value cryptocurrency, has not fully utilized its liquidity potential due to high gas fees and slow transaction speeds.

In order to introduce the highest market value cryptocurrency BTC into the Ethereum DeFi ecosystem and promote its liquidity, a common practice is to wrap BTC, for example, into an ERC20 token called WBTC on Ethereum, thereby unlocking the liquidity potential of BTC. This is actually a form of cross-chain approach.

However, the Orbiter cross-chain protocol supports native Ethereum assets and does not require wrapping or other operations.

How does Orbiter accomplish cross-chain functionality? An example will make it clear.

For example, A wants to transfer their 0.1 ETH from the zkSync chain to the Arbitrum chain.

The general process for cross-chain transfer using Orbiter (excluding fees) is as follows:

1) A, as a Sender, transfers 0.1 ETH from zkSync to the address of B (one of the Makers, which can be understood as a cross-chain intermediary). This step only occurs on the zkSync chain.

2) B, as a Maker (cross-chain intermediary), receives 0.1 ETH on zkSync.

>3) After receiving 0.1 ETH on the zkSync chain, B transfers 0.1 ETH to A's Arbitrum address on the Arbitrum chain. This step only occurs on the Arbitrum chain.

4) B receives 0.1 ETH on the Arbitrum chain.

Throughout the entire cross-chain process, there is no need for asset wrapping; it is simply the transfer of native assets between different addresses.

In this process, the two token transfers occur on Ethereum's Layer 2 network, which has very low transaction fees and faster speeds.

Let's take an inappropriate example.

This is like communication between Chinese people and Americans. Due to different languages, cultures, and religious beliefs, communication between the two parties requires translation as an intermediary, which naturally increases the cost of communication.

And if it is communication between people from Hunan and Hubei, because they have similar cultural backgrounds and beliefs, there is no need for a translator as an intermediary. The communication is much smoother and of course the cost will be much lower.

5. Operation Mechanism

1. Two Roles

In Orbiter Finance, there are two roles, Sender and Maker.

Sender is the person initiating the cross-chain transfer, the demand side of the cross-chain, while Maker is the liquidity provider, the counterparty to Sender, and the recipient of the cross-chain service.

When Sender initiates a transfer, Maker provides liquidity, and the smart contract ensures the security of the entire process.

Before Maker provides cross-rollup for Sender, it needs to deposit excessive collateral in Orbiter's contract and set the service in the protocol.Fees rules.

During the execution process, Sender sends assets to the Maker on the Resource network, and the Maker sends the assets back to the Sender on the target network.

If Maker engages in malicious behavior, such as not transferring the assets back to Sender on the target network after receiving them from Sender.

At this time, Sender can initiate an arbitration request to the contract using Maker's collateral, and then receive excess compensation.

2. Maker Operation Process

In the Orbiter cross-chain protocol, a client will be provided to Maker. Of course, Maker can also deploy a client on its own to automate the refund process, that is, some backend operations of Maker can be automatically completed.

In this client of Maker, the user's cross-chain currency, amount, and cross-chain network will be considered.

Listening to the network and implementing corresponding automation operations based on the data obtained is a normal process. 3. Decentralized anti-malicious mechanism However, Maker may also engage in malicious behavior. To address the issue of Maker's malicious behavior, Orbiter adopts a solution called "pre-trust + dispute arbitration." By default, Orbiter trusts Maker and assumes that Maker will handle assets correctly and return the corresponding assets to users. However, there is a possibility that Maker may engage in malicious behavior, such as withholding the user's assets after receiving cross-chain assets and not returning them to the user on the target chain. Therefore, Orbiter uses a decentralized mechanism, mainly implemented through three contracts: MDC, EBC, and SPV, to prevent Maker from engaging in malicious behavior. 1) MDC contractMDC is short for Market Deposit Contract.

The MDC contract has two functions: custody of Maker's margin and processing of Sender's fund return and compensation.

2)EBC Contract

EBC is short for Event Binding Contract.

This contract is used to prove the validity of transactions on the source network and the target network.

3)SPV Contract

SPV is an abbreviation for Simple Payment Verification.

It is a simple transaction verification contract used to prove the existence of transactions on the source network.

For example, Sender sends 0.1 ETH to Maker on Arbitrum, and SPV is used to prove the authenticity of this transaction.

Then these three contracts will run a mechanism, and Orbiter can ensure that users do not suffer asset losses when Maker misbehaves.

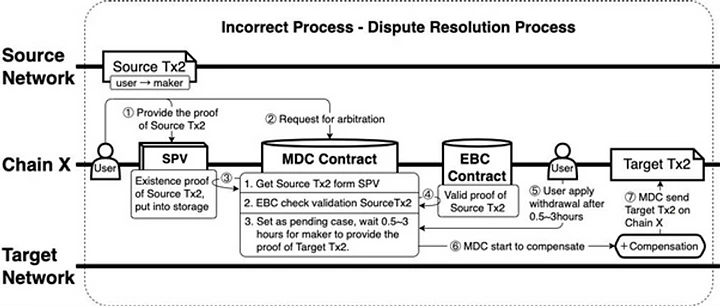

If the Sender fails to receive the tokens correctly from the Maker after transferring them, the dispute resolution process will follow the steps below to help the Sender retrieve the tokens:

1) The Sender needs to provide relevant transactions from the source network to the SPV contract.

2) The Sender requests arbitration through Orbiter's MDC contract.

3) The MDC contract obtains proof of existence for the transactions from the SPV contract and confirms that the transaction has occurred on the source network.

4) MDC contract obtains proof of validity for transactions on the source network from the EBC contract.

The MDC contract verifies that transactions on the source network, according to Orbiter's rules, are legitimate and sent by the Sender to Orbiter's Maker with a valid identification code.

5) The MDC contract sets this arbitration as a pending case, and the Maker needs to provide the target network transaction within 0.5 to 3 hours.

If the Maker provides the correct target network transaction within the specified time, the MDC contract can obtain proof of validity for the target network transaction from the EBC contract, confirm the match between the target network and the source network transactions, and close this arbitration by displaying the target network transaction to the Sender;

Otherwise, if the Maker fails to provide relevant target network transactions within the specified time, the Sender can trigger the MDC contract to arbitrate.

6) The MDC contract starts arbitrating Sender compensation.

7) The MDC contract will send the tokens and compensation (about $15) back to the Sender on the MDC contract deployment domain. The tokens returned and compensated to the Sender are deducted from the Maker's collateral.

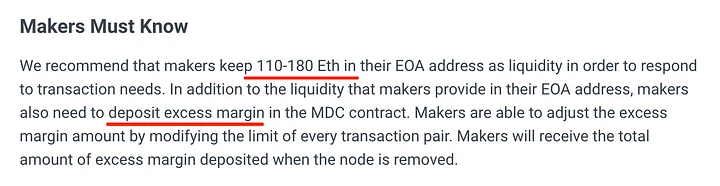

4. Excess Collateral Mechanism

In addition, in order to prevent malicious behavior by the Maker, Orbiter Finance has also introduced an excess collateral mechanism.

In the Orbiter protocol, the Maker needs to provide two types of funds, one for liquidity, which is the funds exchanged to users, and the other is excess collateral.

If the Maker is dishonest and the Sender does not receive tokens as scheduled in the target network, then all losses incurred by the Sender will be paid out of the excess margin, and the Sender will also receive compensation from the Maker's excess margin.

So, in the Orbiter protocol, does the Maker have enough incentive to provide better services?

First, in the mechanism of Orbiter, the Maker can earn substantial income from each cross-chain service (without impermanent loss risk).

Second, if the Maker fails to timely send the correct information to the Sender, the MDC contract of Orbiter will send it back and compensate the Sender with the Maker's margin.

Therefore, Orbiter's design not only prevents Maker's malicious behavior but also incentivizes Maker to provide better services.

5. Fees

For Senders, Orbiter fees include transaction fees and withholding fees.

Transaction fees: Fees paid to the platform and Maker, charged as a percentage of the transfer amount.

Withholding fees: Fees prepaid to the Maker for the purpose of paying Gas fees when transferring to the destination network.

Due to the fluctuation in Gas fees, Orbiter adjusts the fees based on the Gwei of the destination network to ensure that Orbiter's fees are lower than the average level, but such adjustments are not frequent.

6. Orbiter Advantages

1. Cross-chain Speed and Fees

In terms of cross-chain speed and fees, Orbiter offers the following advantages:

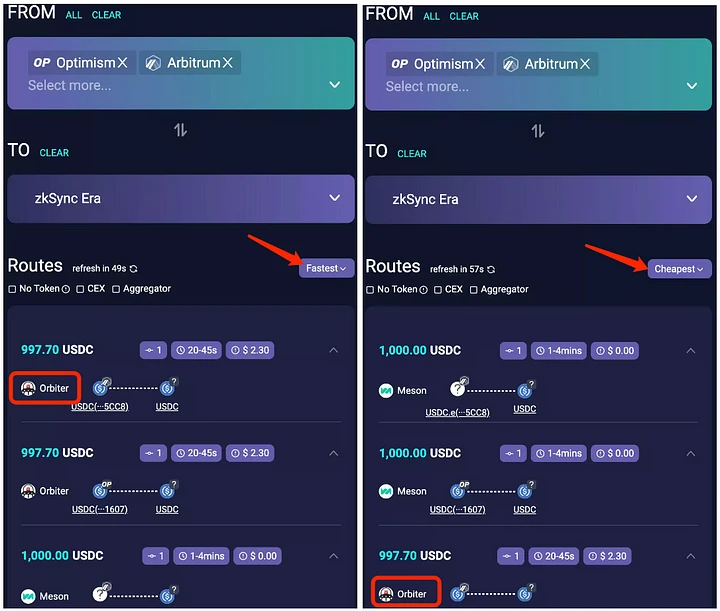

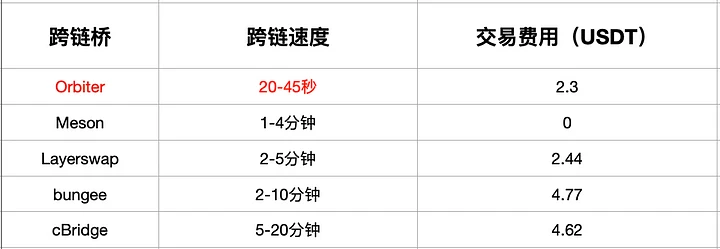

data-selectable->You can query the speed and fees of some cross-chain bridges of Ethereum L 2 through https://chaineye.tools/bridge.If we transfer 1000 USDC from the OP chain/ARB chain to the ZK chain, let's see the fees and speed of these cross-chain bridges:

You can see that Orbiter is the fastest, completing cross-chain transfers in about 20-45 seconds, while Meson, ranked second, takes 1-4 minutes.

And if ranked by transaction fees, Orbiter ranks second, but Meson, ranking first, has a fee of 0. Meson has a daily limit of 5 transactions/$5000 exempt from fees.

For the same scenario, let's take a look at the time required by other cross-chain bridges:

Layerswap: 2 - 5 minutes, cost: 2.44 U

Bungee: 2 - 10 minutes, cost: 4.77 U

cBridge: 5 - 20 minutes, cost: 4.62 U

When performing cross-chain operations, speed and cost are both important factors for us. By comparison, in terms of overall speed and transaction fees, Orbiter is still very excellent, especially its cross-chain speed is much faster than other cross-chain bridges.

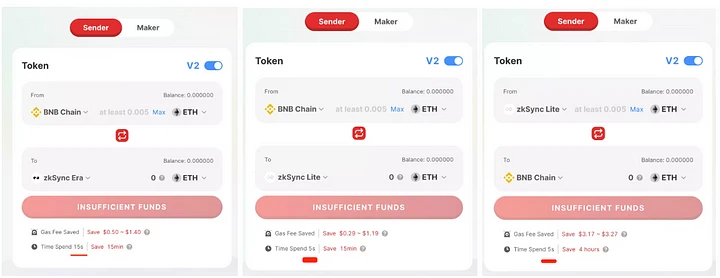

In the Orbiter cross-chain bridge, the time required for cross-chain transactions is usually around 30 seconds. The slowest one is the Ethereum mainnet, which takes about 45 seconds to cross to the Layer 2 network or vice versa. The fastest cross-chain transaction is between the BNB chain and the ZK chain, which can be completed in just 5 seconds. Other Ethereum Layer 2 cross-chain bridges generally take more than 2 minutes to complete.

2. Security

In the Orbiter cross-chain protocol, decentralized anti-fraud measures and over-collateralization mechanisms prevent liquidity providers from behaving maliciously after receiving funds, ensuring the security of user funds and enhancing the protocol's security.

In addition, since Orbiter is built on top of Ethereum, it inherits Ethereum's security. Therefore, Orbiter has a strong advantage in ensuring fund safety.

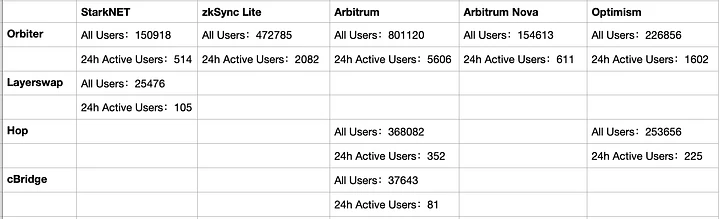

3. Active Users

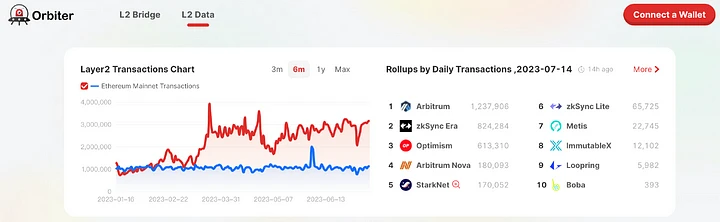

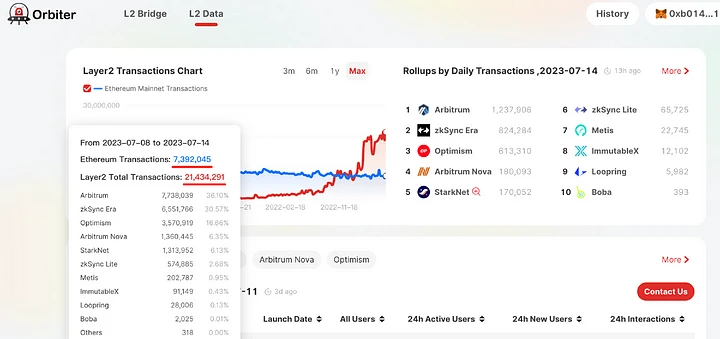

You can check some active users of cross-chain bridges at https://www.orbiter.finance/data.

After data statistics from the Orbiter L 2 Data platform, Orbiter has advantages in terms of active users and user breadth.

4. Official Endorsement Recommendation

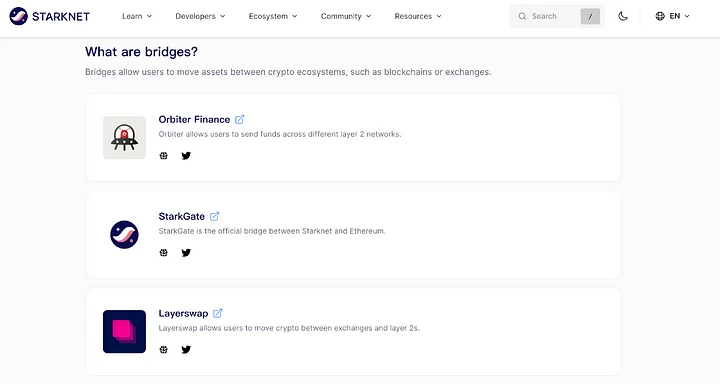

StarkNET's official website recommended the Orbiter cross-chain bridge, ranking first.

The Zksync official website also recommended Orbiter in the cross-chain bridge section.

Optimism also recommended the Orbiter cross-chain bridge in the ecosystem's cross-chain bridge subdivision project.

Orbiter has official endorsement for its cross-chain bridge, which naturally increases its credibility. Moreover, the official recommendation will bring Orbiter a considerable number of users.

5. L 2 Data

In addition to cross-chain functionality, Orbiter has also launched an L 2 Data (Data Dashboard).

L 2 Data supports Arbitrum, Optimism, Starknet, and zkSync data, including metrics on accounts and transactions, TVL, users and user age, active user ratio, new user ratio, interactions, and new contracts.

Orbiter L 2 Data aims to provide individuals, institutions, and developers with more comprehensive, scientific, and effective data on the Rollups ecosystem.

L 2 Data is also a unique feature that sets Orbiter apart from other cross-chain bridges.

Seven, Future Outlook

1. Cancun Upgrade, L 2 Eruption, Increase in Cross-chain Demand

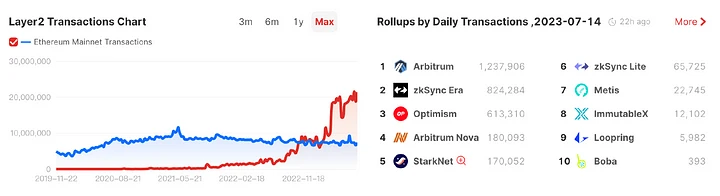

According to Orbiter L 2 Data (https://www.orbiter.finance/data) platform statistics, since the end of last year, the Ethereum network has experienced an explosive growth in L 2 solutions such as Arbitrum, Optimism, and others, indicating an increasing demand for cross-chain solutions.

L 2's total number of transactions has surpassed that of the Ethereum mainnet.Currently, the total number of transactions on Ethereum L 2 is more than three times that of the Ethereum mainnet, including a significant number of interactions conducted for airdrops.

However, even if some transactions are for airdrops, the data at least also indicates the current development status of Ethereum L 2 ecology. After all, Layer 2 networks have lower fees and higher scalability, and more and more projects choose to build their own projects on Ethereum Layer 2 or migrate from other chains to Ethereum Layer 2.

With the completion of Ethereum's Cancun upgrade (possibly by the end of the year, currently there is no exact time), the transaction fees on Ethereum Layer 2 networks will be significantly reduced. When the transaction fees on Layer 2 networks approach 0, it is likely to bring about a big explosion in the Ethereum Layer 2 ecosystem.

As the Ethereum Layer 2 ecosystem becomes more and more prosperous, the demand for cross-chain bridges will also increase significantly. With the advantages of the cross-chain bridge Orbiter, it will definitely gain a larger market.

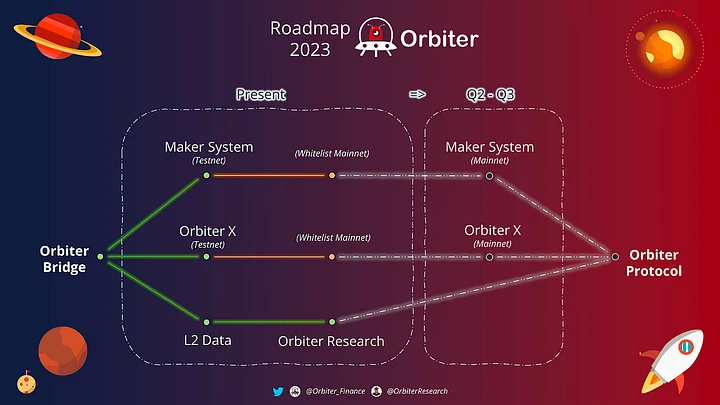

2. Orbiter X and Orbiter Protocol's Tremendous Potential

According to the Orbiter Roadmap, Maker System and Orbiter X are scheduled to be released in Q2-Q3, but the specific dates have not been confirmed yet.

Orbiter X is an enhanced version of Orbiter that provides a simple and secure platform for executing cross-chain and cross-asset transfers. Supported by a powerful Maker system and a decentralized cross-rollup bridge, these features make Orbiter X the ideal choice for anyone looking to transfer assets between different networks quickly, securely, and cost-effectively.

According to the official Orbiter Medium, Orbiter's goal is not only to act as an L2 cross-chain bridge but also to serve as infrastructure for Ethereum's expansion. Orbiter aims to be a universal Ethereum protocol.

Centered around Ethereum's expansion, the Orbiter Protocol is driven by a range of cutting-edge features, such as zero-knowledge algorithms, EIP-4337 (account abstraction), recursive proof, and message synchronization. These features aim to facilitate better scalability, interoperability, and security, thereby improving the overall availability and adoption of the Ethereum network.

The transition from Orbiter to Orbiter Protocol reflects the platform's commitment to enhancing the Ethereum ecosystem.

By then, Orbiter will not only be a cross-chain bridge protocol, but also a general Ethereum-based protocol, which undoubtedly enhances our imagination space for the future of Orbiter.

3. Expected Issuance of Platform Tokens

As we all know, although Orbiter has been online for more than two years and the project has been developing quite well, Orbiter has not yet issued its native tokens, and the official has not disclosed any information about the token issuance.

However, there have always been rumors about Orbiter issuing native tokens. Due to the expected issuance of tokens by the project party, many users use Orbiter in order to benefit from airdrops.

In any case, with the outbreak of Ethereum Layer 2, the demand for cross-chain bridges will also increase rapidly. As a leader in the subdivided track of Layer 2 cross-chain bridges, Orbiter, along with the project party's grand vision (to become an Ethereum underlying protocol), will definitely develop better and may become a leader and standard setter in Ethereum L2 cross-chain bridges. In addition, since the project has not yet issued native tokens, Orbiter is a project worthy of our continued attention.

Follow the hot air balloon @HorairballoonCN on Twitter for more industry information: https://twitter.com/HotairballoonCN