Original author: YettaS (X: @YettaSing )

Yesterday, the presidents words once again boosted $XRP, surpassing $ETH to become the second FDV in a short period of time. Although it has long been famous, few people know what it does. Is Ripple a huge scam? If not, why do we hardly see its real users in daily life? What is the scale of Ripples business? Is it enough to support its current value? If not, what does it rely on?

This article will take you through Ripples business logic and face its challenges and controversies, from its cross-border payment innovation to the core XRP bridge role, to help us understand in depth how to turn populism into a feast of capital and technology in this industry.

What kind of business is Ripple?

Ripple is engaged in cross-border payment business. The traditional cross-border payment process is divided into information flow and capital flow. At the information flow level, SWIFT unifies the standards of various remittance countries; at the capital flow level, the initiating bank and the receiving bank complete the clearing and settlement. If there is no direct relationship between the two, the funds need to be transferred through the corresponding bank or central bank. Most of the funds transfers need to go through multiple intermediary banks. Therefore, there will be problems such as: 1. long time, 2. high cost, 3. low transparency.

Crypto is very suitable to solve the transfer and settlement of funds.

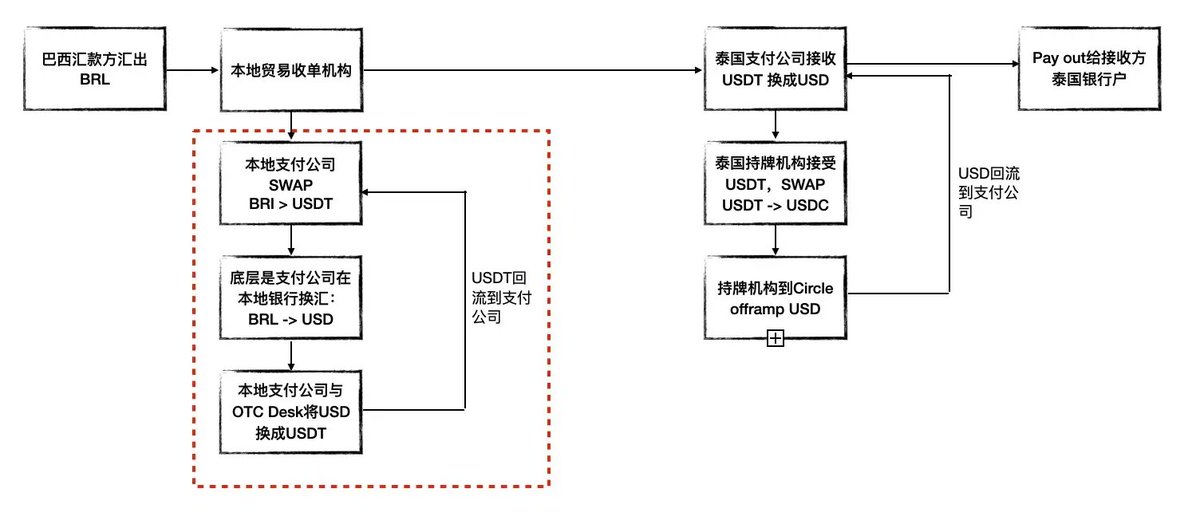

Let’s first talk about the solution under stablecoins: local OTC/payment companies receive foreign exchange, which is exchanged into USD at the bank. USD needs to go to OTC such as Cumberland to exchange into USDT, and then USDT completes the transfer on the chain. The OTC conversion from USDT to USD must be completed again at the receiving end, and then the exchange is exchanged into local currency through the bank. Under this solution, the transfer and settlement of USDT becomes very simple, but the difficulty and moat lies in the entire OTC network. If USDC is used, the process will be more convenient because deposits and withdrawals can be completed directly with Circle in compliant places.

The following figure is a flowchart with USDT on one end and USDC on the other end as an example. In fact, the red box in the figure below is the key to the entire stablecoin cross-border payment, that is, OTC can provide USDT deposits and withdrawals at any time, and the amount of funds they occupy is not small. This is the highest cost link in cross-border payment, and therefore it is also the place where Tether has the most moat. This is exactly what I mentioned in Consensus in the Cracks: Tether and the New Global Financial Order : All kinds of channels and exchange platforms have become Tethers workers to help it spread its network to the world.

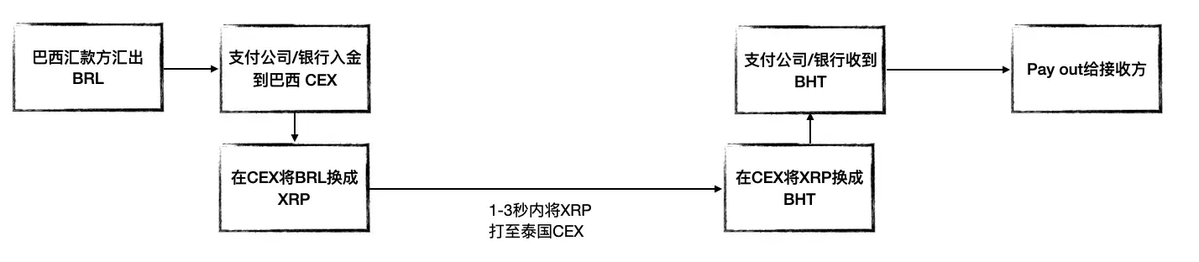

Ripple is actually a simpler solution than stablecoin. Its process is that foreign currency is exchanged for XRP through local banks or payment institutions at CEX, XRP is transferred to the CEX of the receiving country, and then XRP is exchanged for local currency. The following figure takes Brazil to Thailand as an example, and the currency link is BRL -> XRP -> BHT. In other words, Ripple uses XRP as a bridge currency to recreate a foreign exchange market.

Ripple actually provides a very clever and efficient cross-border payment solution. In traditional SWIFT or stablecoin cross-border payment scenarios, capital occupation has always been a pain point. Every time a currency exchange is carried out, banks or OTCs usually need to pre-inject sufficient funds into the account to ensure the smooth completion of the entire payment process. For example, in the stablecoin solution, banks must have enough USD for currency exchange, and OTC merchants need to reserve USDT in advance. This pre-funding is not only cumbersome, but also greatly reduces the efficiency of fund use. But Ripples advantage is that it cleverly utilizes the liquidity mechanism of CEX and avoids the pain point of pre-preparing cash. By exchanging assets directly on CEX, this is the On-Demand Liquidity it proposed.

What is the key to rebuilding the foreign exchange market?

Ripple is not just doing an ordinary business, it is more like promoting a new cross-border remittance model. From a compliance perspective, the policy environment and transaction models available in different regions are different, and Ripple is trying to single-handedly promote this new market change through its own efforts.

There are two key elements in Ripples development path:

Bank BD: Make banks willing to use XRP as a cross-border payment solution.

CEX market depth: Ensure that XRP trading markets in various regions have sufficient liquidity to support global currency exchange.

To this end, Ripple has not done less.

Lets talk about the first point first. Ripple did not directly engage in too many currency-related businesses before 2017. Its initial goal was to replace SWIFT, relying on the advantages of the information layer, and cooperating with many banks to promote the education process of the market. In this way, Ripple gradually made major banks in various places its strategic partners. For example, in September 2016, SBI (Strategic Business Innovator) acquired 10.5% of Ripples shares for 55 million. In the same year, Ripple also received investment from SCB (Siam Commercial Bank). It was not until 2017 that Cuallix became the first financial institution to try to promote XRP as a bridge currency . With the epidemic, the business using XRP as a bridge currency was widely rolled out.

Here is also an explanation for why there are few real use cases of Ripple, because Ripples cross-border payment solution is not directly exposed to ordinary users or merchants. It is mainly operated through the banks channels, and merchants or remittance recipients do not need to know what channels the bank uses to remit money. In fact, as long as the bank is willing to allocate a little bit of business to Ripple, it is enough to support the entire business model.

Lets talk about the second point. Ripple must establish a global CEX network to ensure the trading depth of XRP, 7*24 hours trading, small slippage, and smooth deposit and withdrawal. Ripple has also made great efforts on this end. For example, in 2019, Ripple invested in Mexicos first CEX Bitso, and gradually expanded its market influence to Brazil and Argentina. At the same time, Coins.ph, a mainstream exchange in the Philippines, became an authorized partner of Ripple and became its Preferred CEX for XRP payment, further enhancing Ripples market penetration.

Ripple is actually a highly BD-driven business. Just take a look at LinkedIn and you will find that Ripple has a large BD and Marketing team, and all of them have high-end backgrounds in consulting and investment banking. Most people cannot support this situation.

How is Ripple doing in this business?

In 2023, the volume of global cross-border payments will be about 190 trillion . In contrast, Ripple has so far handled about 35 million cross-border transactions with a transaction value of about 70 billion, which is only a sesame seed compared to the volume of global cross-border payments.

I have interviewed a local OTC trader in Latin America. Their annual cross-border transaction volume is about 1 to 1.5 billion US dollars. This is just an ordinary OTC desk. From this perspective, Ripples transaction scale is insignificant compared to the market influence of stablecoin payments.

According to industry practice, the cost of cross-border payments is usually between 1% and 2%. Based on this calculation, if Ripple relies solely on cross-border payment business income to make a profit, it is obviously a drop in the bucket.

What’s more, in the early days, Ripple had to make a lot of subsidies in order to get banks and payment companies to use its solutions. For example, in the first quarter of 2020, Ripple paid a subsidy of 15 million US dollars to MoneyGram , once the world’s second largest remittance company, to encourage them to use the Ripple network.

What’s next for Ripple — expanding custody and stablecoins

Unlike Tether, which directly leverages the global liquidity of the US dollar and promotes the expansion of US dollar hegemony, Ripples ecosystem is completely dependent on building its own network and attracting alliances to maintain. The bottleneck of this payment business is obvious. Therefore, Ripple also needs to think about how to break through this bottleneck. Based on its own corporate customer advantages, Ripple has chosen three business lines for expansion - Payment, Custody, and Stablecoin.

In May 2023, Ripple acquired Swiss custodian Metaco for US$250 million .

In June 2024, Ripple acquired Standard Custody . Standard has nearly 40 currency payment-related licenses in the United States, a major payment institution license (MPI) from the Monetary Authority of Singapore (MAS), and a VASP (Virtual Asset Service Provider) registration from the Central Bank of Ireland. Its CEO Jack McDonald also serves as Ripples senior vice president of stablecoins, which actually paves the way for Ripple to issue stablecoins.

In December 2024, Ripple officially issued the RLUSD stablecoin and obtained approval from the New York Department of Financial Services (NYDFS).

At this point, Ripple can be viewed as a normal Fintech company, with the three business chains clearly broken down.

How Crypto Helped Ripple

If the business itself doesn’t make much money, then how does Ripple make money? The answer is simple: selling coins.

The protracted lawsuit between Ripple and the SEC was caused by selling coins. The SEC accused Ripple of selling more than $1.3 billion of XRP to 1,278 institutions to finance the company. The SEC believes that XRP is an unregistered security, which violates federal securities laws and requires Ripple to pay a fine of up to $2 billion. In August 2023, the court ruled that Ripple only had to pay about $125 million , but the judge also mentioned that its On-Demand Liquidity service may have crossed the line.

Why can Ripple sell such a large amount of coins?

We mentioned earlier that On-Demand Liquidity (ODL) is the core of Ripples cross-border payment solution. As long as the liquidity of XRP is guaranteed, all parties do not need pre-funding and can use XRP when exchanging currency. Based on this, ODL provides Ripple with continuous liquidity support for monetization. After all, the largest holder of XRP is Ripple itself. Moreover, as a bridge currency for cross-border payments, XRP should obviously not be defined as a security but a currency.

On-Demand Liquidity is actually a very clever way to kill three birds with one stone in Ripple’s business.

Ripple closely binds business needs with the circulation of XRP. The liquidity of XRP in business scenarios not only provides a basis for Ripples narrative, but also makes its operations in the capital market more handy.

A high-end financial populism experiment

Ripples business model has actually gradually shifted from products to capital operations, and has gradually evolved into a market consensus-driven profit-making method. This is why we jokingly call Ripple a blue-chip meme that only follows favorable policy fluctuations.

In my opinion, Ripples business logic is a brilliant financial populist experiment. It attracts the participation of mainstream financial institutions by packaging the pain points of cross-border payments, and at the same time, it takes advantage of the cognitive bias of Crypto retail to amplify the strategic significance of its business. This also makes Ripples business operations deviate from the simple business-driven profit path of traditional Fintech companies and enter a high-risk and high-return field that relies more on market narrative and capital logic.

We have no way of knowing what the original intention of the project was, whether it was to obtain initial funds through capital operation to promote industrial progress, or to play the game of capital arbitrage by borrowing products of certain value. But it is undeniable that Ripple has a sophisticated control over financial populism.

In the financial market, value creation and value recognition are often not completely equal, especially in a highly speculative environment like Crypto, where market consensus itself can constitute a business model, and Ripple is a typical example of this model. It is neither completely dependent on product growth to drive revenue like traditional Fintech, nor completely dependent on liquidity bubbles like pure Crypto speculative projects, but it cleverly shuttles between compliant financial systems, shapes credibility with institutional endorsements, and amplifies its narrative with the help of policies and market sentiment.

Is Ripple creating value or manufacturing faith? The core of high-end financial populism often lies in this ambiguous boundary.