Original | Odaily Planet Daily ( @OdailyChina )

Author: Azuma ( @azuma_eth )

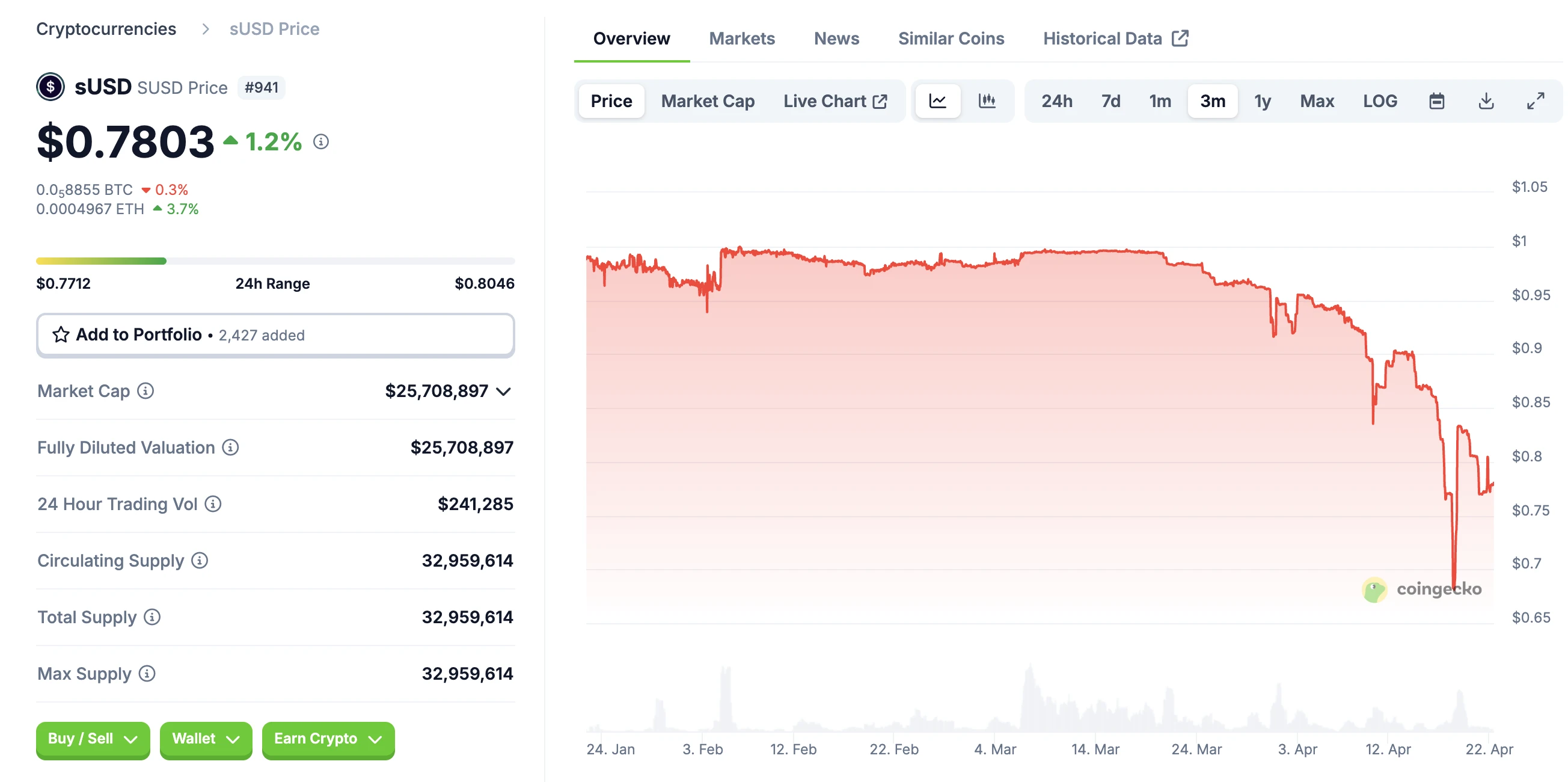

Synthetixs stablecoin sUSD has recently attracted market attention due to its long-term decoupling.

Since the initial signs of decoupling on March 20, sUSD has continued to decoupling, falling below $0.7 at one point and temporarily reporting $0.78 as of the time of writing. As Synthetix continues to roll out various bug fixes, sUSD seems to have stabilized at a low level, but whether it can return to the anchor is still a rather complicated issue for the time being.

Brief analysis of the reasons for anchoring

The decoupling of sUSD needs to start with Synthetix’s positioning transformation and protocol changes.

Synthetixs original positioning was a synthetic asset (Synths) protocol that allows users to mint synthetic assets that track the performance of different assets (such as BTC, ETH) through over-collateralization. sUSD is the only synthetic asset that still has a wide range of uses today, as Synthetix has gradually abandoned the original synthetic asset model and turned to perpetual contract DEX.

Previously, Synthetix users had to pledge SNX to mint sUSD at a 750% collateralization rate - that is, for every $7.5 of SNX pledged, $1 of sUSD could be minted. The minting mechanism of synthetic assets is similar to the lending market, where the collateral is locked and the synthetic assets become loans that incur debt. The debt of sUSD is denominated in US dollars, but the debt of synthetic assets such as Bitcoin is denominated in Bitcoin and fluctuates with the price of the token. SNX pledgers need to bear a corresponding proportion of the global debt in the system, which requires Synthetix to design complex hedging strategies to avoid the risks brought by price fluctuations. This hedging demand, extremely high collateralization rate and system complexity make SNX pledgers lack interest , so Synthetix recently launched a new model with the SIP-420 proposal.

In early 2025, SIP-420, which aims to simplify the sUSD minting process and improve the sUSD minting efficiency, was approved by governance. SIP-420 introduced a shared debt pool mechanism, and plans to gradually shift the sUSD minting method from an individual mortgage model to a collective fund pool model within 12 months. SNX pledgers no longer need to mint sUSD individually and assume personal debts, but can entrust funds to the public pool, thereby achieving a structure without liquidation and personal debt. At the same time, SIP-420 will also reduce the sUSD collateral rate from 750% to 200% to significantly improve the systems capital efficiency.

However, with the exemption of personal debts, when the sUSD price deviates from the anchor value, SNX pledgers no longer have the motivation to repurchase sUSD at a low price to repay debts (previously, individual pledgers could buy sUSD at a discount to repay debts to stabilize prices), and the original self-anchoring adjustment mechanism of the protocol becomes invalid. This is also the fundamental reason why sUSD will decouple.

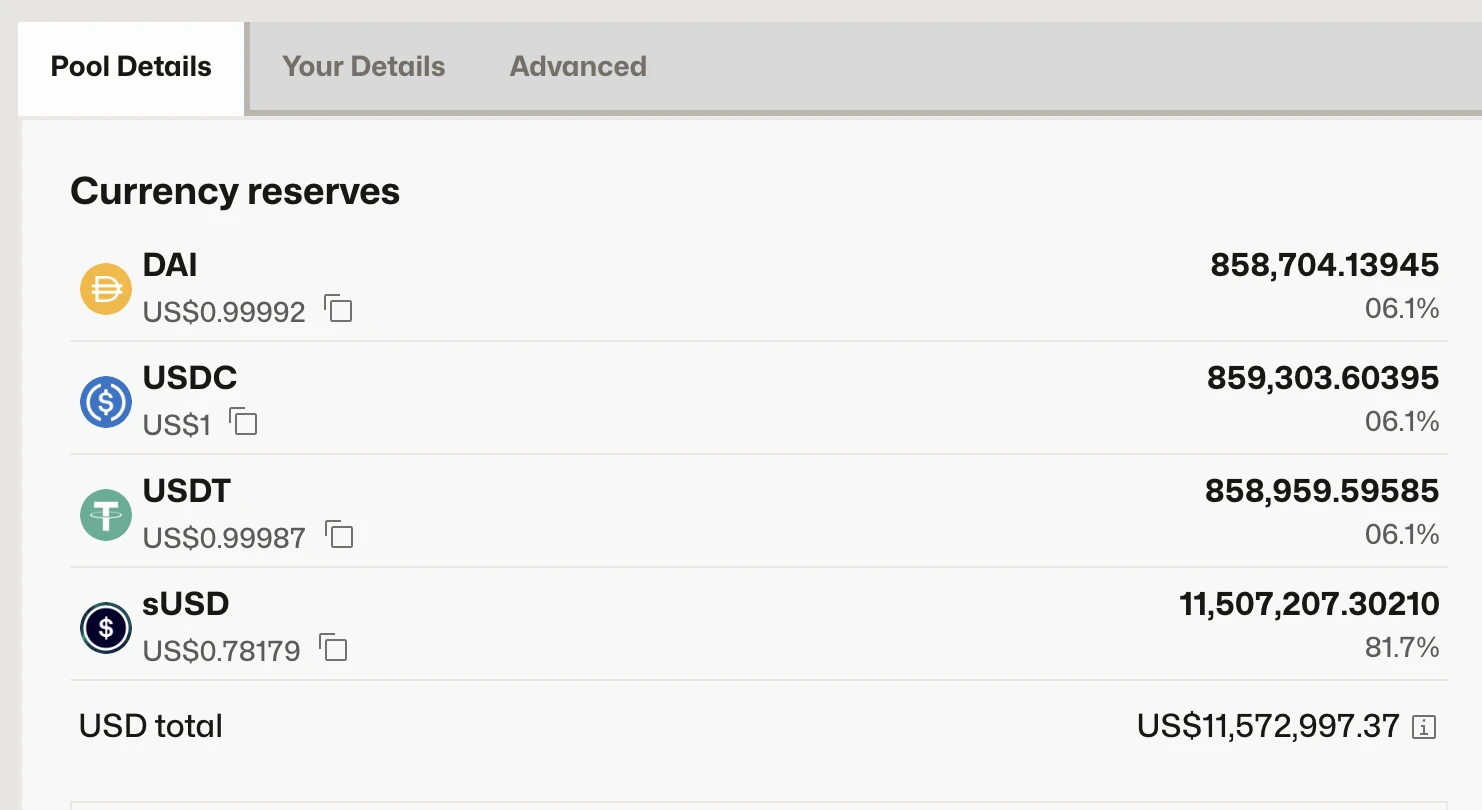

The reason why the depegging situation is gradually intensifying is that the sUSD liquidity is not as sufficient as expected. Taking the largest pool on Curve (sUSD/USDC/DAI/USDT) as an example, of the total liquidity of about 11.51 million US dollars, the sUSD pool accounts for about 81.7% - this means that the actual exit liquidity has been consumed in large quantities during the depegging process.

Synthetix’s Solution

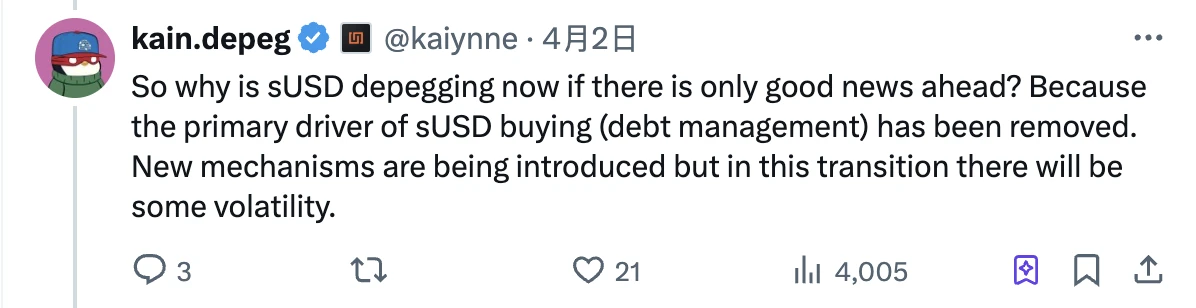

On April 2, Kain, the founder of Synthetix, responded to the depegging of sUSD for the first time. Kain mentioned that the depegging was because the main driving factor for purchasing sUSD (debt management) had been eliminated , and the new mechanism was in transition, so there was a short depegging.

As mentioned above, SIP-420 hopes to achieve a mechanism transition within 12 months, but the community obviously cannot wait for 12 months with a de-pegged stablecoin. To this end, Synthetix has recently launched a number of additional measures to try to fix the price of sUSD. The common keyword in these measures is incentive.

The first measure is to provide incentives for the liquidity of sUSD . In the latest incentives, the yield of sUSD/sUSDe LP pledged on Convex has reached 49.18%;

The second measure is to provide incentives for sUSD deposits through Infinex, another project developed by the same team. The incentives will last for six weeks, with 16,000 OP rewards distributed every week to users who deposit more than 1,000 sUSD.

The third measure is the latest plan, which is to allow users to pledge sUSD to the 420 pool. After staking, the sUSD will be locked for one year, but 5 million SNX will be provided as an incentive.

Obviously, the above three measures are all aimed at solving the problem of insufficient demand for sUSD purchases mentioned by Kain. By providing additional incentives for some pan-locking behaviors, Synthetix hopes to stimulate the demand for sUSD purchases and limit the potential selling pressure of sUSD, thereby gradually pushing the price of the stablecoin back to its anchor.

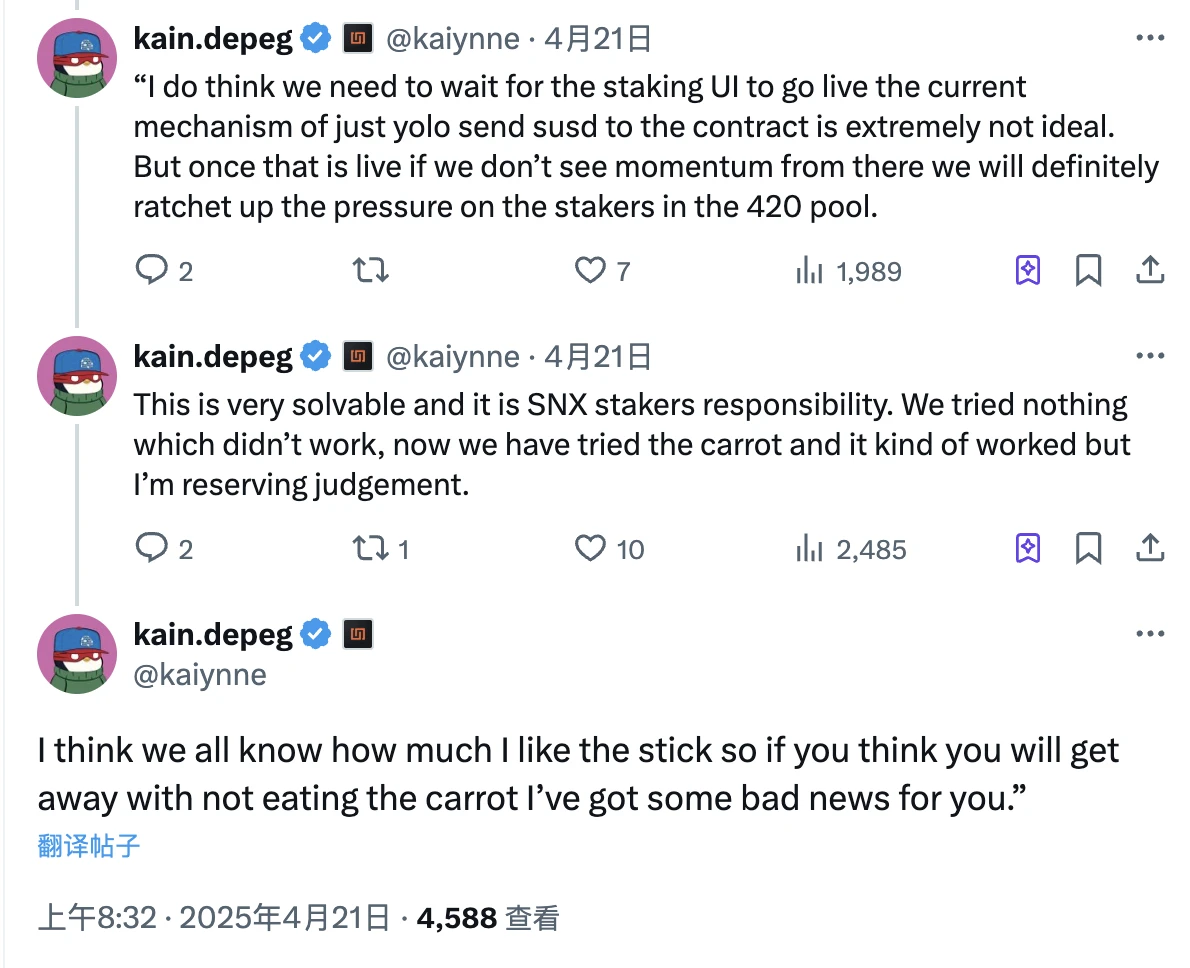

Especially for the third measure with stricter conditions and stronger incentives, Kain also published a post yesterday mentioning his expectations for this measure, and emphasized that the problem is completely solvable, and the team will gradually solve the de-anchoring problem by optimizing the incentive mechanism.

It is worth mentioning that Kain also mentioned that if SNX stakers do not adopt the newly introduced staking mechanism to help solve the sUSD (SUSD) depegging problem, they will be subject to a big stick - or implying that after multiple incentives, the next step is to use penalty conditions to put pressure on users who still do not cooperate with the repair action.

Since Synthetix has not yet provided a user interface for sUSD staking, the staking operation still needs to be handled manually by the team. Therefore, it is not yet known how many users will eventually participate in sUSD staking under the incentive, which will greatly affect the repair effect of sUSD.

Based on the current situation, it is difficult to determine whether Synthetix can stabilize the situation . Although there are some voices of bargain hunting in the market, I personally do not recommend fishing chestnuts in the fire right now. If you cant resist the temptation of discounts, you need to pay close attention to the price performance of SNX - to prevent the death spiral of price decline, insufficient collateral, increased discounts, and panic selling.

Alternative arbitrage opportunities

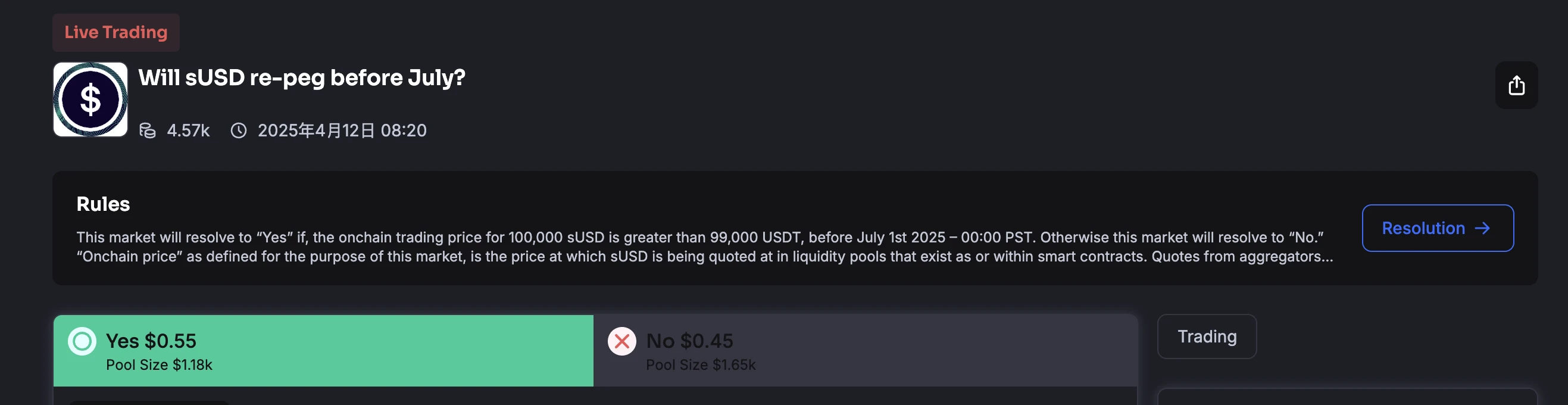

Compared with betting on anchor return, there seems to be another arbitrage opportunity in the market at present - the prediction market.

The prediction market Truemarket has launched a prediction pool on whether sUSD can return to its anchor before July. The current quote for the Yes share is $0.55 and the quote for the No share is $0.45.

Since sUSD is currently quoted at $0.78, the price of each unit of sUSD will be restored to $1 after the anchor is re-anchored, and each unit of Yes share can also change from $0.55 to $1. The existence of this price difference provides a certain arbitrage space.

However, the prediction pool on Truemarket is relatively small and cannot handle large-scale transactions, so the actual operating space of this strategy is not large. It is recommended to pay attention to whether other more mainstream prediction markets including Polymarket will open similar prediction pools and look for potential arbitrage opportunities.