Original author: James Zhu

TL;DR

The stablecoin market continues to grow, and crypto payments will not completely replace the traditional fiat currency system

The real significance of PayFi is to promote the application and innovation of crypto assets in real-world scenarios

Solana is not necessarily the only option for PayFi or crypto payment. Ton Network and Sui are likely to catch up with their respective advantages.

PayFi has huge potential in the future. As a composite innovative application in multiple tracks, its potential market value may exceed 10 billion US dollars.

In recent years, the crypto payment track has been constantly evolving, from the initial prejudice that crypto payments were considered to be gray market trading tools to the acquisition of the stablecoin platform Bridge by the traditional financial technology platform Stripe, and the entry of orthodox industry giants such as Paypal and Visa. Combined with the recent emergence of the new concept of PayFi, it has attracted widespread attention.

ArkStream In order to better understand the prospects of this track, we briefly sorted out the encrypted payment track and focused on how PayFi iterates the encrypted payment track, so as to gradually explore its future development direction.

Crypto Payment Track

Since its birth in 2008, Bitcoin has gradually transitioned from small-scale transactions by technology enthusiasts to commercial applications widely accepted by merchants around the world, and then to regulatory intervention and compliance development. It has now formed a diversified and platform-based payment ecosystem. Today, with the maturity of technology and the expansion of application scenarios, encrypted payments are gradually being integrated into the traditional financial system, providing users with more efficient, low-cost, highly transparent, and decentralized payment solutions, heralding a new round of changes in the field of financial technology.

Behind this innovation, stablecoins, as a bridge between cryptocurrencies and legal tender, provide a foundation for the widespread application of crypto payments through stable value storage and efficient on-chain circulation. Studying the stablecoin market can help us understand the entire market.

Stablecoin Market Overview

https://visaonchainanalytics.com/

https://defillama.com/stablecoins

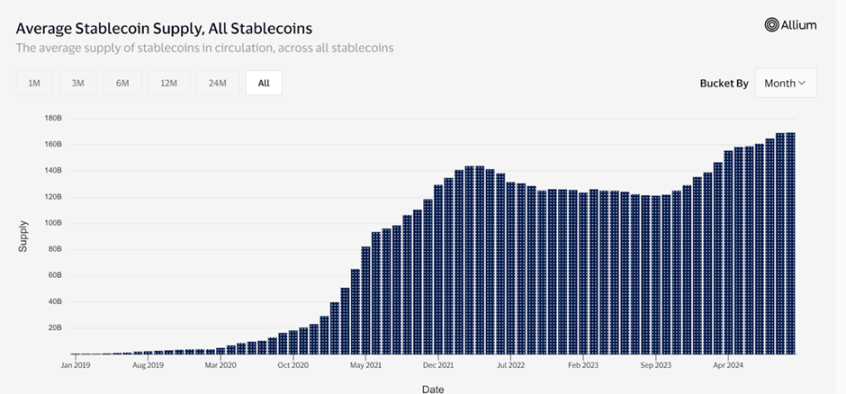

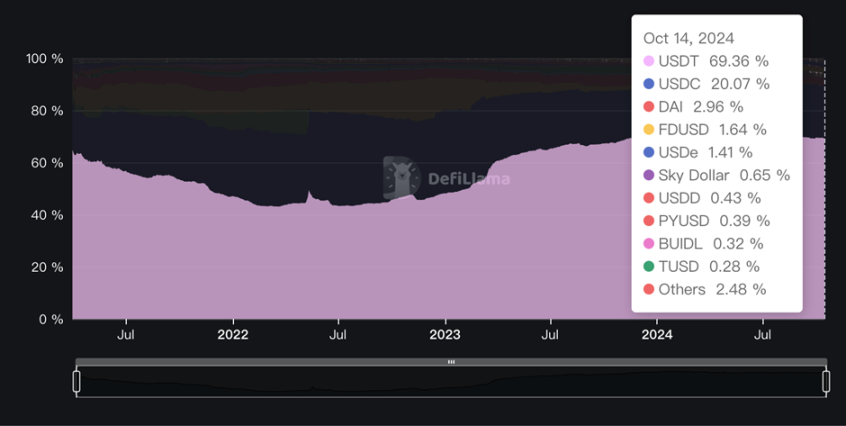

There is no doubt that the popularity of crypto payments is directly linked to the stablecoin market. These two charts (total stablecoin supply and respective stablecoin market share) reflect that the supply of stablecoins has experienced long-term growth worldwide. USDT and USDC, as the two giants of stablecoins, occupy 90% of the total market, and USDT is the undisputed leader (70% market share) and shows a stable and slow upward trend.

At the same time, we investigated the distribution of USDT and USDC on the chain. USDT was issued on 13 chains in total.

Among them, the issuance volume on Torn is the largest, accounting for more than 50%, followed by Ethereum and Solana. The top four on-chain issuance volumes account for nearly 99% of the total issuance volume. On the contrary, the distribution of USDC is more concentrated, with issuance on Ethereum accounting for nearly 92% of the total issuance volume, followed by Solana, Torn and Polygon.

It is not difficult to conclude that ETH and Solana are still the mainstream stablecoin application scenarios. The continued growth of the stablecoin track combined with the entry of many leaders in the traditional payment industry is sufficient to prove that the encrypted payment track has initially possessed an operating system of payment scale, and it also directly proves that the market recognizes the application scenarios of stablecoin payments.

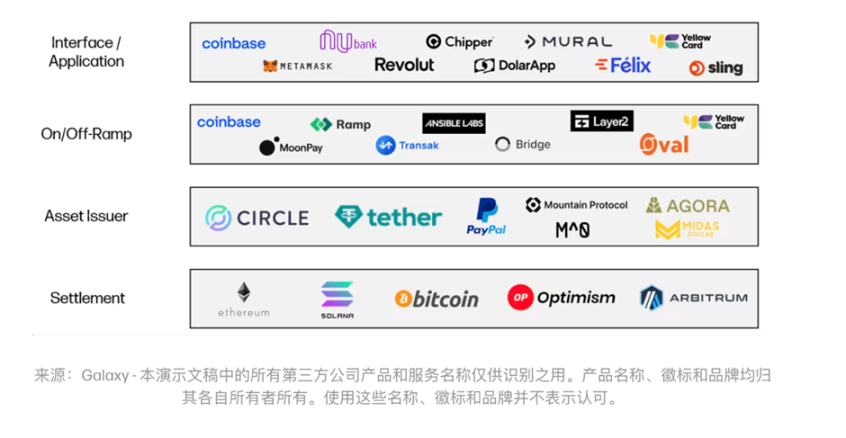

To better understand how crypto payments work, let’s analyze the four-layer architecture of crypto payment solutions, which ensures the security, scalability, and user experience of crypto payments.

Crypto Payment Solutions

In the cryptocurrency payment solution, we can see from the flowchart that there are four layers of architecture:

https://www.galaxy.com/insights/perspectives/the-future-of-payments/

Settlement layer: The public chain infrastructure at the bottom of the blockchain, many Layer 1s and general Layer 2s such as Optimism and Arbitrum. They differ slightly in speed, scalability, privacy and security, and are essentially selling block space.

Asset issuance layer: responsible for the creation, maintenance and redemption of stablecoins, aiming to maintain a stable value for fiat currencies or baskets of anchored assets. Issuers make profits by investing in stable-yield assets such as government bonds. Unlike intermediaries in traditional payments, asset issuers do not charge fees for each transaction using their stablecoins. Once a stablecoin is issued on the chain, it can be self-custodied and transferred without paying any additional fees to the asset issuer.

Deposit and withdrawal layer: Deposit and withdrawal providers serve as the connection between blockchain and legal tender, and as a technical bridge between stablecoins on the blockchain and legal systems and bank accounts. This type of platform is mainly divided into two categories: B2C and C2C.

Interface/Application: The platform provides a software interface to customer service, supports cryptocurrency payments, and uses traffic-driven fees generated by front-end transaction volume as a business model.

Current status of the encrypted payment track

Traditional payment giants enter the crypto market

With the year-on-year expansion of the crypto market and the approval of ETFs, traditional payment giants and crypto-native payment projects are actively developing and expanding related businesses. As early as 2023, Visa expanded the settlement function of USDC to Solana, providing a more efficient solution for cross-border payments and real-time settlement.

Combining the four-layer architecture of crypto payments that we introduced earlier, Visa builds its crypto payment ecosystem through multi-level cooperation:

At the asset issuance layer, Visa and Circle work together to use USDC as a stablecoin for settlement to ensure stable and compliant payments.

In terms of the gold layer, Visa supports users to move funds between fiat currency and cryptocurrency through cooperation with Crypto.com;

At the application layer, Visa provides acquirers such as Worldpay and Nuvei with the option of USDC settlement, ensuring that merchants can flexibly process crypto payments.

At the settlement layer, Visa chose Solana as the blockchain infrastructure, leveraging its high parallel processing capabilities, stable and predictable transaction fees, and fast block confirmation times to achieve more efficient on-chain settlement.

Through this integration, Visa is no longer solely dependent on the traditional bank settlement system. This integration means that users can use USDC for settlement directly through the blockchain network, eliminating intermediaries, shortening settlement time, and reducing costs. This move not only demonstrates how encrypted payments can bring innovation to the traditional payment system, but also provides new ideas for the future global payment network.

Paypal also chose Solana as its new public chain for PYUSD payment this year and actively promoted blockchain-based payment methods. Paypals vice president has repeatedly emphasized Solanas performance in high throughput and low latency, making it an ideal infrastructure for crypto payments. Although these traditional payment giants are not as good as Web3 native payment players in blockchain technology and understanding of the Crypto industry, they have quickly entered the crypto payment market with their huge user base and traditional industry resources to compete for market share.

Native Crypto Projects

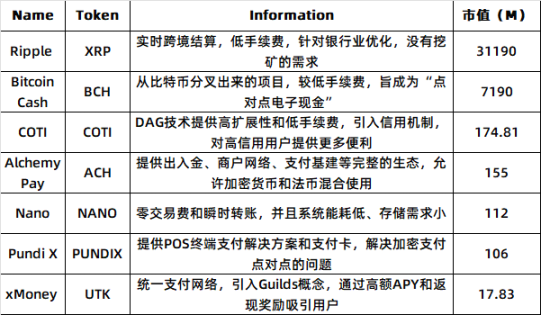

Compared with these traditional giants, native crypto payment projects promote business development in more innovative ways. Here we have counted the projects belonging to crypto payment in Binance Exchange.

Ripple for B2B cross-border transactions

Ripple has raised nearly $300 million in total so far, with investors including a16z, Pantera, Polychain, IDE and other well-known venture capital institutions. Currently, there are nearly 6 million active accounts, and more than 300 partner institutions in 50 different countries.

XRP is the native token of the Ripple Network. As a Layer 1 public chain, Ripple focuses on the B2B market and is committed to building a CBDC ecosystem in cooperation with banks around the world through a decentralized payment settlement and asset exchange platform.

Ripple uses the RPCA consensus algorithm, and its RippleNet is built on the XRP Ledger, providing a variety of solutions including xCurrent, xVia and xRapid, aiming to improve the efficiency and liquidity of cross-border fund transfers. Through these technologies, Ripple cooperates with traditional financial institutions such as Bank of America and Credit Suisse. Compared with the traditional SWIFT system, Ripple has significant advantages in transaction speed and cost, completing transactions in seconds at a cost of less than 1% of the traditional cross-border payment cost.

According to statistics, the number of XRP payment user transactions is about 150,000 per day, with an average daily active user of more than 10,000. Its development has not been smooth sailing. It has experienced a lawsuit by the SEC for several years, accusing it of issuing securities in an unregistered manner. It was not until recently that the SEC withdrew its lawsuit against Ripple.

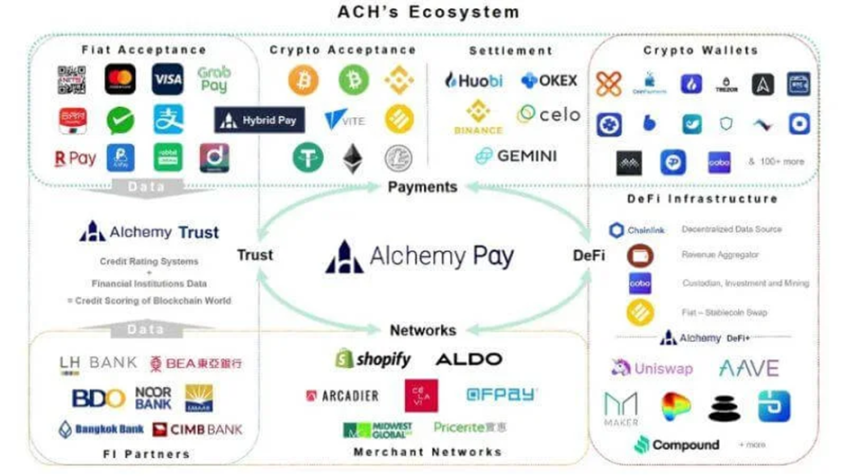

Alchemy Pay for Crypto Payments

Alchemy Pay has received a total of US$10 million in financing from investment institutions such as DWF and CGV. Recently, it has attracted public attention again due to its cooperation with Samsung Pay for its virtual card.

Alchemy Pay has built a hybrid payment architecture that combines on-chain and off-chain by integrating underlying payment protocols such as Lightning Network, State Channel, and Raiden Network. The on-chain is responsible for ledger management and data storage, while the off-chain handles computationally intensive tasks such as inspection and reconciliation. This architecture supports Alchemy Pay to provide customized solutions including deposit and withdrawal payment services, NFT quick purchase, encrypted credit cards, and encrypted payments.

https://alexablockchain.com/alchemy-pay-to-transform-crypto-payment-with-its-new-product/

According to the ACH ecosystem map compiled by a third party, Alchemy Pays ecosystem has opened up four major sectors: payment, merchant network, DeFi, and trusted assets. Its partners include industry leaders such as Binance, Shopify, Visa, and QFPay, highlighting its extensive layout in the entire payment chain.

The biggest difference from XRP is that Alchemy Pays token ACH is not a medium for crypto transactions, but provides users with cash back rewards through each payment, providing a consumption reward mechanism similar to traditional credit cards, enabling actual payment scenarios and improving user loyalty.

ArkStream believes that whether it is the traditional industry giants relying on their deep industry resources and global business network to enter the crypto market, or the crypto-native payment projects relying on their decentralized architecture and token economic model, these two types of players are promoting the development of the industry in different ways. Traditional giants have strong market influence and compliance advantages, while crypto-native projects have unique advantages in technological innovation and rapid iteration. Recently, we have also witnessed Stripe completing the largest acquisition in the history of crypto by acquiring Bridge. We look forward to the two forces joining forces to give full play to the traditional industrys ability in resource integration and large-scale operation, combined with the innovative mechanism of crypto, to promote the entire payment industry towards digitalization, cost reduction and efficiency improvement.

Pain points of the crypto payment track

1. Unstable transaction costs: The original intention of crypto payment is to reduce the middlemen and transaction costs in the traditional payment process, but in actual operation, its fees are not cheaper than traditional payment. The network often sees a surge in transaction fees during peak trading periods, especially the congestion problem of major public chains is more significant. In contrast, the rates of traditional payment tools such as credit cards or third-party payment platforms are more stable, and many daily transaction fees are borne by merchants (similar to the free shipping theory), which is less perceived by users and easier to accept.

2. Limited processing power: Although the decentralization and consensus mechanism of blockchain ensure the transparency and security of the system, it also greatly limits the processing power of the network. Since blockchain requires global nodes to reach a consensus, the transaction speed is limited by the block capacity and block time. Although Layer 2 expansion solutions (such as the Lightning Network), more efficient cross-chain communication and sharding technology may bring new breakthroughs, even Solana, which has been proven to have the best performance, still cannot be compared with traditional payment giants such as Visa in terms of its highest TPS. For high-frequency small-amount payment scenarios, the current encrypted payment network still has obvious bottlenecks.

3. Lack of application scenarios: Although crypto payments can be used for daily consumption, transfers, cross-border payments, etc. in reality, common business scenarios in mature financial market environments, such as lending, insurance, leasing, crowdfunding, asset management, and other derivative application scenarios, still rely on the traditional financial system, and the share of crypto payments is completely blank.

ArkStream The fundamental reason is that the iteration of existing crypto technologies and the application of products often give priority to the interests of existing users in the crypto field and ignore the broader market needs. Whether it is Alchemy or Visa, the focus on blockchain is still on deposits and withdrawals, crypto debit cards, and crypto peer-to-peer payments. In order to further achieve Mass Adoption, ArkStream believes that project parties need to pay attention to the needs of users outside the crypto ecosystem, especially the needs to unlock more application scenarios and create a full payment ecosystem for crypto. Lily Liu, chairman of the Solana Foundation, noticed this market gap and proposed the concept of PayFi at the Hong Kong Web3 Carnival in April 2024 to meet these challenges and promote the widespread use of crypto payments.

PayFi: A new chapter in Web3 payments

PayFi Introduction

First of all, what is PayFi?

PayFi is not an independent concept, but an innovative application that integrates Web3 payment, DeFi, and RWA.

RWA tokenizes assets and puts them on the chain, allowing for a 1:1 seamless transfer of value on the blockchain and using smart contracts to build transaction and settlement processes;

DeFi focuses on the on-chain economy and innovation of traditional financial products around decentralization. Whether it is automated market makers, flash loans, liquidity mining, etc., its mainstream purpose is trading;

Web3 Payment focuses on using cryptocurrency as a payment transaction medium, such as cross-border remittances and encrypted payment cards, to improve the efficiency of traditional finance.

However, PayFi is not equal to RWA, Web3 Payment or DeFi. ArkStream believes that its real significance lies in promoting the application of digital assets in real scenarios in the real world. To be more precise, it expands the innovative application scenarios of DeFi to reality on the road already paved by RWA and Web3 Payment.

https://www.feixiaohao.com/news/12951184.html

PayFi focuses on two core concepts:

Tokenization of real-world assets: When the essence of transaction payment scenarios is real life, the premise of realizing PayFi is to move traditional payment scenarios to the chain through tokenization. Through the tokenization of stable and low-risk assets, DeFi can achieve capital transparency, high liquidity, multiple gameplay, and high returns. At the same time, RWA provides a wider range of asset categories and a stable source of anchored income.

Unleashing the time value of funds: Another important concept of PayFi is to realize the time value of funds in a relatively low-cost but most efficient way through the characteristics of smart contracts and blockchain centralization. For example, users can manage and invest funds without intermediaries, such as on-chain flash credit markets, installment payment systems, and automated investment strategies. More application scenarios are all aimed at reducing opportunity costs and enabling funds to quickly enter the market for reinvestment or other purposes.

Here we use a basic mathematical model to quantify the value created by PayFi, focusing on the opportunity cost loss caused by the capital yield:

P is the prepayment amount, r is the interest rate, and assuming that traditional cross-border payments take 3 days and crypto payments take 3 minutes, we can calculate the opportunity cost of the two cases:

Opportunity cost (traditional payment) = P × r × 3

Opportunity cost (payment in crypto) = P × r × ( 3/1440)

The difference between the two is about the interest rate difference of 3 days. From our simple reasoning, we can conclude that the opportunity cost difference between the two will become larger and larger as the prepayment increases and the interest rate rises. Therefore, this efficiency improvement is particularly significant in high-frequency, large-value transactions, and interest rate hike environments.

PayFi’s public chain selection

So far, many crypto payment projects have come to Solana for deployment. At present, Solana has become the main platform for PYUSD, with a market share of 64%, far exceeding Ethereums 36%. EUROC, EURC and other stablecoins that meet the MiCA standard will also be launched in the Solana ecosystem.

So why do both traditional finance and native crypto projects tend to develop on Solana? We analyzed this and summarized the following key factors: high-performance public chains, capital liquidity, and talent liquidity.

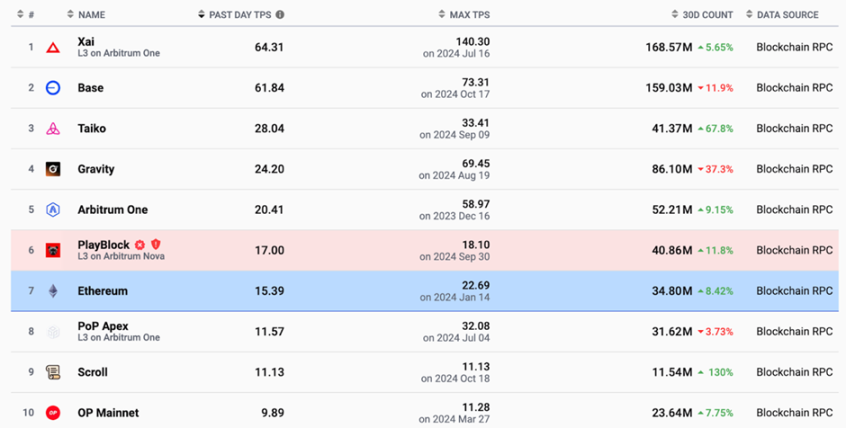

High-performance public chain: Solanas high performance is its core competitiveness. So far, its recorded TPS ranks among the best in the public chain. Solanas consensus mechanism and low gas fee make its performance significantly better than most L2 solutions.

Capital Liquidity: Solana’s ecosystem has received $61 billion in pledged capital, and investments from top venture capital funds such as a16z and Polychain Capital have further enhanced Solana’s market confidence and competitiveness.

Rich application group: Many C-end application scenarios, whether it is Sanctum debit card, Helium Sim card or Solana official mobile phone, far exceed the application construction of other public chains

Most Layer 2 projects such as Optimism, zkSync, Lighting Network or public chains including Polygon, Monad, Aptos, etc., all claim to have stronger and better TPS and scalability. However, according to website data, the highest TPS records of most L1 and L2 are not even a fraction of Solana.

https://l2 beat.com/scaling/activity

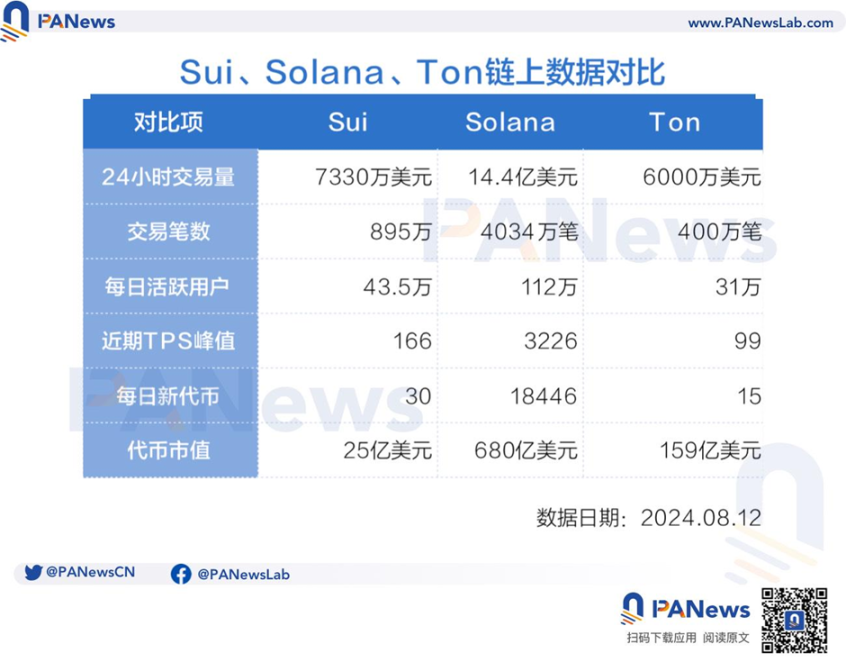

Although Solana has experienced several major security issues since its mainnet launch in 2020, ArkStream believes that it will be difficult for a chain to fundamentally replace Solana in the short term. Here we believe that Sui and TON, as two emerging public chains, are gradually showing their unique advantages and providing more options for the development of future encrypted payments.

Sui: Parallel Processing + Innovation Ecosystem

As a new generation of public chain, Sui adopts DAG architecture and parallel processing. Unlike Solanas high-frequency trading and DeFi expertise, Sui focuses more on solving network bottlenecks in large-scale user interactions. This also explains why Gamefi and more complex contracts may benefit from Suis parallel computing capabilities and scalability.

Although Sui has not attracted large-scale capital like Solana, and its peak TPS is less than half of Solana. However, the development team behind it has rich experience in payment and decentralized application development, and may attract more innovative projects to develop on its ecosystem in the future. For PayFi, Suis parallel processing capabilities may highlight its advantages in applications with intensive user interaction.

TON: Community + Payment Bridge

TON originated from Telegrams platform optimized for large-scale community communications and small multiple payments. Different from the technical paths of Sui and Solana, TON focuses on low latency and high scalability. Its sharding architecture can support a large number of small payment transactions and has been integrated into Telegrams user ecosystem.

TON’s greatest potential lies in its huge user base, backed by 900 million monthly active users and integrated mini app functions. As a bridge connecting Web2 + Web3, TON provides a huge ready-made market for payment projects such as PayFi through social payment and micropayment fields.

https://www.techflowpost.com/article/detail_19707.html

Although Solana has taken a leading position in the current crypto payment market, including PayFi, with its proven high performance, rich DeFi ecosystem and capital advantages, as technology continues to upgrade, the future of crypto payment may be multi-chain coexistence. Suis parallel processing capabilities and innovative application scenarios, as well as TONs widespread use in social payments, are expected to become the key force in breaking the existing crypto payment landscape.

As for whether the PayFi project will choose Sui or TON, it may ultimately depend on factors such as the projects product demand, market positioning and GTM strategy, but the richness of multiple chains and application scenarios in the future will undoubtedly provide more opportunities for the PayFi project.

Business model and application

The concept of PayFi was first proposed in April 2024, and the number of related projects is relatively small. We divide the projects in PayFi that we have seen so far into two tracks. The two application scenarios are: cross-border trade and credit finance.

Huma Finance

Product introduction: Huma Finance is the current focus of the PayFi track. Its main business is PayFi applications for C-end and small and medium-sized enterprises. The newly acquired Arf mainly solves the liquidity of prepaid capital in current cross-border payments.

Arfs vision is to solve the liquidity and timeliness issues of prepaid capital in current cross-border payments. Through the Arf platform, the trust issues between buyers and sellers are solved, and there is no need to prepay banks or letters of credit, which are required for traditional cross-border transactions. Arf builds an on-chain liquidity network by providing peer-to-peer services, providing on-chain stablecoins to enterprises in advance while eliminating the need for prepayments. When using Arfs services, enterprises only need to pay the relevant fees and repay Arf within the agreed time.

https://x.com/arf_one

Meanwhile, the main business of Huma Finance revolves around the concept of Buy Now, Pay Never claimed by Lily Liu. The core concept is that customers can choose to use their accounts receivable that are about to expire as collateral. Huma tokenizes these accounts receivable through its agreement. Customers borrow from the loan pool, and the mandatory part will be implemented by the smart contract on the chain. Its extensibility includes: trade financing, small and micro enterprise credit, international tuition payment, etc.

Technical architecture: Huma Finances PayFi Stack includes six layers: transaction layer, currency layer, custody layer, financing layer, compliance layer and application layer, covering all levels from transaction processing to asset management, financing and compliance. This full-stack design ensures that the entire process from loan application, asset evaluation, capital provision to final payment can be completed in the same ecosystem. PayFi greatly simplifies the complex lending and payment process through automation, decentralization and multi-level technology integration, improves efficiency and reduces costs.

Data analysis: So far, the total loan amount is 1 billion US dollars, and there is no record of default. As the leader in the PayFi track, Huma Finance has raised 38 million US dollars.

PayFi future development market

After introducing PayFi-related projects, we also thought about the regions of its application scenarios. ArkStream believes that PayFi undoubtedly has the potential for global mass adoption, and its early application scenarios are not necessarily limited to developed countries (the United States, Singapore, Europe, etc.). We believe that emerging markets also have broad prospects.

Market strategy in developed countries: In developed countries, PayFi can use its ability to integrate DeFi innovations to supplement existing digital payment systems. Due to the clearer regulatory framework and policy support in developed countries, (such as USDC, PYUSD, EUROC) have been widely used in these countries. Finding a suitable entry point, for example, cooperating with retailers, e-commerce, and cross-border financial platforms to build low-cost and more capital-efficient crypto payment channels may accelerate the opening of the PayFi market.

Opportunities in emerging markets: At the same time, PayFi is in areas where traditional financial services are lacking. By providing products such as crypto micro loans and flash loans, the decentralization and cross-border convenience of the crypto payment system can provide financial services to these unbanked people. For example, in Africa, Southeast Asia and Latin America, or in some countries with high inflation fiat currencies such as Nigeria and Argentina. Because emerging markets lack complex traditional financial infrastructure, providing stable PayFi products may achieve scale faster than in developed countries.

Therefore, ArkStream concluded that PayFi should combine multiple market development strategies and develop on two tracks: in developed countries, the focus should be on iterating and establishing partnerships to assist existing application scenarios. In developing countries, the focus should be on promoting the application of encrypted payments and PayFi and the penetration of the cross-border remittance market.

Development prospects

Although the concept of PayFi was proposed not long ago and its application projects are relatively scarce, ArkStream believes that PayFi has potential for future development in the current environment. We see that both the development of crypto payment projects and the external economic environment are of great benefit to PayFi.

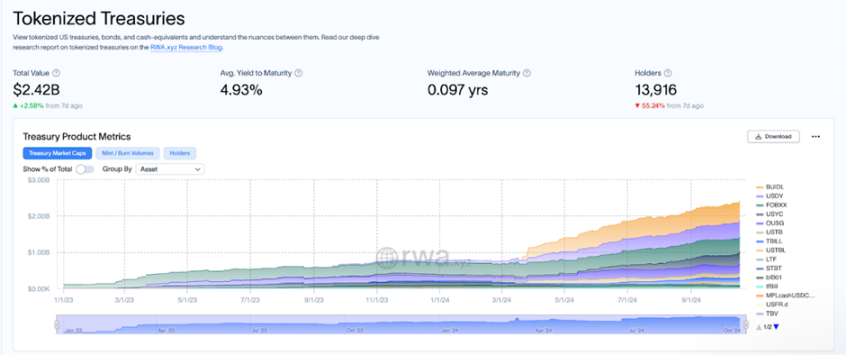

The global high interest rate environment caused by the US interest rate hike in the past few years has led to a lot of attention to bond products, and many users in the crypto market have also transferred their money to the tokenized bond market. Users value its stable underlying assets and relatively high liquidity.

According to RWA.XYZ data, the size of the tokenized U.S. Treasury bond market has increased from US$770 million at the beginning of 2024 to US$1.916 billion today (as of August 1, 2024), an increase of 248%.

https://app.rwa.xyz/

As the United States announced a rate cut, the yield of U.S. Treasury bonds continued to decline, and investors dependence on U.S. Treasury bonds weakened. At the same time, this part of the funds needed to find the next scenario to take over. Investors turned to look for other assets with sustainable value and stable income sources.

PayFi, combined with the rise of the RWA model, just fills this need. Currently, the locked-in amount of the RWA track is as high as 6 billion US dollars, and it continues to rise. The essence of RWA is to transfer real-world assets (such as bonds, accounts receivable, supply chain financial assets, etc.) to the chain through tokenization, providing investors with diversified choices and achieving higher liquidity of assets.

Here we provide three potential RWA targets:

MakerDAO RWA provides traditional assets such as real estate and accounts receivable, combined with the DAI stablecoin issued by MakerDAO, to effectively connect the capital demand of the off-chain with the liquidity of the on-chain. It is also the RWA protocol ranked first in TVL.

Tether Gold provides traditional gold-pegged tokens, allowing investors to invest in gold through cryptocurrency without having to directly hold physical gold;

Ondo Finance provides risk-graded treasury bonds, corporate bonds, and other real financial assets on the chain. Funds can be invested according to risk preferences. Against the backdrop of declining treasury bond interest rates, RWA products such as corporate loans provided by Ondo may be more in line with investors preferences.

in conclusion

At present, the number of projects related to the PayFi track is extremely limited, and most of them are still in the early stages of development. Therefore, we pay more attention to the innovation of PayFi project solutions.

From the perspective of business model, PayFi combines multiple tracks such as crypto payments (such as Ripple, Stellar), DeFi lending (such as AAVE, Compound), RWA (such as MakerDAO RWA, Ondo Finance), etc. Projects in these fields have successfully verified the feasibility of their business models and proved their market demand and growth potential. By horizontally referencing the market value of these tracks, PayFi, as a composite innovative business model, may have greater room for development. Considering that the market value of leading projects in fields such as crypto payments, credit financing, and RWA has reached billions to tens of billions of dollars, we have reason to speculate that with the unlocking and superposition of multiple scenarios such as cross-border payments, supply chain finance, and corporate financing, the overall market value of the PayFi track may even break through this upper limit.

From a product perspective, the development of the PayFi project in the future should focus on segmented payment scenarios and optimize the efficiency and experience in these areas. There is no doubt that PayFi is one of the few remaining blue ocean markets, but there is still a lack of a large number of application projects in this track. We call on more developers to use existing encrypted payment technologies, pay attention to the global market, and innovate in combination with actual needs in real life.

For example, at the Token 2049 conference this year, we noticed that TADA Taxi’s cooperation with the Ton Network reduced the commission rate of taxi software through encrypted payment and profit sharing, making it stand out among similar taxi platforms. At the same time, we also noticed that Ether.Fi is carrying out encrypted payment card business. Its Cash business not only has the functions of traditional encrypted payment application scenarios, that is, depositing encrypted assets for consumption. At the same time, it allows users to use the income from liquid pledge to repay their consumption expenses.

This kind of breakthrough in real-life scenarios is where PayFi has great potential that can be used as a reference worldwide. Project owners should not only focus on finding the next high-yield reservoir for on-chain funds, but should pay more attention to how to let users in traditional industries experience the convenience of PayFi, and further increase the penetration of the crypto market from an altruistic perspective such as price and products.

It is conceivable that many new financial products that are difficult to achieve in the traditional financial system will appear in the future, such as:

Second-level lending: By pledging crypto assets through the PayFi platform, users can obtain loans that are more advantageous than traditional financial channels;

Pre-consumption and investment: Without the need for debt, users can consume or invest in advance before the future income cycle arrives;

High-yield liquidity funds: By using pledge and liquidity pledge, users can retain the liquidity of funds while enjoying high yields of more than 10%;

Prepayment of interest on locked-in financial products: Users can use interest as working capital before the financial product matures.

These innovative products all take advantage of the core concept of time is money. By maximizing the value of time, we clearly realize that PayFi is not a castle in the air, nor is it just a carnival for insiders. Whether from the perspective of practicality or innovation, PayFi is gradually opening up the path of integration between crypto and traditional finance. As a long-term investor, ArkStream sees the potential of PayFi and even foresees a bankless future.

The innovation of these application scenarios combines the needs of DeFi and real-world applications, further verifying the huge potential of PayFi in releasing capital efficiency. ArkStream believes that the long-term application prospects of PayFi are unlimited.

Reference

https://visaonchainanalytics.com/

https://defillama.com/stablecoins

https://www.galaxy.com/insights/perspectives/the-future-of-payments/

https://usa.visa.com/solutions/crypto/deep-dive-on-solana.html

https://usa.visa.com/solutions/crypto/deep-dive-on-solana.html

https://www.explinks.com/blog/web3-payment-research-report/

https://alexablockchain.com/alchemy-pay-to-transform-crypto-payment-with-its-new-product/

https://www.feixiaohao.com/news/12951184.html

https://l2 beat.com/scaling/activity